In January, I wrote BCM was entering 2022 with a reduction in our tactical risk allocation, moving to neutral weight from last year’s overweight position. That was a fortunate and timely call given the weak start to this year for risk assets.

The rationale was the tailwinds that supported equity markets in 2020 and 2021 were transitioning into headwinds. Where there was unprecedented stimulus before, there is declining fiscal support, tapering QE, and rising interest rates now. Throw in hot inflation and tensions in Eastern Europe and we have a global equity market that is down about -8% year-to-date.

Figure 1: ACWI YTD Return

Despite all the talk about a market “crash,” global stocks have not even reached the technical definition for an average correction of -10%. Anyone losing their lunch over year-to-date moves should understand the real ride hasn’t even begun.

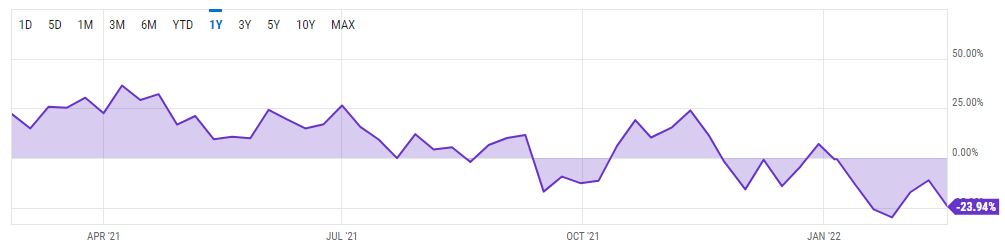

Of course, some market segments have really moved. The NASDAQ is down over -17% YTD and a number of high-flying tech stocks have capitulated and reversed some of the irrational exuberance we saw in markets during the pandemic.

Figure 2: Tech Getting Rational

The pullbacks are healthy and necessary. Parabolic moves to the upside are unnatural, unsustainable, and cause problems for everyone except the fortunate few that manage to sell at the top.

The problem, as always, is distinguishing a run-of-the-mill correction from a more severe bear market or an outright crash. Based on sentiment, a majority of individual investors expect markets to get worse and are near the most bearish levels of the past year.

Figure 2: Investor Sentiment

Figure 3: Historical Investor Sentiment

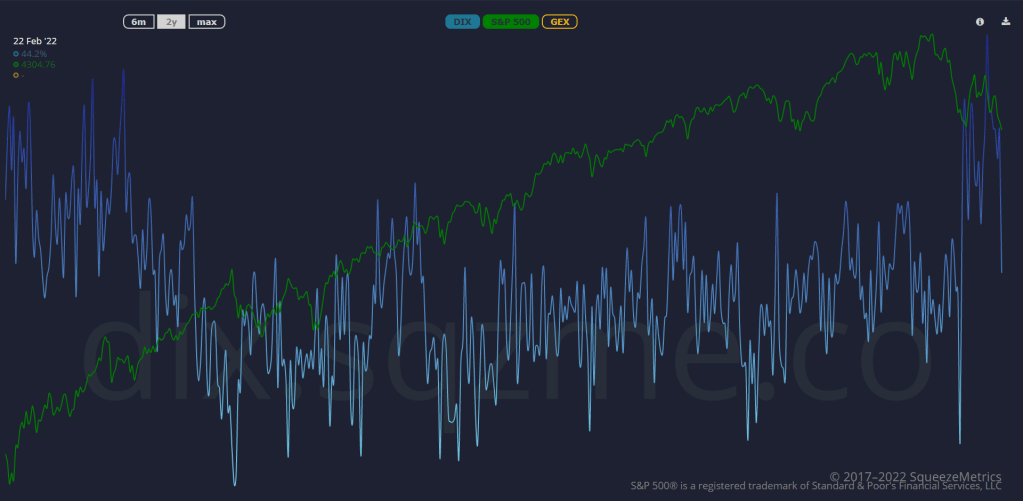

Some would consider this to be a contrarian indicator. Institutional buying activity in dark pools shows the “smart money” was accumulating stock as markets sold off in January and February, shown as DIX below. That could have just been dealers adjusting their hedges. Regardless, today was an exception that saw a sharp reversal into risk-off positioning as Russia moved into Ukraine.

