MACRO OVERVIEW

Global equity markets notched a new all time high in early September only to pull back since. The rise in market volatility has some fearing another meltdown. To be clear, nobody knows what happens next, but it’s worth noting how current economic and market conditions contrast with Q1.

Figure 1: Global Equity Market

The crash in Q1 was led by deteriorating fundamentals. COVID-19 was the match that lit everything ablaze (something I did not foresee), but the data were what they were. Had it not been COVID something else would have eventually blown up.

On the other hand, the rally from the March low appears to be supported by relative improvements in fundamental data. Relative being the key word. There’s no doubt economic conditions are still ugly. But as I wrote in August, it’s also possible for markets to be less ugly than they were before.

For example, in the US the Treasury Yield curve has decidedly steepened out of inversion after oscillating around the zero line for a year. This is a positive sign from a strong leading indicator.

Figure 2: US Treasury Yield Curve

We’re also seeing leading indicators rise globally as reflected by the OECD Composite Leading Indicator data shown in Figure 3. At this point the recovery looks as extreme as the the decline, and it reflects a world in synchronized re-acceleration following the sudden stop in Q1.

Figure 3: Composite Leading Indicators

Meanwhile, market conditions continue to improve from the depths of the March lows. The extreme spikes in volatility we saw across asset classes are receding back towards pre-COVID levels. Although September saw a rise in volatility, the overall trend has been improvement towards calmer market conditions.

Figure 4: Asset Class Risk

These changing conditions led to a change in MV’s risk exposure positioning. In Q3 MV increased its target risk allocation from underweight to neutral weight, where it remains at present.

To be sure, there are no shortages of risks and uncertainties. While a burgeoning recovery appears to be underway, anything from a resurgence of COVID to a contested presidential election could flip conditions upside down.

That said, we know we cannot predict what will happen next or when markets will move. Instead, we simply pay close attention to current economic and market conditions, and adjust our risk exposure accordingly. At present conditions call for neutral risk exposure and we will adjust as conditions change.

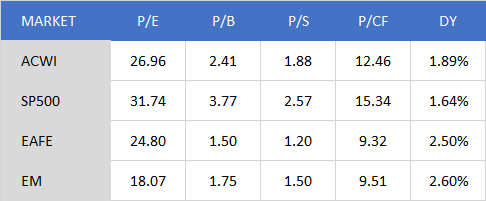

SEEKING VALUE

Within MV’s risk allocation, it’s becoming increasingly difficult to find anything that’s priced “low.” That isn’t a surprise based on simultaneous all-time-highs in global equity markets and all-time-lows in interest rates. From risky tech stocks to to risk-free Treasuries, just about everything looks expensive.

In times like these, relative values (versus absolute) are the best we can do. From that perspective we favor foreign equity markets, both EAFE and EM relative to US and global markets.

Figure 5: Equity Market Valuations

However, due to a lack of perceived absolute value MV is keeping value position sizes small. This results in a peculiar situation where MV’s value positions are substantially less than MV’s target risk allocation.

In other words, MV’s current risk exposure target for the portfolio is 60%, but the total of all value positions only add up to 30%. That leaves a risk exposure shortfall of 30% (60% Target – 30% Value = 30% Shortfall). There are three choices to remedy this shortfall.

- 1) Do nothing and remain underweight risk exposure. Doing nothing is the easiest choice, but may also be the riskiest in terms of opportunity cost. For example, imagine sitting in cash for all of 2019 or Q3 2020 because equity valuations did not look low enough – those would have been costly decisions.

- 2) Increase value position sizes to fill the risk allocation shortfall. Increasing position sizes must be done within reason and limits. First, value position sizes should be justified by valuation and expected return, not the risk exposure target. Second, hard limits on value position sizes are mandatory to protect against the inevitable chance of being wrong.

- 3) Fill the risk allocation shortfall with broad, global equity market exposure. The rationale for this is the risk allocation target is determined by economic and market conditions, not by valuation. In other words, current conditions can call for high risk allocation even if valuations are high.

In practice, prevailing circumstances determine which remedy is most appropriate. Currently, economic and market conditions call for a neutral risk allocation of 60% which also implies a continuation of the upward trend in risk assets.

