OVERVIEW

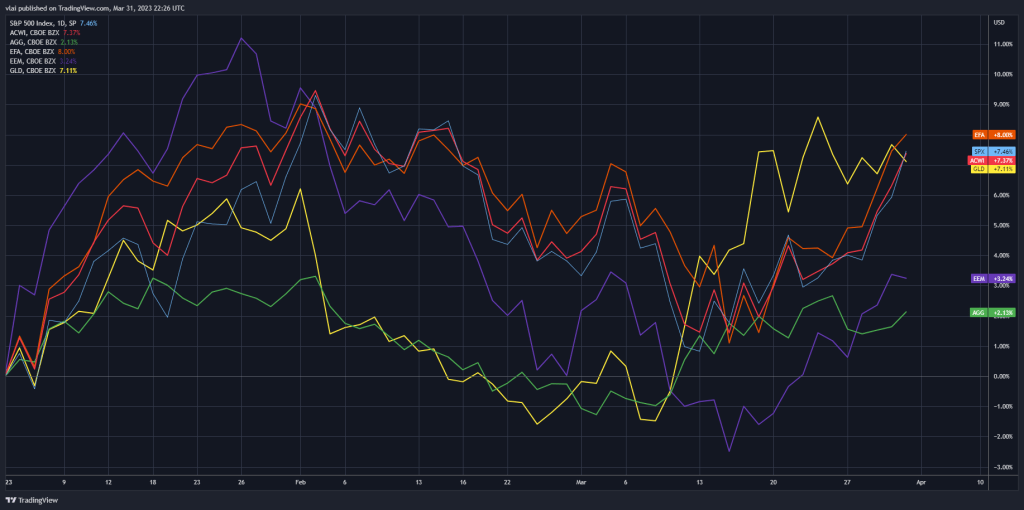

2023 got off to a blazing start. Global stocks were up more than 7% in Q1. That combined with some better-than-expected economic data has investors hopeful that the tide has turned on the bear market of 2022. However, there was no shortage of volatility during the quarter. And if Q1 was indicative of things to come, we can expect more swings into 2023.

Global Markets YTD

MACRO VIEW

After falling for most of 2022, data on business activity surprised to the upside in Q1. The S&P US Composite PMI Index jumped to 50.1 in February and was up for the last two months. 50 is a closely watched level because it marks the threshold between business activity expansion and contraction (above 50 indicates expansion).

Composite PMI

In the U.S., all-important consumer spending held up through the end of 2022 and continues to have support from strong employment conditions. At last count, the U.S. added over 300 thousand jobs in February. As bulls would say, “that doesn’t look recessionary.”

