QUARTER REVIEW

Global equity markets continued their ascend from their Q1 lows. As of September 30, the MSCI ACWI (global stock market) is +1.89% year-to-date. That doesn’t sound like much, but that’s after recovering the -36% peak-to-trough decline from Q1. From that perspective, this year has been nothing short of remarkable.

Figure 1: Global Equity Markets

ECONOMIC AND MARKET CONDITIONS

Economic conditions continue to be “unprecedented.” Extreme deterioration of economic data in Q1 and Q2 have given way to an extraordinary recovery in Q3. For example, Figure 2 shows the magnitude of swings in employment based on US non-farm private payroll data.

Figure 2: US Employment

Likewise, the Treasury Yield curve, which had been teetering above and below the “zero line” since last year is definitively steepening away from inversion, shown below. As a leading indicator, this is a good look for economic conditions.

Figure 3: US Treasury Yield Curve

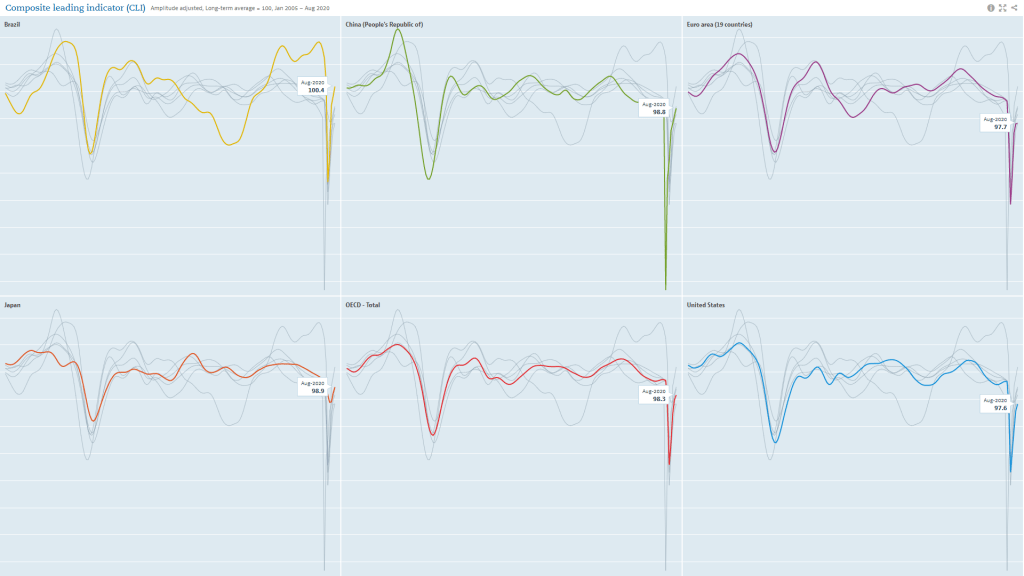

Global economic data are confirming an upward trend. Figure 4 shows Composite Leading Indicators from the OECD for the US, Brazil, China, Japan, the Euro area, and the world. It’s clear we’re seeing a broad and coordinated recovery from the sudden stop of early 2020.

Figure 4: Composite Leading Indicators

Meanwhile, rising market volatility over the past month has some fearing another meltdown. To be clear, nobody knows what happens next, certainly not me. But it’s worth noting how current market conditions contrast with Q1.

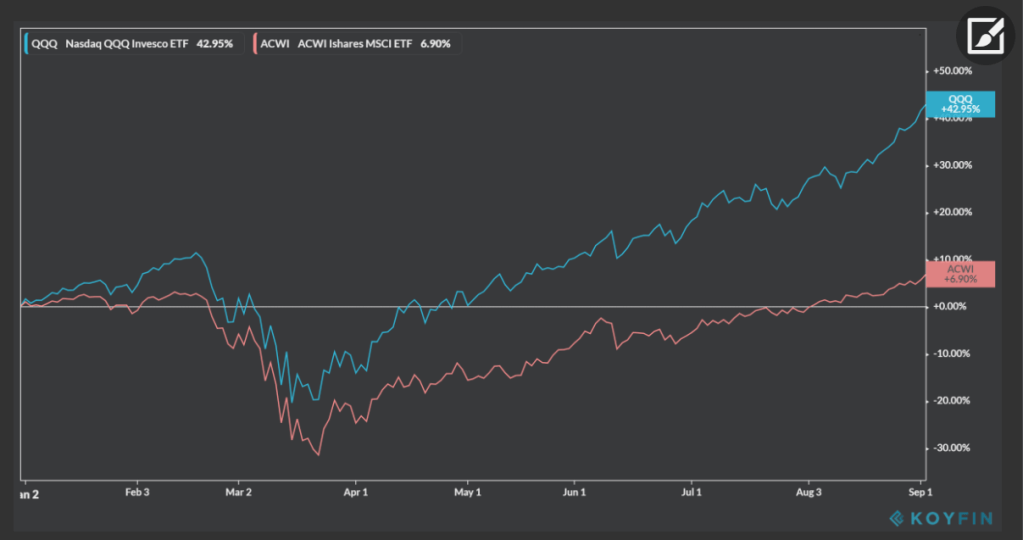

The massive rally since the March lows was led by high-flying tech stocks, shown in Figure 5 as the QQQ (NASDAQ tech stocks) vs ACWI (global stocks).

