In October, the US printed weaker than expected GDP growth. The first reading was 2% year-over-year versus a consensus forecast of 2.7%, which itself was already well below Q2’s 6.7%. This corroborates the “moderating growth” narrative of the past two quarters.

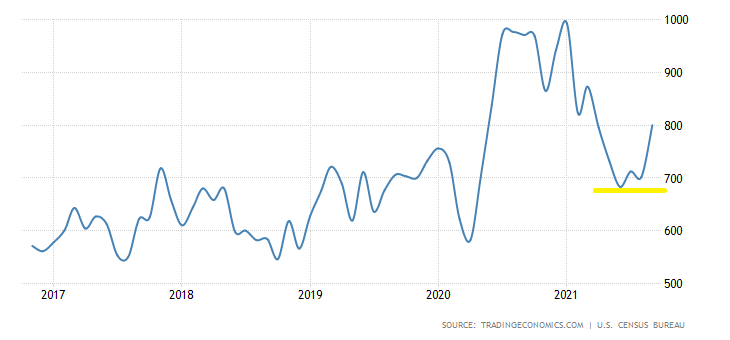

That doesn’t mean we’re on the cusp of a double-dip recession. Actually, some economic indicators that were flashing yellow earlier this year have turned around. For example, new home sales recently bounced off a steep slide from their January highs.

Figure 1: New Home Sales

Meanwhile, global PMI numbers are back to expanding after almost falling into contraction territory in August.

Figure 2: JPM IHSM Global Composite PMI

It’s probably not a coincidence the weakness in economic data coincided with the Delta variant surge that began in May. And coincidentally (or not), that surge appears to have peaked in September.

Looking ahead we have pent-up demand unleashing into the holiday season and a massive infrastructure bill that will feed into momentum for the rest of the year. Even without those considerations, the market exhibits seasonality on its own.

For what it’s worth, historically the period from August into October is weak for the stock market while the final months of the year are strong. For example, S&P 500 returns have been positive in the fourth quarter almost 80% of the time since 1950, also known as the “Santa Rally” effect.

Figure 3: S&P 500 Seasonal Returns

Does that mean it’s time to throw caution to the wind? No, of course not. Equity market valuation is still at extreme levels and there’s no doubt that segments of the financial markets have gone full-on-irrationally-exuberant-ludicrous-bubble-mode (a very technical term).

Then, does that mean it’s time to move to cash? Again, no, the problem is markets can stay irrational for longer than most can stay patient and sane. Sitting in cash while “watching your neighbors get rich” (h/t Jeremy Grantham) often ends in the same way as trying to time the market’s tops and bottoms; both lead to doing the wrong things at the wrong times.

The market is not some kind of show with episodes and intermissions when we can conveniently start or stop, neatly enter or exit. The market has no beginning or end, it is a show that is always on and never pauses.

At BCM, our job is not to predict what happens next but to watch carefully, wait patiently, and respond to whatever comes. At present economic and market conditions are supportive of risk assets, as such our models remain fully invested relative to their strategic targets.

There are obvious risks, conditions will change, and we will respond accordingly when they do. Meanwhile, the show must go on.

—

Victor K. Lai, CFA

You must be logged in to post a comment.