At the end of the first quarter, the wall of worry was high. Global stocks were down, oil was spiking, and the shadow of the newly erupted war in Iran had investors bracing for a broad drawdown. Cautious positioning seemed not just prudent, but necessary.

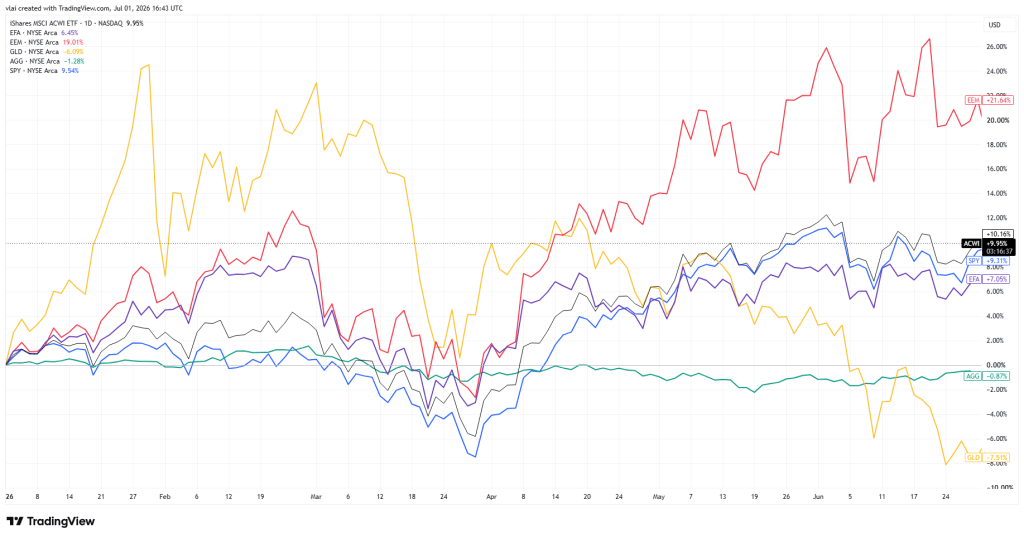

Q2 delivered a textbook reminder of how quickly markets and sentiment can flip. Instead of rolling over, global stock markets staged a massive relief rally. US stocks (S&P 500) blasted off from their late-March lows of around 6,343 to push past 7,380. Global equities (ACWI) similarly rebounded with emerging markets leading the way. Meanwhile, the US bond market (AGG) remained under pressure, and gold surrendered its Q1 luster as immediate panic subsided.

