I wrote several times this year about my preference for international equities versus US. In August, I pointed out the selloff in Chinese stocks looked like an overaction. The Chinese market is up about +10% from its August lows. My timing was lucky, but there are still many long-term reasons to be bullish on Chinese equities.

There are obvious and significant near-term risks for big red that will cause heightened volatility, so broader emerging market equity exposure might make more sense for some investors. For what it’s worth, EM as a group still looks relatively undervalued versus the ROW.

Figure 1: Market Multiples

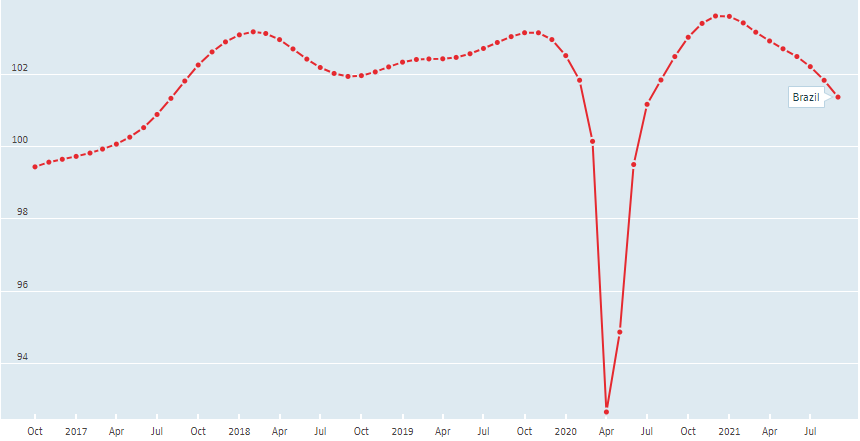

Within EM equity China is actually not the most attractively valued. That distinction goes to Brazil, and its valuation has become even more relatively attractive following an -11% decline over the past week. Brazil is down about -18% YTD and by over -30% from its June high (represented by EWZ in Figure 2). That’s earned Brazil another distinction as the world’s worst-performing equity market in 2021 (by country).

Figure 2: EWZ vs ACWI Price Performance YTD

There’s no extraordinary reason for the price action. The reasons are mundane by today’s standards. Brazil’s government is corrupt, incompetent, and dysfunctional (sound familiar?). The current administration botched its response to the pandemic. Brazil suffers from some of the worst COVID-19 fatalities in the world. Some lawmakers have gone as far as accusing President Bolsonaro of war crimes for advocating herd immunity.

Beyond COVID’s devastating effects, Brazil’s finances are also in disarray. Account deficits are rising and government debt is soaring at a time when fiscal stimulus is in demand (again, familiar?). Inflation is obviously on the rise, sending interest rates higher, spooking investors, and putting downward pressure on the Brazilian Real.

Figure 3: Brazil Debt/GDP

Figure 4: Brazil Inflation

This has the hallmarks of a classic emerging market death spiral, and so all the doom and gloom surrounding Brazil is understandable. However, these issues are not unique to Brazil and despite the current overcast, there is a brighter horizon. Unless Brazil becomes a failed state, it will recover and investors will refocus on the country’s more positive distinctions.

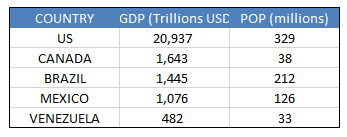

For example, not only is Brazil the largest economy in South America, it’s actually the third-largest in all of the Americas. Brazil also has the second largest population. In other words, Brazil’s economy is larger and more significant than is commonly recognized (it’s not going away).

Figure 5: Largest Economies, Americas

And despite the problems, Brazilians are getting back to work, spending their money, and creating a rebound in economic growth.

Figure 6: Brazil Non-Farm Payrolls

Figure 7: Brazil Consumer Spending

Figure 8: Brazil Annual GDP Growth Rate

To be fair, the rebound in GDP was really a side effect of the pandemic, is not sustainable, and is already slowing, which is part of what’s spooking markets.

Figure 9: Brazil Change in GDP

Pessimism about Brazil is still pervasive and there’s a good chance it’s still too early to buy. If economic conditions deteriorate there will be further downside ahead. I’m not calling a bottom for Brazilian stocks and I’m not trying to, I don’t know when the market will bounce.

What I do know is that in a world of extremely rich valuations, Brazil stands out as the most reasonably priced market in the most reasonably priced segment of global equities. That this value is found in one of the world’s growth darlings (past and future), the very “B” in “BRIC,” is a distinction worth attention.

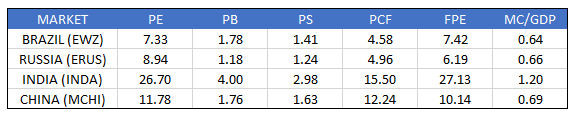

Figure 10: EM Multiples

Brazil may be “cheap for a reason,” but like COVID, those reasons will pass. Keep in mind Brazil doesn’t need to nail a perfect landing, it simply needs to get up and perform less bad than expected. Right now expectations are low.

Meanwhile, taking a step back from the current selling puts the volatility into perspective. The bigger picture suggests the current drawdown is nothing out of the ordinary and may just be another leg down within a longer-term uptrend off the bottom in Q1 2020. Time, not timing, will tell.

Figure 11: EWZ Price

Again, I don’t know if Brazilian stocks have found a bottom. But I’m confident a long position in Brazil at current prices or better will be rewarded over time. I lack the audacity to pick single Brazilian stocks, but I estimate appreciation of ~60%+ for a broad Brazilian equity market fund like EWZ and am building a long-term position on price weakness. If you take a position, do your homework first, and don’t bite off more than you can stomach.

—

Victor K. Lai, CFA

Disclosure: Victor Lai is long EWZ.

You must be logged in to post a comment.