QUARTER IN REVIEW

Q1 was a bumpy ride for investors. Global equity market prices (MSCI ACWI) swung from being down almost -13% to only down about -6% for the quarter. However, the negative returns were broad. All major equity regions and even the US bond market were down YTD.

Figure 1: Global Markets YTD

MACRO PERSPECTIVE

So far, 2022 has indeed been a year of transition. This was expected, heading into the year we already faced the triple threat of declining fiscal stimulus, tapering of QE, and rising interest rates.

During the quarter, uncertainty spiked higher with Russia’s invasion of Ukraine (a topic I will explore in another post). In addition to the humanitarian crisis and the threat of global military conflict, there are macroeconomic spillovers as well. For example, crude oil prices shot up above $100 a barrel on fears of global supply disruptions, adding stress to an already fading expansion.

Figure 2: Brent Crude Oil Prices

Figure 2 shows that prior oil price spikes are typically short-lived but often correspond with recessions (shaded grey). This was true for the tech bubble (2000), the great financial crisis (2007), and even the pandemic (albeit to a lesser extent).

That doesn’t mean a recession is imminent. 2010 to 2015 saw a period of elevated oil prices with no recession. Economic data often give false signals on their own, but their signals become more reliable when we observe uniform trends developing across a broad range of leading indicators.

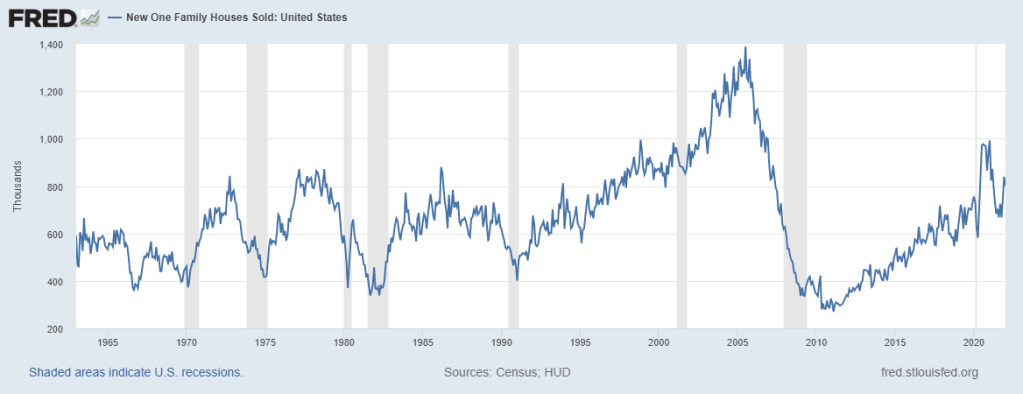

Two such indicators I’ve written about several times over the past year are homes sales and the Treasury yield curve. Historically peaks in home sales and inversions of the yield curve have both led US recessions.

At last measure, new home sales look to have peaked last year, and the yield curve is within basis points of inversion. The 2-10 Year Treasury curve temporarily inverted this week, and other segments of the curve (e.g. 3/5 – 10) had already inverted before that.

Figure 3: New Single Family House Sales

Figure 4: US 2-10 Treasury Spread

To be fair, some economic data weaknesses can and should be attributed to lingering COVID and the outbreak of Omicron last year. Housing was certainly impacted by supply chain breakdowns and material shortages.

As for the Treasury yield curve, some argue things are “different this time” because of the Fed’s unprecedented tampering with the bond market (i.e. QE).

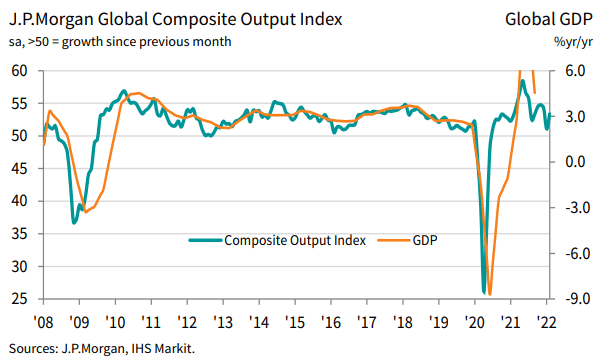

Meanwhile, not all data points are weak. Global PMI readings staged a comeback in February signaling a rebound after flirting with contraction in January.