Global Markets YTD 2026

MACRO VIEW

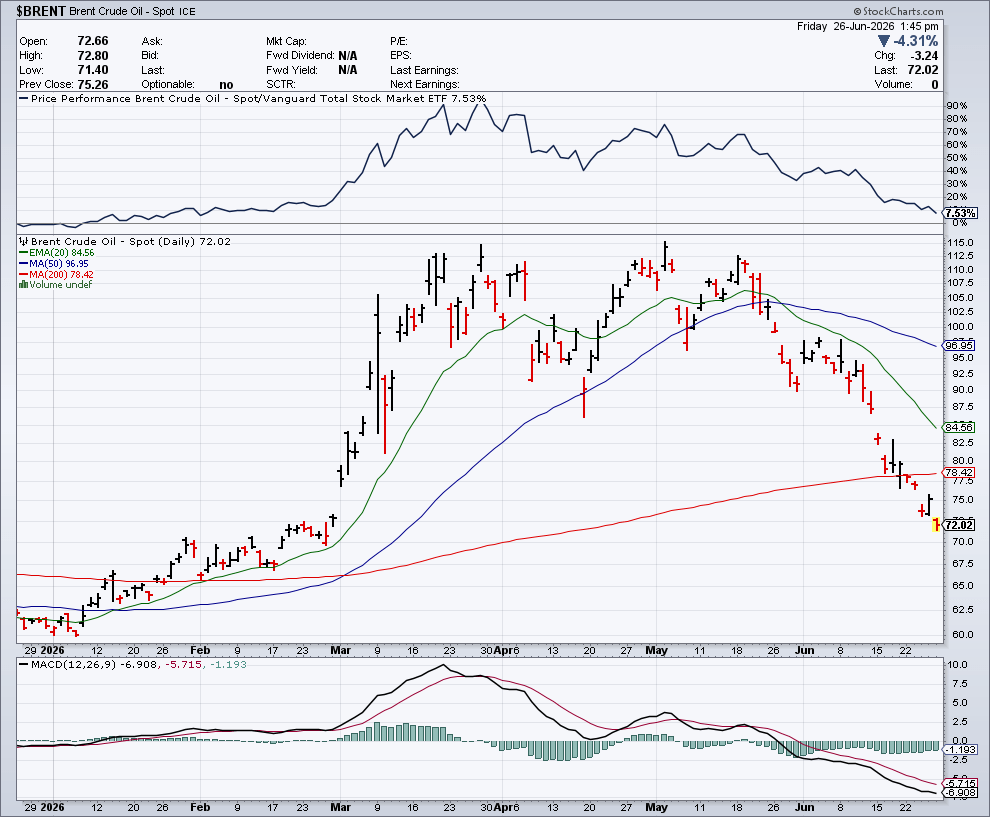

As I wrote last quarter, historically, U.S. wars are not as bad for markets as feared by consensus. At the same time, oil price shocks tend to cause lingering weakness in the economy and the markets. In early April, that risk was front and center as the Strait of Hormuz shut down and Brent crude peaked near $118 per barrel.

Brent Crude Prices

I suggested $100+ per barrel oil prices into the summer could threaten a recession. Fortunately, oil prices plummeted in May and June just before the summer heat, and now prices are bouncing around a $70 handle. U.S. President Donald Trump may be one of the only people (and the most outspoken person) convinced oil prices would fall as quickly as they did.

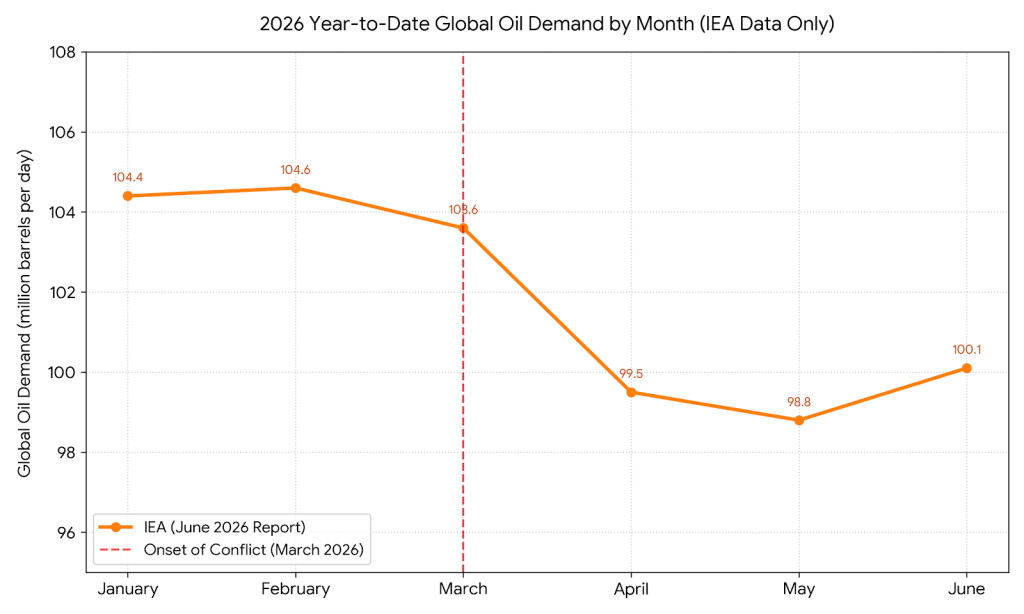

Whether we credit that to clairvoyance, inside information, or the on-again-off-again negotiations, he was right. Yet, as the president takes his victory lap for his deal-making abilities, there’s a detail worth noting. At least part of the price capitulation was due to a decline in demand. Global oil demand fell precipitously in Q2 following the spike in prices.

