NOTE ON UPDATES

Starting with Q1 2021, BCM is consolidating its various update notes into a single “Quarter Update,” labelled as “Quarter Update” under Categories. This reduces redundancy and makes updates easier to follow.

QUARTER REVIEW

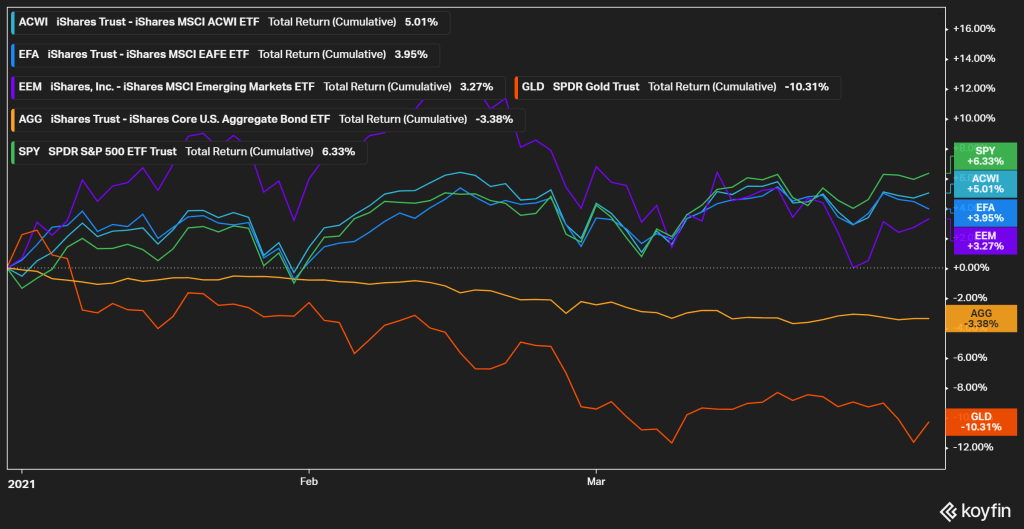

Q1 started with a rally in risk assets, but equity markets are still off their all-time-highs notched in February. Overall, markets retain a risk-on tilt with the ACWI +5% YTD while safe havens like bonds and gold are down for the quarter.

Figure 1 Global Markets

MACRO CONDITIONS

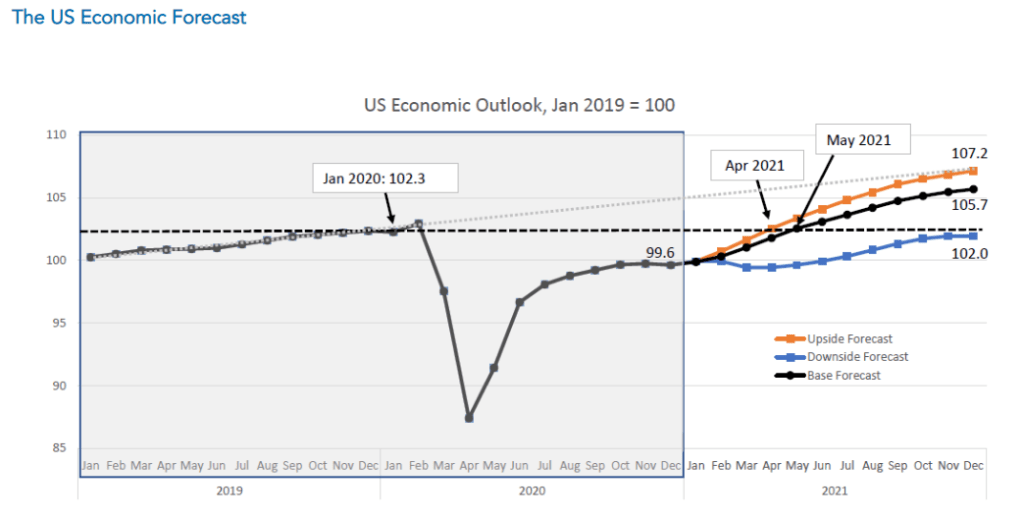

Economic conditions so far this year have mostly unfolded as we expected. Despite incessant back and forth over the pandemic, vaccines are disseminating, stimuli are distributing, and people are re-emerging from self-imposed hibernation.

Looking ahead, our baseline expectation is for continued expansion of the global business cycle. That expansion could accelerate even more than expected due to the greasing (i.e. fiscal stimulus) of already bulging pent-up demand. Year-ahead economic forecasts are shown for the US and the world in Figures 2 & 3 below.

Figure 2 The Conference Board US Growth Forecast

Figure 3 IMF Global Growth Forecasts

Meanwhile, market conditions reiterate the same narrative. For example, the outperformance of value over growth stocks has widened to a notable spread since we initially pointed out the potential reversal this past November.