Figure 5: Global PMI

In addition, all-important employment has remained persistently strong throughout the pandemic recovery. This is particularly encouraging for consumer-driven economies like the US.

Figure 6: US Employed Persons

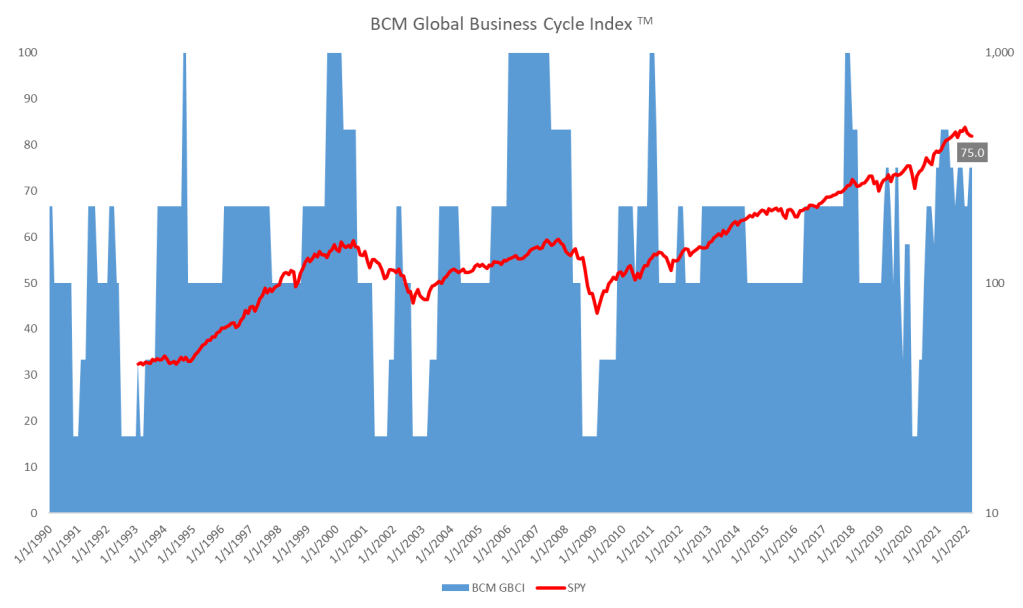

The quarter-end rebound in global financial markets suggests investors believe spring marks the end of a temporary winter lull. Global economic conditions, as measured by the BCM Global Business Cycle Index TM rose to 75 in March (from 66.7 in February). Still off last year’s peak, but also some relief from what was a downward trend.

Figure 7: Global Business Cycle

INVESTING COMMENTARY

At BCM we moved to a modest underweight position in risk assets in March. The decision was driven by changes in economic and market conditions. The existing concerns already noted above were exacerbated by the escalation in the Russian/Ukrainian conflict and its spillover effects.

Meanwhile, we also observed deteriorating market conditions including negative price trends across global markets, weakening breadth and momentum within markets, and decreasing market liquidity with rising implied volatility.

Technical market weakness on its own does not necessarily mean a market crash. But when that weakness is combined with deterioration in fundamental economic conditions, the risk of large drawdowns increases.

Overall, recent changes in economic and market conditions led us to believe a modest reduction in risk exposure was prudent and we used market strength late in the quarter to reduce our positions in risk assets.

Note, we are not at a maximum underweight risk position. We would do that when economic and market conditions exhibit further and significant deterioration. In that sense, this adjustment was a pre-emptive risk management maneuver that will help us move more quickly into a max-underweight position when the need arises.

At the same time, we are fully aware we could be wrong. The unprecedented, globally coordinated stimuli of the past two years will have lasting ripple effects on markets and economies. We recognize even tired markets can catch a second or third wind. In that case, we would need to quickly re-risk and play catch-up.

Only time and data, not timing, will tell what happens next. Although we do not know how conditions will change, we know they must. Meanwhile, we watch carefully, wait patiently, and will respond accordingly when they do. Based on what we see right now, a modest underweight position in risk assets is the most prudent and appropriate adjustment.

—

Victor K. Lai, CFA

You must be logged in to post a comment.