Therefore MV is filling the risk exposure shortfall with a position in ACWI (All Cap World Index). This can be seen as the “next best alternative” because it allows MV to participate in the “rising tide” of the global equity market and also avoid the the risk of picking a “leaking boat” (picking the wrong market). That risk is especially germane at present given the lack of compelling valuations.

A NOTE ON VALUATION

I recognize taking a position in global stocks may seem contradictory given my gripes about equity market valuations. So I’ll reiterate MV’s target risk allocation is not based on valuation. It’s based on broad economic and market conditions. The risk target is changed tactically as conditions change, irrespective of valuation.

That being said, yes, equity market valuations look high, well-above averages, and likely to revert one way or another over time. However, just because prices look high today does not mean they will not go even higher tomorrow.

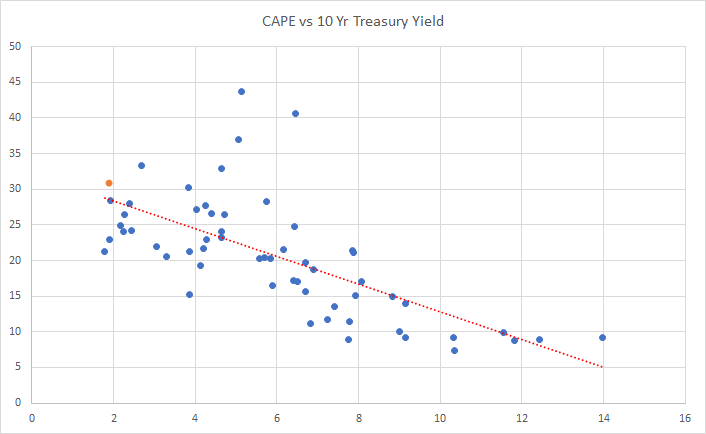

That cliche is obviously not a good reason to buy, but it’s also extra-relevant due to the current interest rate environment. Equity market valuations have an inverse relationship with interest rates. In other words when interest rates are lower market valuations are higher and vice-versa.

Figure 6 shows this by plotting stock market valuation on the Y-axis (S&P 500 CAPE ratio) over interest rates on the X-axis (10 Year Treasury Yield). The inverse relationship is highlighted by the red trend line. Notice when interest rates are lower (to the left), market valuations are higher. Presently, we are very close to the trend line (orange dot).

Figure 6: Equity Valuations

Intuition tells us the relationship isn’t random. For example, let’s assume the 10-Year Treasury note currently pays 0.70% interest per year. That yield is safe and guaranteed but also very low. Investors who want higher returns would need to invest in riskier assets, like stocks, for example. The lower interest rates go, the more investors may be forced into riskier assets, bidding up prices and valuations.

Beyond that logical reasoning, there’s also an empirical explanation. When interest rates are lower, future cash flows are “discounted” less, resulting in higher present values. Rational investors should be willing to pay more for those higher values, once again leading to higher valuations. This especially germane to equity prices because much of a stock’s worth is based on expectations of future cash flows like sales, earnings, and dividends, etc.

The point is stock market valuations, although high, may not be as high as they look on the surface due to the current interest rate environment. Low interest rates can act as a support for elevated stock market prices. For what it’s worth, the US Federal Reserve has said it plans to keep “policy accommodative” (low rates) until 2023.

THE BOTTOM LINE

To be sure, there are no shortages of risks and uncertainties looking forward, and anything could happen. Unable to predict what happens next, MV starts by focusing on current economic and market conditions. Those conditions currently call for a moderate level of risk exposure, regardless of valuation.

To the extent that MV cannot complete the target risk allocation with undervalued positions, it will fill the shortfall with the next best thing, which is broad, global equity market exposure.

Portfolio risk exposure will change based on economic and market conditions, while value positions will change based on valuations and expected returns.

We cannot predict when these changes will happen, we can only assure you they will. To that end we will be watching closely, waiting patiently, and responding to the changes as they occur. We’ll keep you informed of what we are seeing and doing along the way.

—

Victor K. Lai, CFA

You must be logged in to post a comment.