Consumer Spending

Non-Farm Payrolls

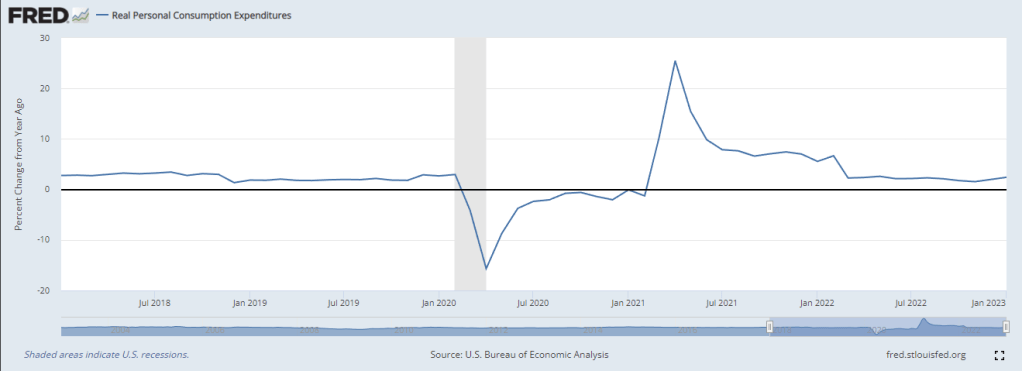

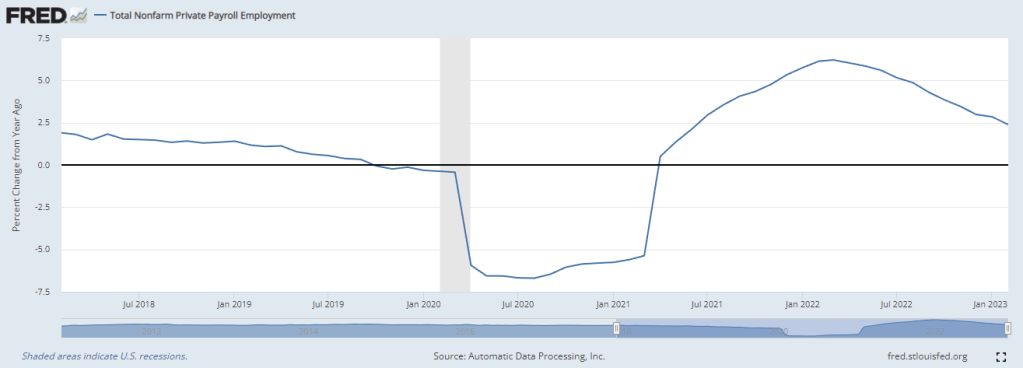

But the glass can also look half-empty. Despite an increase in the dollar amount of consumer spending, the rate of change actually declined substantially off its peak (albeit, from an unsustainable pandemic-induced spike), and ditto for jobs data.

US Consumption Growth

US Jobs Growth

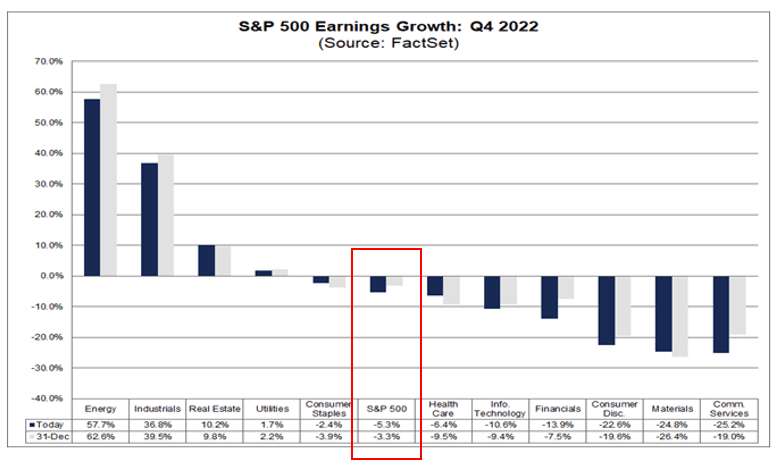

Meanwhile, GDP and earnings have decelerated to a halt, with S&P 500 earnings growth going negative for the first time since the 2020 COVID lockdowns.

US GDP Growth

S&P 500 Earnings Growth

Despite some positive economic numbers to start the year, it is worth noting that even the worst downturns do not happen in straight lines. Overall, the most likely scenario remains what it was last year, a coming recession.

The duress in the banking industry is the most recent harbinger of that eventuality. The failure of Silicon Valley Bank (SVIB) and several others in as many weeks has investors fearful of another Great Financial Crisis (GFC). Anything is possible, but it also seems likely we will avoid a GFC-type of catastrophe.

The GFC was fueled by permanent and catastrophic losses on toxic assets with distressed credit quality. SVIB’s failure was driven by “paper losses” on mainly government securities with little to no credit risk, exacerbated by a mismatch to the bank’s liabilities. Other regionals like Signature Bank and First Republic Bank appear to suffer from similar issues.

SVIB may not be GFC part deux, but it may still mark a pivotal point. Over the past year, markets have been twisting themselves over how high the Federal Reserve (Fed) would raise interest rates. Last year I wrote, “Predicting the exact terminal rate is less important than understanding the Fed will hike until something breaks” (because it always does). SVIB’s failure and the banking sector fallout qualify as something breaking. The question now is what does the Fed do next?

MARKETS & INVESTING VIEW

Investors have patiently wished and waited for the Fed to signal it would pause and even cut interest rates (aka the pivot). In 2022, the S&P 500 repeatedly rallied and failed on speculation about whether the Fed would be tighter or looser than expected.

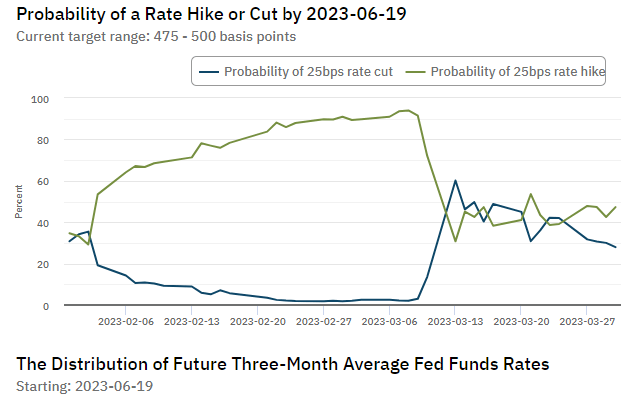

In the wake of SVIB, it seems investors could finally get what they want. Although the Fed still hiked by 25 basis points in March, the chart below shows that market expectations for a near-term Fed rate cut jumped from near 0% to over 50% (blue line). Likewise, the expectations of continued rate increases collapsed from near 100% to below 50% (green line).