Figure 5: NASDAQ vs ACWI

The near-vertical moves in some tech names was indicative of an inevitable and necessary correction (at least). We are seeing that reasonable expectation unfold as the sell-off has been led by the same names.

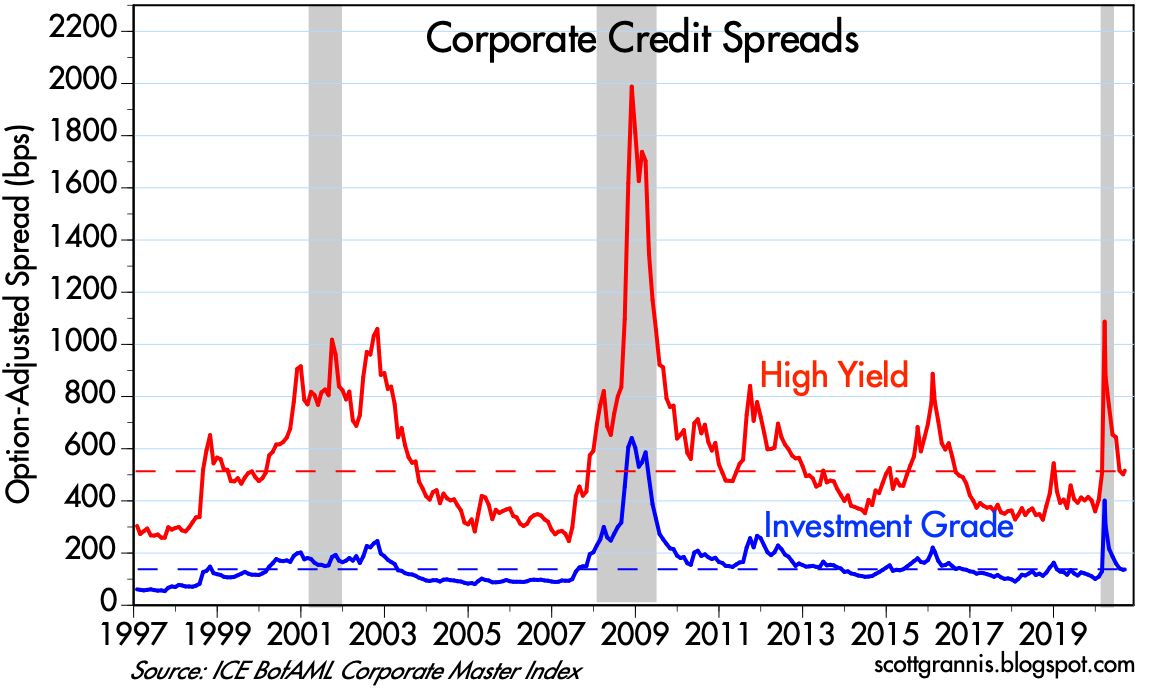

Meanwhile, beneath the surface it appears market conditions have been improving. Figures 6 and 7 show the continued easing of market stress as measured by the VIX and credit spreads, respectively. Admittedly, volatility has picked up in September, but both indicators are clearly well off their March highs and on a downward trend.

Figure 6: S&P 500 & VIX

Figure 7: Credit Spreads

TACTICAL ALLOCATION

In Q3, TA model portfolios moved from underweight to neutral weight and are currently at their strategic target allocations. This is a change from our positioning in Q2. And although we did not expect to adjust so quickly, TA is ultimately data driven and the moves were directed by improving economic and market conditions.

To be clear, there is no shortage of uncertainties and we don’t know what happens next. COVID remains unresolved, it’s ultimate economic impact is unknown, and the US braces for a looming and contentious presidential election. Any of these uncertainties could turn this burgeoning recovery on its head.

In times like these, it may seem irrational to take any risk at all — why not just sit in cash? The problem is interest are rates so low cash practically guarantees a loss in real terms (inflation is currently higher than the return on cash). Zero is a low hurdle to beat and the belief that we cannot do better than a “practically guaranteed loss” over time also seems irrational.

Rationality aside, it’s worth remembering that markets often move on relative terms, especially in the short-run. As I wrote last month, markets can move on whether conditions look relatively better or worse rather than absolutely good or bad.

While it is true economic conditions still look ugly, it can also be true they look less ugly than before. What happens next will be influenced by whether conditions marginally improve or deteriorate. Likewise, our positioning will change based on those conditions.

We cannot predict how or when conditions will change We simply watch closely and wait patiently for the changes to occur. At present, TA is neutral weight risk exposure but will adjust as conditions warrant. We’ll keep you informed of what we’re seeing and doing along the way.

—

Victor K. Lai, CFA

You must be logged in to post a comment.