Global equity markets have continued an “unprecedented” rally and in the US the S&P 500 has notched a new all-time-high. Many intelligent investors have watched in disbelief as stocks shot up despite dismal economic conditions. But the seemingly irrational market may be more logical than it appears.

Caution and Uncertainty

BCM was certainly in the cautious camp due to the severe and (dare I say again) “unprecedented” collapse in both economic and market conditions. Stocks experienced the fastest bear market ever in Q1 and heading into Q2 everything from GDP to employment was deteriorating at shocking rates. Given the extreme levels of uncertainty, caution was warranted.

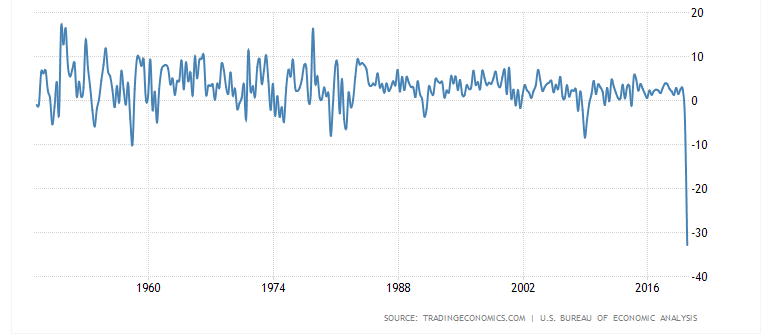

Figure 1: US GDP Growth Rate, April 2020

Figure 2: US Initial Jobless Claims, April 2020

As BCM clients know, we began moving to towards underweight risk positions across all our models early in Q1 and that helped avoid the worst of the market draw-down that followed. Like I wrote before, it wasn’t because we could predict market moves (we can’t), rather the economic and market data we follow had been deteriorating since late 2019.

We had no idea COVID-19 would strike or how much the market would move in response. However, we saw weakening data while markets appeared priced for perfection, “historically, not the best environment to be reaching for risk and returns.” If it wasn’t COVID-19, it would have been another shock, eventually. The point is the data drove our decisions and the timing was mostly lucky.

For Better or Worse

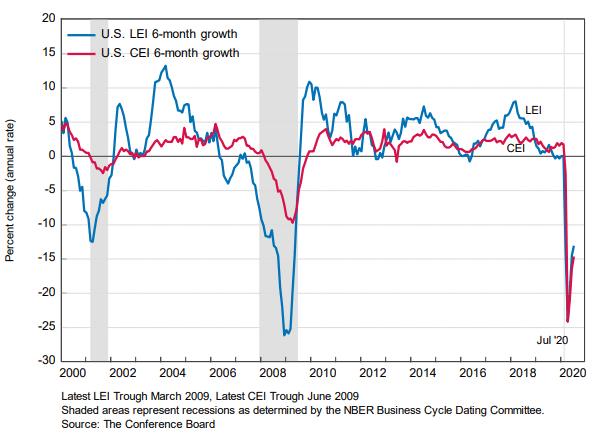

That point in mind, it’s important to recognize the data has been changing again heading into Q3. Figure 3 shows the rate of change in US economic indicator indices published by The Conference Board.

Figure 3: US Leading and Coincident Economic Indicator Indices

Figure 4 shows the Global Economic Surprise Index published by Citigroup. Combined, the charts show the extreme collapse of economic conditions during Q2, as well as the extraordinary (and unexpected) rebound since then.

Figure 4: Global Economic Surprise Index

To be clear, economic conditions are still plain ugly. That fact makes it difficult for logical investors to justify equity prices. However, a change in perspective can provide a perfectly rational reason for this market behavior.

While logic may be black and white, yes or no, the market often moves in the grey. In other words, markets can take a “relatively better or worse” perspective instead of an “absolutely good or bad” one.

Yes, conditions may still be ugly, but they can also be marginally better-looking than before. Assuming conditions continue to improve, there’s no reason equity markets cannot continue to grind higher. The key is the marginal improvement or deterioration.

The Bottom Line

We are not married or bound to a single position for better or worse — we are not forever bullish or bearish. Likewise, we don’t change our positions based on feelings or emotions. Instead, we change our positions as economic and market conditions change, for better or worse.

Just as quickly deteriorating conditions brought us to maximum risk underweight in Q1, improving conditions are guiding us back to strategic targets now. To be clear, we are not overweight risk assets and not reaching for returns. That’s not to say it won’t happen, but only time and data will tell when.

Meanwhile we will be watching carefully, waiting patiently, and adjusting accordingly as conditions warrant.

—

Victor K. Lai, CFA

You must be logged in to post a comment.