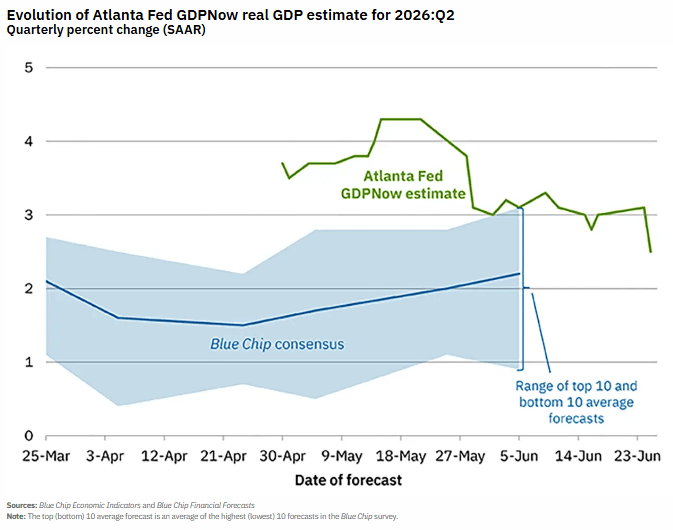

The same downshift can be seen in economic activity. Real GDP growth estimates were marked down from over 4% in May down to a 2% handle by June.

This suggests a classic case of demand destruction, where higher prices became the cure for higher prices, not statecraft or deal-making prowess. It also suggests the U.S. economy is not as robust as the president likes to insist. A booming economy would be more price inelastic, more able and willing to absorb price increases.

That doesn’t mean the U.S. is headed for recession. GDP growth at 2% is still positive, and lower oil prices should help moving forward. Still, this should be a somber warning to keep careless victory laps at bay. Like the Strait of Hormuz, the coast is not yet clear, and the water could still be choppy.

INVESTING VIEW

Markets and investors seem to be in consensus that it’s time to go risk-on. The S&P 500 reached new all-time highs in June, and the AI frenzy was back in full swing, epitomized by the largest stock IPO in history (SpaceX). Meanwhile, fixed-income markets are retreating from rate-cut expectations, and futures are pricing in a “higher-for-longer” environment. Last, but not least, gold prices continue their capitulation from their Q1 highs.

Our conservative positioning in Macro Allocation (MA) worked in our favor during Q1, but it did us no favors in Q2. Fortunately, our overweight of non-U.S. and emerging market equities offset the underweight penalty. Regardless, our objective is not to predict every market swing; short-term market moves are unpredictable by nature.

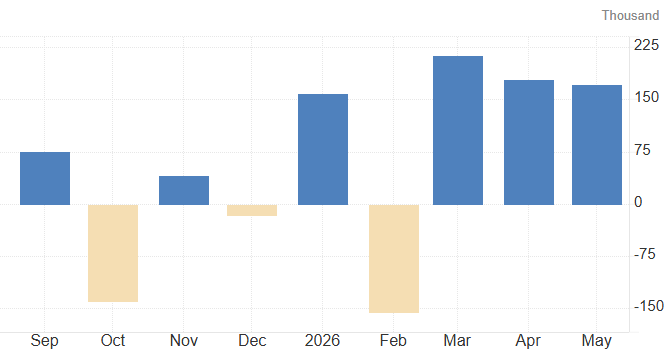

We simply seek to adjust our risk exposure based on currently observed economic and market conditions. As conditions change, so does our positioning. With that in mind, I’ve written for some time that employment conditions are the most important macro considerations to watch. I noted the job market began to show weakness in Q4 and into Q1, with losses in Oct, Nov, and Feb.

Non-Farm Payrolls

Continued deterioration would have been a red flag, but employment conditions bounced back in Q2 with three consecutive positive readings. Yes, the job market of 2026/2025 looks softer than that of 2024/2023 but still shows remarkable resilience and has avoided the breakdown many feared.

Meanwhile, earnings have continued to surprise to the upside. While many analysts expected earnings growth to moderate in 2026, 85% of S&P 500 companies reported earnings that beat consensus estimates in Q1. In aggregate, earnings climbed over 27%, the fastest rate since the post-pandemic surge (consensus was 15% for 2026).

It appears the market train has not only avoided derailing but is also picking up steam. As such, we are re-risking MA portfolios back to neutral risk positions, in line with their strategic targets (up from underweight). We make the adjustments not to chase returns and not because of FOMO, rather simply because data and conditions warrant the change.

At the same time, we refrain from moving to an overweight risk position because we recognize the precarious nature of increasing exposure at a time when market valuations and investor sentiment are elevated, which they still are. Ultimately, our approach for MA is a delicate balance of careful risk-taking and prudent risk management. We continue to do so and will keep you updated with changes as they happen.

—

Victor K. Lai, CFA

You must be logged in to post a comment.