THE DEATH OF VALUE

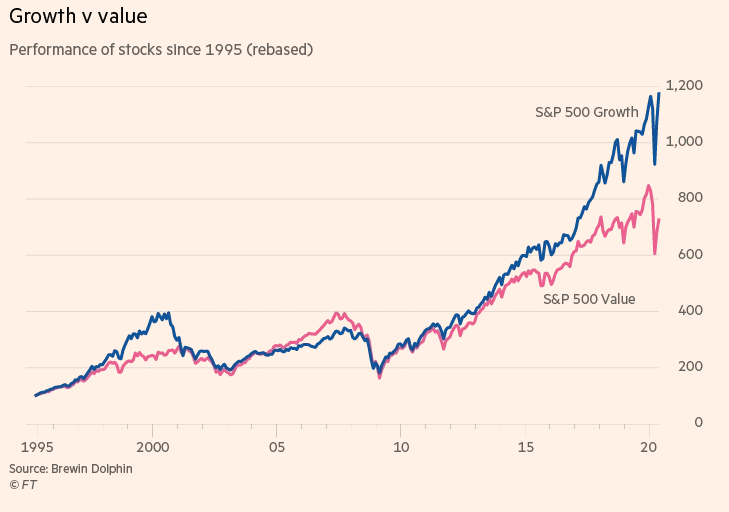

The death knell for “value-investing” has rung many times over the years. And after a decade of lagging explosive growth stocks (like “FANGMAT”) it rings louder than ever. The divergence between growth and value has reached historical levels and now looks even more stretched than during the 1990s dot-com boom. Is it time to leave value for dead once and for all?

Some investors believe so. They say markets, investing, and the world have all changed since the good-old-days of Benjamin Graham’s Security Analysis (aka “the bible” of value investing). In some ways, they’re right. Historically low interest rates, stubbornly low inflation, anemic economic expansion — all of these factors contribute to growth outperforming value.

A LONGER LOOK

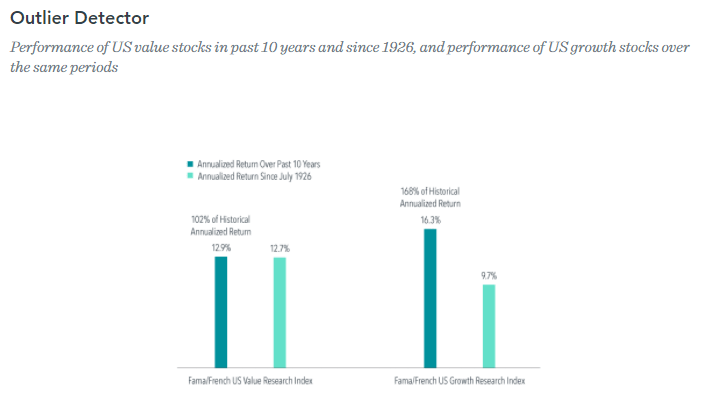

However, it’s worth noting that 10 year or even longer periods of underperformance may not be enough to write-off value. That’s because value has a very long history of outperformance. In fact, over some 100 years of market history value has demonstrated a return premium versus growth of over 300 bps per year.

In addition, that premium has shown to be statistically significant (not random), with value outperforming 59% of the time. Of course, that also means value underperformed 41% of the time. From that perspective, value’s “underperformance” should expected with some frequency.

Despite all the criticism value gets for “underperforming,” it really isn’t doing that bad. Value stocks have delivered an annualized return of ~13% over the past decade. Not only is 13% per year nothing to complain about, but it’s also very much in line with long-term historical returns for value. In other words, value stocks have behaved as expected.

In reality, what has not behaved as expected is the performance of growth stocks. Growth stocks have delivered an annualized return of ~16% over the past decade, well above it’s long-term historical return of ~10%. In other words, the outperformance of growth stocks has been the real outlier, not the underperformance of value.

THE LONG AND SHORT OF IT

In the short run anything is possible and it’s reasonable to assume value will likely continue to trail growth near-term. However, I don’t believe that marks value’s demise and over a longer period I expect value to outperform again.

From that perspective, it makes sense to use market strength to to rotate out of high-flying growth sectors like tech, and into out-of-favor segments like (dare I say it) energy. Yes, the energy sector clearly faces both near and long term challenges. However, the current uncertainties surrounding the sector may also sow the seeds for an upside surprise over time.

It’s worth nothing we saw a similar setup during the dot-com boom of the 1990s when tech was also heavily favored over energy. But in the following decade energy was the best performing sector and tech the worst. This time around, the contrast is even more pronounced.

History may not repeat itself, but it often rhymes. Listen carefully and that ringing death knell starts to hum a familiar tune — that it’s not time to leave value for dead.

—

Victor K. Lai, CFA

You must be logged in to post a comment.