Figure 4: Dark Pool Activity

Arguments can be made either way and it’s too early to declare a verdict. Regardless, I maintain 2022 will be a year of transition. A major theme I wrote about in 2021 was a moderating economic expansion. At this point, it’s highly likely global growth peaked in Q2 2021 and it has been moderating since. The BCM Global Business Cycle Index TM currently reads 66.7 on a scale of 100. We are not in contraction but are on the way.

Figure 5: Global Business Cycle

The “way” can take longer than expected, dragging on for months and even years while investors ask are we there yet? Just ask those who have been sitting in cash since March 2020 (or better yet March 2009) waiting for the “real” crash.

Investing is inherently uncertain and nobody knows what the markets will do next, or when. The best we can do is carefully watch relevant data points and move when they tell us to. More often than not the data say to do nothing but wait patiently and that’s okay. It’s not perfect but it’s a disciplined process based on facts, logic, and reason that beats (most of the time) sporadic, irrational moves driven by fear, greed, and speculation.

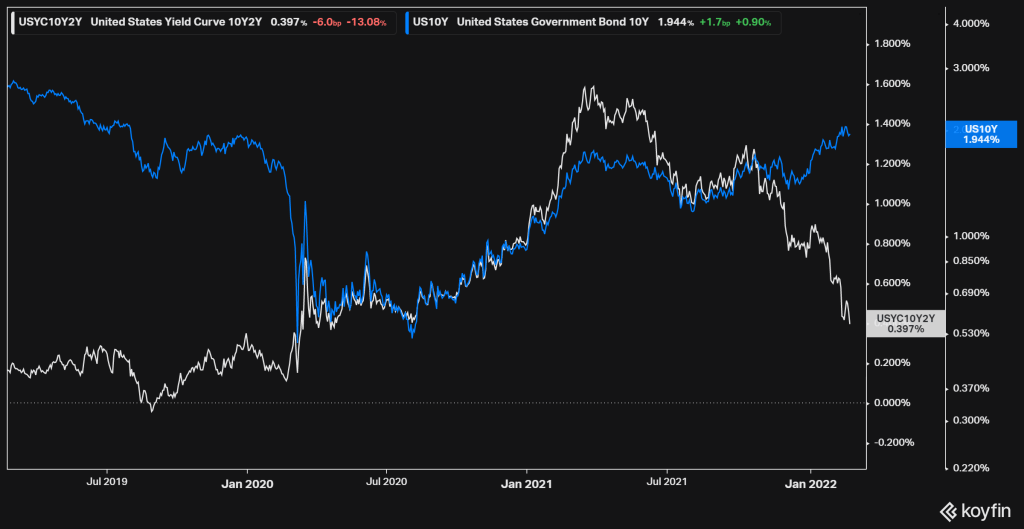

Some data points I have been watching closely are Treasury yields. I wrote in December the 10-year Treasury yield was curiously declining and threatening a potential yield curve inversion. Ironically, 10-year yields shot back up as soon as I wrote that! But even as yields rose, the spread between 10 and 2-year yields continued to narrow and is now less than 40 basis points from inversion. In other words, the yield curve did flatten and a potential inversion is still in play (which was my primary concern).

Figure 6: 10-2-Year Treasury Yield Spread

If we see an inversion of the yield curve, corroborated by deterioration in other leading indicators (employment, cyclical sectors, etc.), and a breakdown in financial market conditions then we will have seen all the data we need to move full-on risk-off. Meanwhile, it’s a simple matter of watching, waiting, and occasionally wondering “are we there yet?”

—

Victor K. Lai, CFA

You must be logged in to post a comment.