Stocks are set to close on a great 2019. Year to date, global stocks are up well over 20%. US stocks have led and are making new all-time highs along the way. Fed Chair Powell has suggested no more rate hikes in 2020 and President Trump announced a “phase one” agreement in the US-China trade dispute. The good news just keeps on coming.

Ironic, then, that I’m increasingly cautious about the year ahead. Not just because of the current positive news stream, but because I was still quite optimistic this time last year when the stock market slipped into free-fall and while many investors were in panic mode.

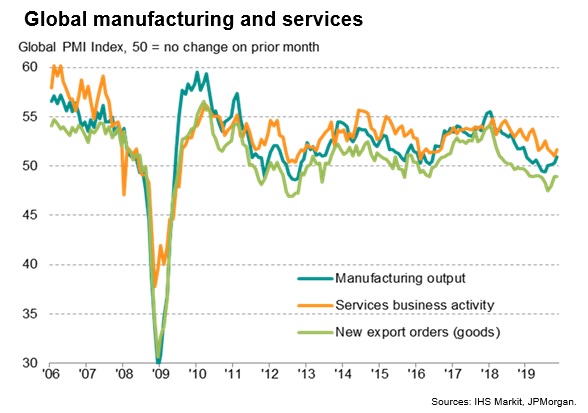

Things are, dare I say, different this time. Last year the Fed was still tightening (due to expected growth), employment was still strengthening and earnings were still growing. The current de-escalation of the trade spat is positive but could be too little too late. Damage to global business activity has already been done, most clearly to exports and manufacturing, but even services have seen a downtrend.

The real concern is whether the weakness in business activity will impact the consumer. As I noted last month, it seems businesses have absorbed much of the trade war casualties through volume, foreign exchange, and profits. But that obviously cannot go on forever.

If circumstances don’t improve, employment and consumption will be next in line to feel the pain. And arguably, those are the very things that have kept our current expansion going. As of now, employment still appears to be holding up. However, Initial Jobless Claims, one of the best leading indicators of employment conditions, may have hit a bottom in April of 2019. A continued uptrend could signal trouble ahead.

And of course, we’ve also seen warning shots from other indicators like the Treasury yield curve. It’s fair to say our outlook has come close to full circle over the past year. From don’t be fearful of a technical sell-off to don’t be greedy at these all-time highs.

For the record, I don’t think we’re headed straight into a recession in the New Year. I don’t yet see enough significant widespread deterioration across leading indicators. At the same time, there are a number of factors that could prolong the risk-on rally. Fiscal stimulus, tax cuts, and a better than expected trade deal are just a few possible surprises given the upcoming election year.

All things considered, it’s impossible to say when the next downturn will strike but we’re clearly 20%+ closer than we were this time last year. Meanwhile, we’re late in the business cycle with valuations and uncertainty high. Historically, not the best environment to be reaching for risk and returns — that succinctly explains our increasingly cautious stance heading into 2020.

Whatever does or does not happen in 2020, this has been a great year for both clients and BCM. On that note, I’d like to say thank you to all our clients and those who support us. We thank you for another year of trust and confidence, something we look forward to building on for years to come. From everyone at BCM, we wish you the happiest of holidays!

Victor K. Lai, CFA

You must be logged in to post a comment.