MARKET SUMMARY

After a strong 2019, global equity markets made an abrupt move to the downside in the past month. Most major stock markets have officially entered into bear market territory and are down between 20% to 30%.

Figure 1: Global Equity Markets YTD Price Returns

With markets already uneasy about slowing economic conditions, the blow from COVID-19 (CV) was enough to wobble knees. The addition of the unexpected breakdown in Saudi-Russian oil talks completed the proverbial “one-two punch” that knocked investors off their feet.

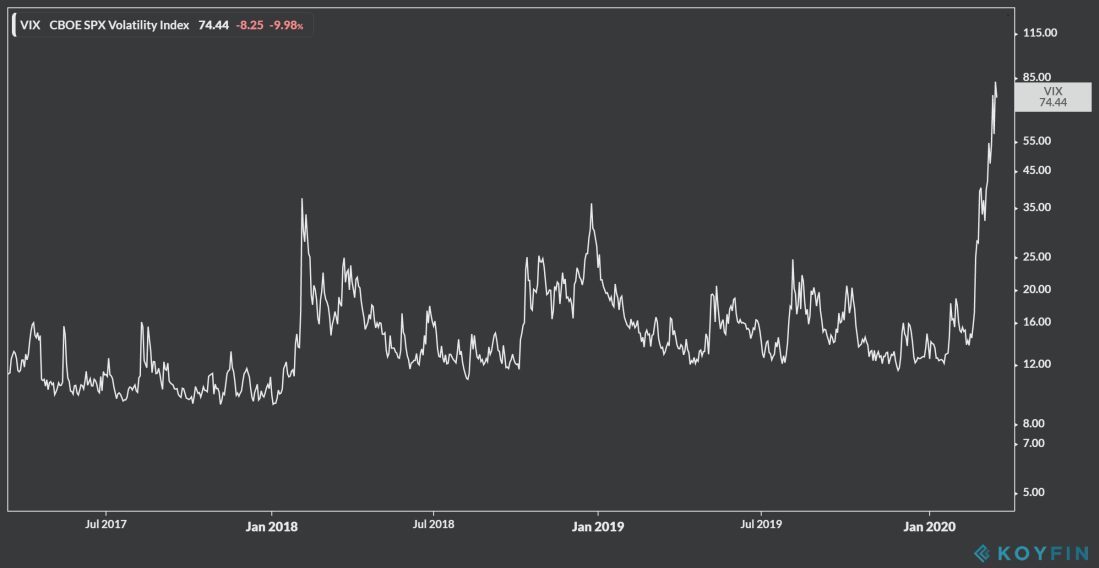

It’s easy to extrapolate this into a worst-case scenario and that’s adding to the angst. Investor fear is palpable and visible in the VIX (aka the market fear index) which briefly touched levels exceeding those of the Great Financial Crisis.

Figure 2: CBOE SPX Volatility Index (VIX)

Although every bear market feels more extreme than the last, in some ways this one actually is. For example, historically it took the US stock market an average of over 10 months (close to one-year) to reach bear market status (i.e. -20%). In 2020, it took the S&P 500 just 22 days, the fastest bear market on record.

Figure 3: S&P 500 Bear Market Statistics Since 1956

The worst part may be the uncertainty of what’s to come. It’s impossible to know what happens next and that’s very uncomfortable to think about. However, it’s important to establish realistic expectations to avoid being caught totally off guard and overreacting.

First, I’m clearly not a healthcare expert, but it’s reasonable to expect news of the CV outbreak to get worse before better. Looking at how CV unraveled in other regions provides an idea of how things may escalate. In the near-term, even if CV is contained increasing testing may still lead to a “spike” in the number of cases. This is not a reason for panic, it’s just setting realistic expectations.

The negative news flow will likely further impact markets. With that in mind, we should recognize the current bear market has not been severe relative to history. For example, the average bear market loss over the past 60 years was -36% (median of -34%), based on the S&P 500. That means current losses haven’t even reached “average” levels. Consider that the US stock market fell more than -50% during the Great Financial Crisis. And during the Great Depression, losses exceeded -80%.

In addition, past bear markets took an average of 10 months to bottom, the longest was 15 months. That does not mean we’re headed for losses of that duration or magnitude, but it is a reminder to anyone already losing their lunch that this roller coaster ride is probably not yet over, and we should prepare our stomachs for more dips ahead.

