Jerome Powell is near the end of his term as Federal Reserve Chair. No doubt, one of the greatest accomplishments of his term was orchestrating a “soft landing” from what seemed like a near-certain post-COVID recession. Unfortunately, that feat will probably be overshadowed by his infamous “transitory” inflation debacle of 2021. That and his public tussle with President Trump over interest rates.

Powell took a defiant and commendable stand against political pressure to bolster the Fed’s reputation of independence and integrity. Although Powell conceded to some rate cuts in 2025, he eventually paused additional cuts due to lingering concerns about inflation. From an economic perspective, that was the right decision. Yet, that hasn’t stopped President Trump’s theatrical attacks on Powell and the Fed to cut rates further.

In reality, the attacks may be a distraction. While the media focuses on President Trump’s wild outbursts, he quietly placed three out of seven current Fed governors. He’s also on the cusp of placing his hand-picked successor to Powell, Kevin Warsh. With Warsh a ceremonial vote away from securing the Fed’s helm, it seems President Trump has the right pieces on the board and was playing chess with the Fed all along.

Markets likely already suspect this, which helps explain their resilience in the face of so many uncertainties. Rate cuts are generally good for financial markets. Lower interest rates are typically positive for the stock market as they lower financing costs, improve corporate earnings, and “grease the wheels” of the economic machine.

Meanwhile, lower interest rates also typically lead to higher bond prices. That’s due to the mechanics of bond pricing (aka duration). As current rates fall, bonds issued in the past with higher rates naturally increase in price due to investor demand.

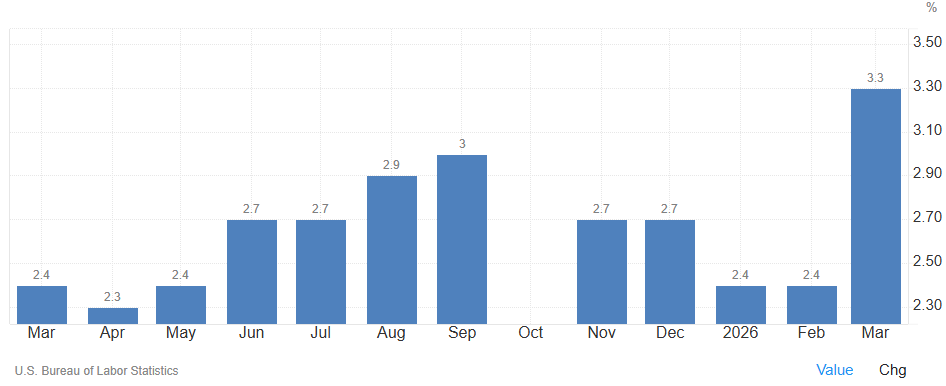

The under-appreciated risk right now seems to be inflation. Remember Powell stood his ground for the sake of thwarting inflation. Even without cutting rates further, the US is already seeing a resurgence in upward price pressure (shown below). That’s likely to get worse in the coming months given the ongoing spike in oil prices.

US Annual Inflation Rate

It’s difficult to argue that cutting rates in this environment wouldn’t lead to even higher levels of inflation. Meanwhile, investors don’t seem to care that higher inflation is bad for financial markets. It erodes the value of future earnings, dividends, and interest payments, leading to lower prices for both stocks and bonds.

Making matters worse, high inflation would eventually force the Fed to reverse course. It would need to raise interest rates, possibly quite aggressively, to bring prices back under control. The combination of high inflation and high interest rates results in the worst scenario for financial markets, where most assets fall in value simultaneously.

Even if the Fed moves to cut rates in an inflationary environment (unusual and unprecedented), we’d likely see a euphoric jump in asset prices first before markets crash against the reality of rate hikes. Of course, that ending is also not certain. Nobody knows what the future will bring. Peace in the Middle East? $50 per barrel of oil? A golden age unleashed by AI? All possible outcomes in a game of investing chess.

—

Victor K. Lai, CFA

You must be logged in to post a comment.