Investors cheering for lower interest rates may also be hoping lower rates will bring back the halcyon days of 2021 when markets only went up. Ironically, a Fed pivot may actually be a net negative for markets.

The Fed painted itself into a corner with a hard stance on raising rates to bring inflation down to a self-imposed 2% target. Flipping 180 degrees to cut rates while inflation is still multiples above that target would cripple the Fed’s credibility, already hobbled by its “transient” inflation farce of 2021.

A sudden policy reversal would also flag a reversal of the optimistic narrative the Fed has worked so hard to maintain, e.g. economy is strong, banks are fine, soft landing is manageable, etc. As bears would say, “that doesn’t look good for the markets.” That does not mean markets will not rally on news of a pivot, and actually, they probably will. However, such a rally will also likely be transient after the reality of the Fed’s reasoning sets in.

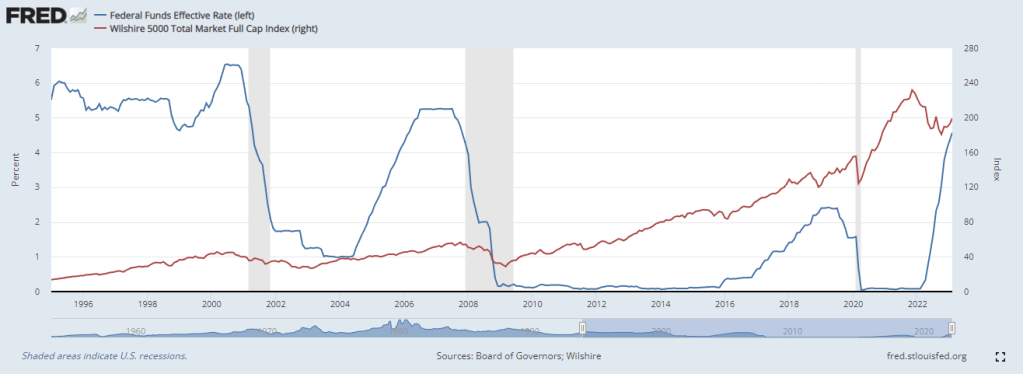

Market history shows stock prices fall after the Fed cuts interest rates. Typically, the worst of major bear market losses happen after rate cuts begin and do not stop until rate cuts are close to an end. The chart below shows how the Federal Funds Rate (blue line) led bear markets in US stocks (red line) during the dot com bust, financial crisis, and COVID downturn. The relationship is not arbitrary. Remember, the Fed cutting rates signal problems ahead.

Fed Funds & US Stocks

The rate cuts will happen one way or another, and whether they happen because of a banking crisis, rising unemployment, or simply a slowing business cycle, there are no positive reasons for rate cuts. For investors, the implication is clear. Be careful what you wish for, a Fed pivot is not bullish for the markets.

At BCM we remain conservatively positioned with a tactical underweight of risk assets like stocks. Our largest allocation is to short-term, high-quality fixed income, like short-term Treasuries and money market securities. With virtually no credit risk, limited interest rate risk, and current yields over 4%, short-term fixed income is relatively attractive in multiple ways.

Within global equities, we prefer non-US foreign markets. I highlighted in BCM’s most recent Investor Letter that valuations are lower in foreign markets, and in some cases, foreign economic conditions are more favorable. For example, leading economic indicators remain relatively positive in Japan versus the US. In addition, the Bank of Japan continues to pursue stimulative policy while the Federal Reserve is committed to tightening in the US.

Composite Leading Indicators

Although markets began this year on optimistic footing, the global economy remains on unstable ground heading into the second quarter of 2023. In the U.S. persistent inflation, slowing growth, and tightening financial conditions are not constructive for a bull market in stocks and risk assets.

Of course, the wall of worry always stands tall while recessions and bear markets, big or small, are always temporary. Long-term investors who manage to hold on instead of leaping from one ledge to another are often rewarded by the fact that markets go up more than down over time.

That does not mean investors should blindly buy and hold forever. It means maintaining an appropriate balance of risk and safety based on current needs and long-term goals. Adjustments can and should be made along the way based on economic and market conditions, but within strategic ranges and limits that keep us in line with objectives (versus all or nothing).

We remain underweight risk assets because current economic and market conditions imply a recession and further downside are still the most likely outcomes. But as SVIB depositors can attest, anything can happen and nothing is really guaranteed, certainly not market forecasts or predictions.

With that in mind, we continue to monitor relevant data and will make adjustments as the information changes. We will keep you apprised of what we are seeing and doing along the way.

—

Victor K. Lai, CFA

You must be logged in to post a comment.