Storied debt ceiling games

Once upon a time, the U.S. government imposed a limit on how much the country could borrow. A debt ceiling was a prudent idea and a good story, but in reality, that ceiling was breached countless times since its inception.

In January of this year, the U.S. broke above the most recent limit of $31.4 trillion dollars. As politicians play a game of chicken with default, the U.S. Treasury expects the country may be unable to meet all of its obligations as soon as June 1, 2023.

That includes interest and principal payments on U.S. Treasury securities (or bills, notes, and bonds issued by the U.S. Treasury, and backed by the full faith and credit of the U.S.).

Why it matters for markets

That matters to global financial markets because U.S. Treasury securities are considered to be the world’s risk-free security. The U.S. has never missed a Treasury interest or principal payment and investors all around the world assume it won’t.

Because Treasuries are perceived as “risk-free,” markets and investors use Treasuries as benchmarks for other investments. For example, if a Treasury bond guarantees an interest rate payment of 3% per year, then another bond that is not risk-free should offer a higher rate.

Virtually all financial markets and assets are priced and valued in similar relative terms, anchored by a perceived risk-free rate. If that anchor is suddenly uprooted, market chaos would ensue as the prices and values of everything are called into question.

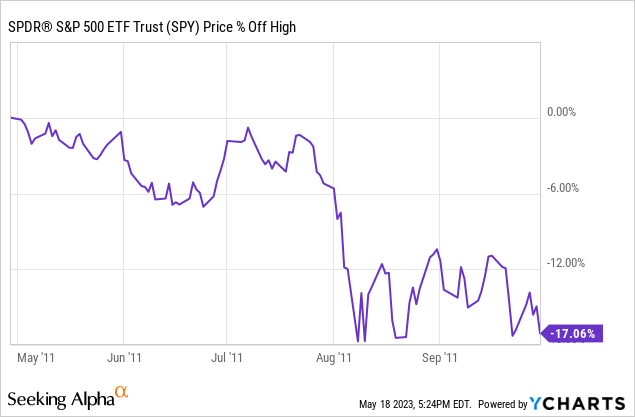

That hasn’t happened, but the U.S. has come close to default. The last time was during the 2011 debt ceiling negotiations. The government got so close to default that credit rating agencies like Standard & Poor’s stripped the U.S. of its coveted AAA credit quality (the U.S. was downgraded). The S&P 500 was down some -17% during that debacle, shown below as the SPDR S&P 500 ETF.

S&P 500 2011 Intra-year Draw Down

What could happen

Just because a default “never happened before” doesn’t mean it won’t happen. That begs the question, what happens if default does happen? It would be chaotic for sure, but may not unfold as some people expect.

It’s reasonable to assume that if there is a default on Treasuries, then Treasury rates should rise (because they are perceived as riskier) and Treasury prices should fall (because prices and rates have an inverse relationship; when rates go up, prices go down and vice-versa).

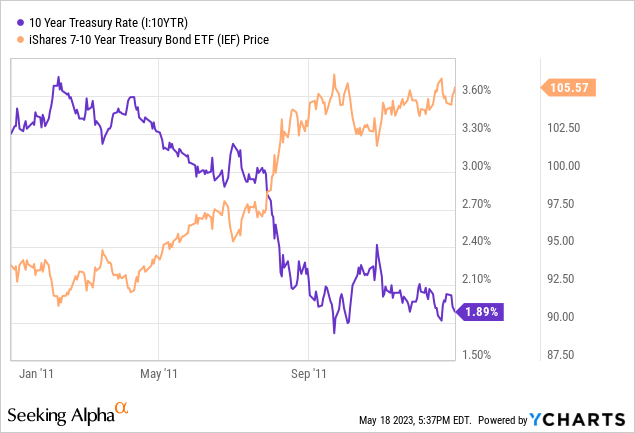

But looking at past market reactions, that might not be the case. Again, default hasn’t happened before, but the 2011 episode was a close call that did result in an increase of perceived risk in U.S. Treasuries vis-a-vis the downgrade of U.S. credit quality.

Global financial markets responded adversely to the news, as expected, but U.S. Treasury yields went down instead of up. The chart below shows the drop in 10-year Treasury yields (purple) and the rise in intermediate-term Treasury prices (orange), shown as the iShares 7-10 Year Treasury Bond ETF .

Despite the downgrade in credit quality and increase in perceived risk, Treasuries still did well because markets often behave in relative terms. The thinking is if Treasuries are riskier, then so is everything else. In that case, investors may still prefer the cleanest dirty shirt in the hamper.

Also, while “default” sounds catastrophic, there are different degrees to such an event. For example, the U.S. making late payments on some of its obligations due to political dysfunction is different from the U.S. being unwilling or unable to pay its debts. Both would be bad, for sure, but most investors understand we’re dealing with the former scenario, not the latter.

In addition, there is a matter of practicality. The U.S. Treasury market is by far the largest, deepest, and most liquid financial market in the world, especially when it comes to assets perceived as relatively safe.

For example, although German government bonds (Bunds) have a higher credit quality than U.S. Treasuries, the Bund market is estimated to be less than $2 trillion in size (Bunds outstanding). In comparison, the U.S. Treasury market is estimated to be over $24 trillion in size.

That makes the Treasury market one of the only “safe” markets that can realistically accommodate the large institutional investors that dominate bond trading and investing. In other words, the U.S. Treasury market is not only the least dirty shirt, but also the most wearable.

The dirty bottom line

Ironically, if the U.S. comes close to missing (or really misses) payments, Treasury yields could actually fall in the short run as investors rush into the assets perceived as most practical and relatively safe.

I’m not downplaying the consequences of a U.S. default. If it happens, it will have serious negative consequences for the U.S. Not only would stocks fall on the news, but it would eventually result in higher interest rates on Treasuries and other debt that could lead to a downward spiral.

As rates rise, the debt becomes more difficult to service, refinance, and possibly even repay at some point. Meanwhile, markets and investors will eventually seek out alternatives just as other countries and technologies seek to replace the U.S. dollar and Treasuries as the world’s reserve assets. That is a catastrophe the U.S. should avoid at all costs.

The solution is a simple truth that is not easy to accept. The U.S. must collectively recognize it has a debt problem and stop spending money it does not have. The U.S. must accept that getting out of this mess means everyone must take less (benefits) and give more (taxes). It’s either that or the U.S. can play dirty and just default.

—

Victor K. Lai, CFA