Many things about China don’t make sense in the West. It’s not just food and politics, but markets too. In China market quotes flash red on upticks and green on downticks. In the wake of the pandemic Chinese stocks led a global rebound with an outstanding rally few expected. But fortunes turned again quickly. The Chinese stock market dropped more than 30% from it’s high and is now negative over the past year (shown as MCHI vs ACWI in Figure 1).

Figure 1: MCHI vs ACWI

The flip-flop has investors scratching their heads in frustration. What’s causing the back and forth? Last year, China was not only the first to deal with COVID, but was also very aggressive, leading to a pronounced economic recovery (Figure 2).

Figure 2: China Composite Leading Indicator

This year, Chinese stocks are weighed down by at least a couple of concerns. First, last year’s economic bounce seems to be losing momentum. China’s latest manufacturing PMI data fell to a YTD low and has been on a downtrend all year (Figure 3).

Other economic data including industrial production and retail sales have also come in weaker than expected. The Chinese government maintains a generally positive outlook but concedes the resurgence of COVID outbreaks and external factors are contributing to an “uneven and unstable” economic recovery.

Figure 3: China Caixin Manufacturing PMI

The second and more prominent issue (at least by the headlines) was an apparent crackdown by the Chinese Communist Party (CCP) on private sector enterprise. The CCP very publicly took down one of China’s most famous billionaire entrepreneurs (Jack Ma) for being critical of the party. The CCP also went after at a number of China’s most iconic tech bellwethers including JD.com, Tencent and DiDi.

It’s unknown whom the CCP is targeting next, so investors are avoiding the line of fire by selling first and asking questions later. But now that we’re here, let’s take a step back, look at the bigger picture, and ask why China would punish it’s own national champions?

There are conspiracy theories ranging from personal vendettas to the CCP targeting companies that listed on foreign exchanges. I don’t know these theories to be untrue, but I don’t think they provide adequate explanations.

I think China is simply struggling with some of the same issues we face in the US. For example, the increasing concentration of power among a few corporate behemoths and a growing divide between rich and poor. The CCP saw too much “excess” in the system, growing social unrest, and decided it was time to act.

We can criticize the CCP’s methods and it’s disregard of freedoms and rights, but economically the CCP is not crazy. Allowing a handful of corporations to consolidate too much wealth and power can stifle competition, create inequality, and systemic risk.

It’s not sustainable and is actually detrimental to long-term growth and innovation. We recognize the same concerns in the US with a never-ending litany of anti-trust and consumer protection suits waged against our domestic tech giants.

The point is the CCP is not trying to destroy it’s corporations, rather it’s trying to create more balanced and sustainable long-term growth. To be fair, the CCP is also likely making a statement about about power and control (and admittedly, Jack Ma’s case has shades of conspiracy).

We may not agree with the CCP’s approach, but I don’t think its “crackdown” makes Chinese stocks untouchable. It certainly makes them more uncertain in the short-run, but it could also improve market stability in the long-run.

As for weakening economic conditions, the data is more mixed than recent headlines imply. While manufacturing PMI did fall, the services PMI actually rose sharply in July (Figure 4).

Figure 4: China Services PMI

Meanwhile, other data points like exports and corporate profits have continued to recover and move in the right direction (Figures 5 and 6, respectively).

Figure 5: China Exports

Figure 6: China Corporate Profits

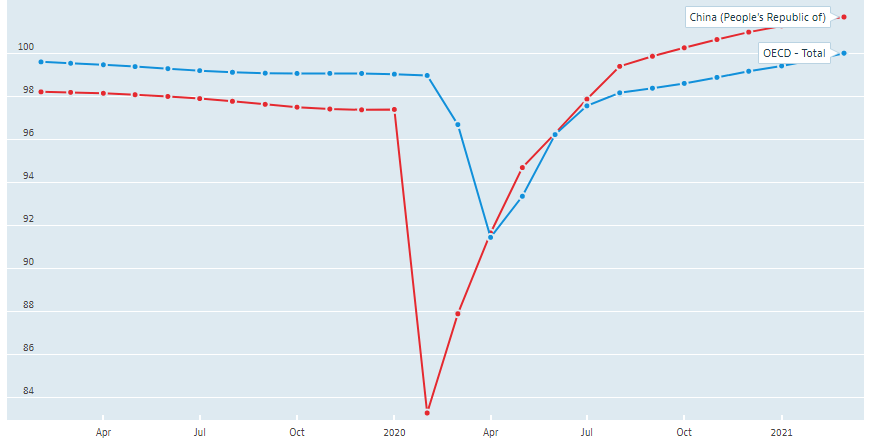

And let’s not forget that in a world of dubious market choices, relatively “better or worse” can be more important than absolutely “good or bad.” Despite it’s issues, China has the third strongest leading indicators among all countries monitored by the OECD.

Figure 7: Composite Leading Indicator by Country

Also relatively speaking, the Chinese stock market looks undervalued versus the global market, and certainly versus the US. Not so compared with emerging markets, however, EM in aggregate (including China) still looks undervalued vs global stocks. To be clear, nothing looks unreasonably undervalued, China just looks relatively not as expensive.

Figure 8: Market Valuations

And of course Chinese stocks are far from a “sure thing.” Particularly near-term, the economic data is mixed and changing, and the whispers of debt problems are getting louder. I don’t know if Chinese stocks have found a bottom. If economic conditions weaken or we get a negative shock China will see further downside. And regardless, Chinese stocks are notoriously volatile in any case.

All that said the Chinese market was already relatively attractive versus global equities earlier this year. Now after a 30% haircut even more so. Red or green, there are many reasons to be bullish on Chinese stocks in the long-run. So bottom or not, the current pullback is an opportunity to build on a long-term position.

If you decide to go long, do your homework, buy on weakness over time, and don’t bite more than you can stomach.

—

Victor K. Lai, CFA

Disclosure: Victor Lai is long MCHI.

You must be logged in to post a comment.