WHAT INVESTORS CAN DO

I wish we could find cures for both COVID-19 and bear markets, but I suspect we will only discover one. With no cure for market volatility, the natural instinct is to panic. As such, it’s important to remain calm, to view the situation from the right perspective, and to focus on simple, practical actions we can control to influence outcomes.

It’s not a groundbreaking approach, but like the CDC’s public advisory for COVID-19, the best defense in a highly uncertain situation often boils down to simple, common sense recommendations like “wash your hands with soap and water.” Here are some simple suggestions for investors.

- Ensure we have adequate liquidity to meet any near-term needs or obligations. This includes things like cash in bank accounts, money market accounts, short-term time-deposits, short-term Treasury-bills, etc. The assets should be safe and easily convertible into liquid cash on demand (with minimal cost and time). We should have at least several months of living expenses on hand but it really boils down to how much liquidity we need to feel comfortable. Not only will this provide security and peace of mind, but the cushion can help us avoid forced liquidation of longer-term investments under unfavorable circumstances.

- Understand our downside risk tolerance. This is a subjective task, but as the saying goes, we know ourselves the best. It’s important to be brutally honest with ourselves about risk. We tend to focus on the upside to risk (we’re all high-risk takers in that sense), but it’s the downside that really defines our risk tolerance. We need to be very clear about how much downside risk we can really stomach.

- Establish clear objectives and time horizons for our investing activity. We don’t need exact precision, but we need a clear understanding of what we are doing and when. For example, we are investing now because we want to retire in 10 years and live in retirement for 20+ years. These are personal goals so there’s no right or wrong, but we do need to know where points A and B are before we try to connect the dots.

- Last but not least, properly align our investments with our goals, time-horizon, and risk tolerance.

Assuming these actions are performed correctly, we can put things into the right perspective and have an effective system for defending against market volatility.

For example, let’s use the scenario from Point 3 above — we’re saving for retirement that is 10 years away and 20 years in duration (so a total time horizon of 30 years).

Next, let’s assume we’re willing and able to stomach the intermittent volatility of a moderate-risk portfolio, represented by a strategic asset allocation of 60% stocks / 40% bonds.

Now, what if the portfolio falls by -20% after the first year of investing?

To begin with, if we weren’t willing or able to stomach a -20% drawdown, we’ll probably panic and sell to avoid more downside.

However, assuming the portfolio was correctly aligned with our risk tolerance. We could keep calm and use logic and reason to determine the best course of action.

For example, we have an investment horizon of 30 years (hopefully more) with retirement still 10+ years away. In that sense, what may happen today, tomorrow, or next year is less important than what is most likely to happen ten or twenty years from now.

Then compound that with knowing a 60/40 allocation had a 95% probability of success (delivering positive returns) based on 5 year-holding periods as far back as we have data. Based on 10-year holding periods, the success rate was 100%.

In addition, a -20% return is not abnormal and is well within the expected range of 1-year returns (the worst 1-year return being -26%). This is all summarized in Figure 4 below.

Figure 4: Rolling Returns 1928 to 2019

It’s important to recognize the high historical probability of success assumed the portfolio was held throughout both up and down periods. By getting scared out of the market when times are bad (i.e. selling when prices are low) we set ourselves up for being lured back in when times are good (i.e. buying when prices are high). Extreme moves in and out can result in a vicious cycle of short-term mishaps that sabotage an otherwise successful long-term strategy.

The point is if we correctly construct our portfolios to match our circumstances before setting sail, then they can weather the storm of uncertainty that markets and emotions will bring.

For those who may have overreached risk-wise and are now panicking about whether to sell, know that over long-enough periods even a 100% stock portfolio can have a very high success rate (historically, 20 years = 100% success for S&P 500). But again, the key is one must persist through ups and downs to achieve it.

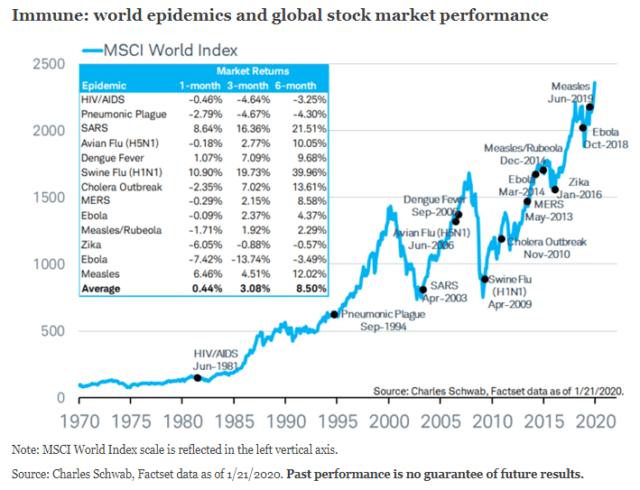

Staying put is a simple concept, but simple is not the same thing as easy, especially when the public is in an outbreak-induced panic. So, for what it’s worth here’s a big picture look at how US stocks have endured past outbreaks over time.

