Uncertainty loves complexity

Uncertainty remains high with respect to the economy and the markets. On the one hand, we have a steeply inverted yield curve and a deteriorating housing market. But on the other, we have improving sentiment and a strong jobs market.

The truth is nobody really knows what happens next and we can find data to support whatever narrative we want. With an endless and ever-growing barrage of data points investing quickly becomes both uncertain and complex. For example, here are two opposing viewpoints I currently see in the financial media (traditional and social).

- “The US stock market exhibits seasonality and is typically up in the third year of presidential election cycles.“

- “The US stock market exhibits seasonality and May typically marks a down period, sell in May and go away.”

The sound bytes of “analyses” invoking different stats, figures, and adages are endless. Trying to take them all in is like drinking from a firehose. And even if we somehow consume all the information, the reality is most of it only works sometimes and none of it works all the time.

For example, does it help to consider who is running for president and when? Maybe so, the “Trump rally” of 2017 is often used as anecdotal evidence of how Republicans are market-friendly. However, a more detailed look reveals that the S&P 500 gained an average of 11.2%/yr under Democrat presidents and only 6.9% for Republicans from 1945-2020 (according to Standard & Poor’s). So, maybe not.

Learning to KISS

The takeaway is we cannot remove uncertainty from investing, but we should reduce complexity. As I like to tell myself, learn to KISS, or keep it simple, stupid! Instead of force-feeding every bit of incremental data available into an investment process (which quickly gets too complicated), simplify by eliminating what is unlikely to help and focus on the most important considerations.

For stocks and the stock market, two of the most important, core, fundamental considerations are earnings and interest rates. Earnings represent the profits that companies generate and are the primary reason why equity investors are willing to buy stocks.

When earnings go up, stock prices go up (all else equal). In other words, rational, profit-motivated investors want to buy stocks in companies that will be profitable and want to avoid those that will go bankrupt. Although many different considerations matter to stocks in different situations, earnings matter no matter what.

A second core consideration for stocks is interest rates. Interest rates often represent a real cost for businesses and companies. Higher interest rates equate to higher interest expenses and lower profits (all else equal). But even if a company has no debt or interest expenses, interest rates still matter because they are a fundamental input to stock pricing and valuation.

If we understand that equity investors are willing to buy stocks today for potential earnings in the future, then the timing of those earnings matters. A $100 payment received today is worth more than a $100 payment ten years from now for obvious reasons. Interest rates influence the present value of future payments (time value of money). The higher interest rates are the lower future payments are worth today (all else equal).

A different and easy way to think of this is in terms of a “hurdle rate.” For example, when short-term interest rates are very low (like near 0% in 2021), investors may be more willing to buy risky assets like stocks. That’s because non-risky alternatives like government bonds or savings accounts offer little to no yield and 0% is a low hurdle rate for stocks to beat.

However, when short-term interest rates rise (like 4% to 5% in 2023), the hurdle gets higher for risky assets. Fewer investors may be willing to roll the dice with stocks when they can earn a “risk-free,” guaranteed return of 4% to 5% sitting in Treasury Bills.

The full circle bottom line

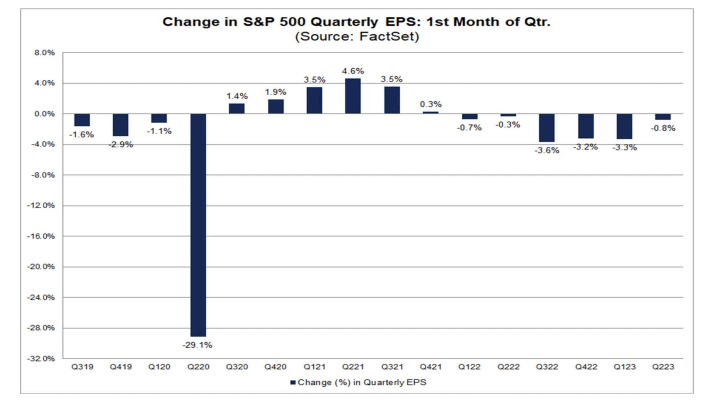

Coming full circle, let’s see how this relates to the U.S. stock market today. Despite breaking headlines about how companies are “beating” earnings estimates, it is worth noting those “beats” were against estimates that were aggressively revised downwards over the past several months. Meanwhile, earnings growth peaked in 2021, declined throughout 2022, and continue to slow in 2023.

We don’t need to pay much attention to interest rates to know they are much higher than where they were last year. The current rate hiking cycle is one of the most aggressive we have experienced in decades.

It doesn’t get much simpler, earnings down and interest rates up is a bad combination for stocks. Does that mean stocks must go down? And is this the only information that’s relevant? No, of course not, anything is possible, and we could probably find alternative data on why stocks will certainly go up from here.

We could probably find data to support any view. But I’ll keep it simple and focus on relevant considerations that we know matter from a rational, logical, and fundamental investing perspective. As of now, the data tells us to be careful with reaching into stocks. That will change, but until it does the bottom line is we remain underweight stocks across our portfolios.

—

Victor K. Lai, CFA

You must be logged in to post a comment.