Figure 5

Lastly, seeing the big picture is relevant beyond the markets. COVID-19 is dreadful, but not the first, worst, and certainly not the last pandemic we will survive. I’m not making light of the situation, just saying that in the coming years the vast majority of people will be alive, well, and laughing about that fight over toilet paper at Costco.

WHAT BCM IS DOING

Again, I realize staying put is easier said than done in the midst of a bear market. That’s why at BCM we take proactive measures above and beyond basic strategic asset allocation to help clients manage against downside risk.

Those who understand our approach know we make tactical adjustments to our portfolios. To be clear, we do not try to predict or “time” when markets will move, and we do not make extreme moves that are “all-in our out” of the markets. Instead, we tactically adjust portfolio risk exposures around their strategic targets.

The idea is to be above targets sometimes, below targets sometimes, and to average out near strategic targets over time. Although some managers advocate an “all-in or all-out” tactical approach, we believe staying near strategic targets over time is the best way to stay on the long-term path of success (e.g. the 95%+ probability of positive returns from Figure 4). Meanwhile, the tactical adjustments help us smooth out the journey during periods of intermittent volatility.

Again, I emphasize we are not “market-timing.” We do not attempt to predict when markets will hit a top or bottom. Instead, we simply recognize markets and economic conditions move in cycles. By monitoring economic and market data we can observe whether conditions are getting generally better or worse, accelerating or decelerating.

In other words, we’re not trying to predict when things will happen. We’re just watching carefully and waiting patiently for them to occur, at which point we adjust our risk exposures accordingly. No, it’s not perfect, but it is a practical, rational process based on relevant information instead of fear, greed, and panic.

As an example, in December last year, we noted economic conditions were deteriorating and markets appeared to have come “full-circle” from just a year earlier. We obviously did not know or even expect COVID-19 or an oil shock was coming, but it was apparent we were late in the business cycle, with high market valuations, and facing a rising wall of worry.

That led us to begin de-risking portfolios early this year. Clients saw us begin reducing equity exposure in their portfolios prior to the extreme drawdowns in March. And understanding markets do not fall in a straight line, we were also able to use the oversized market bounces since then as opportunities to liquidate the remaining exposures we needed. At this point, all client portfolios are at their minimum tactical risk weights.

Of course, this certainly does not mean we could prevent portfolios from declining in value, and it doesn’t mean there won’t be more declines ahead. What it means is we are working proactively to manage risk during this downturn and making it less severe than it otherwise would be by doing nothing and just “sitting on our hands” and strategic allocations.

Likewise, when conditions improve, we will tactically increase portfolio risk exposures to benefit from the next cyclical upturn. Precisely timing the turning points is not important. What’s important is having a clear, calm and disciplined process for recognizing when conditions are improving while the consensus is still in a frenzy of fear and panic. To that end, we have such a process in place.

WHEN IT’S ALL DONE

There wasn’t anything new, shiny, or groundbreaking in this post. The main purpose was to reiterate the same boring, but timeless pieces of advice that investors hear during every downturn. I’ll add one more saying that goes there’s little use to worrying about things we cannot control. This applies to many of the headline topics that are affecting our investments right now, like pandemics, recessions, and bear markets.

When all is said and done, we’re better off focusing on things we can control to improve outcomes regardless of what else happens. For individual investors, that means ensuring our investments are properly aligned with our personal circumstances. For professionals, that means having a disciplined process for making investment decisions based on logic and reason instead of speculation and emotion.

These aren’t the most exciting findings, but sometimes boring is better and I think we have all the excitement we can handle for now.

—

Victor K. Lai, CFA

You’re very welcome, same to you and your family, Young.

LikeLike

Thanks for the update. I appreciate your help in looking at the macro of building long term retirement investment as well as making the adjustments in the micro of my investments to minimize the damage of this down turn. Keep up the great work and stay safe.

LikeLiked by 1 person