Figure 4 Value vs Growth (IWD vs IWF)

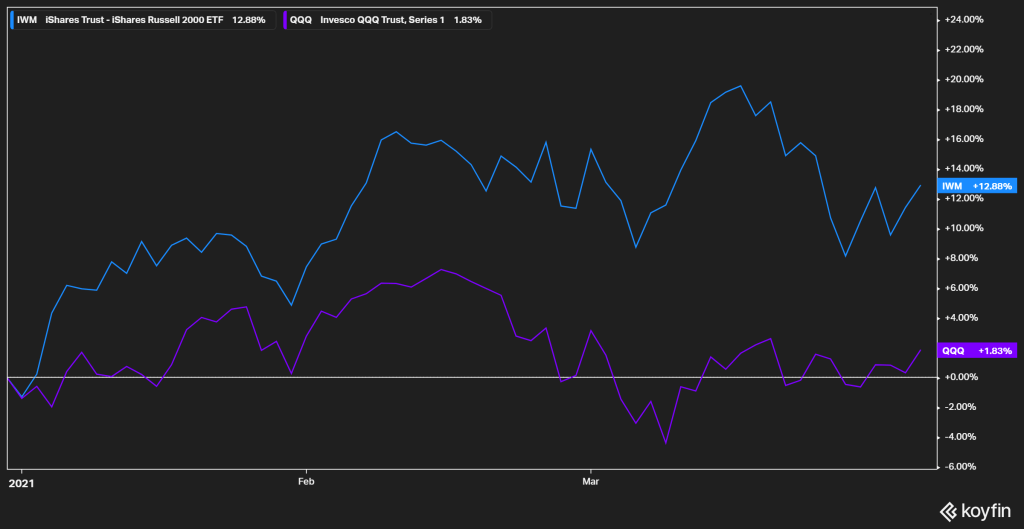

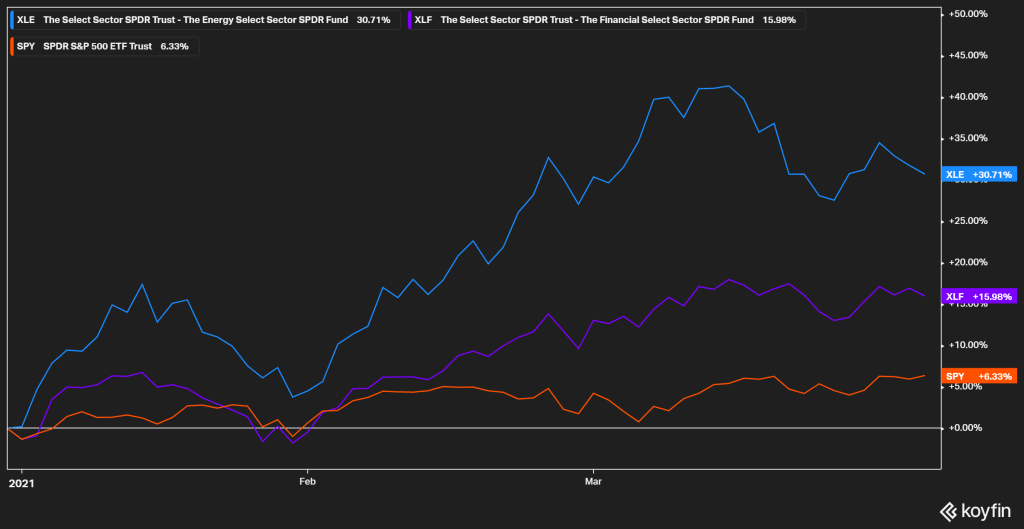

In addition, small caps continue to outperform large-cap tech, while cyclical sectors like energy and financials have taken off versus the broader market.

Figure 5 Small Caps vs Large Tech (IWM vs QQQ)

Figure 6 Energy and Financials vs S&P 500 (XLE, XLF vs SPY)

These conditions reflect broadening market strength as investors rotate out of a small number of large tech names and into a wider range of cyclical stocks that benefit from an acceleration of the business cycle.

INVESTING OUTLOOK

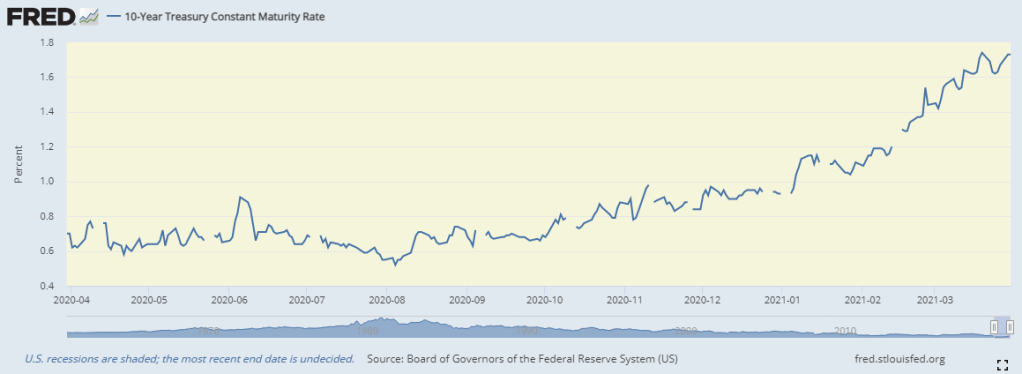

Ironically, just as a positive outlook becomes front and center consensus, a contrarian surprise may be emerging around the edges. As usual, hints first surface in the fixed income markets. Long-term interest rates surged in Q1 as the 10-Year Treasury yield shot up from 0.90% to over 1.70% – an over 80% jump!

Figure 5 10 Year Treasury Yield

Like with equity market action, the rise in yields correspond with expectations for accelerating economic growth. However, the yields also point to caution. I’ve written numerous times about how historically low interest rates have supported high valuations. The reverse logic holds that rising rates could pull the rug out from under elevated prices.

For example, the recent correction in the tech-heavy NASDAQ can at least partially be attributed to rising rates as tech-stocks are typically “long-duration” and sensitive to interest rates. If rates continue to climb, they will drag on all stocks and weigh on the broader market.

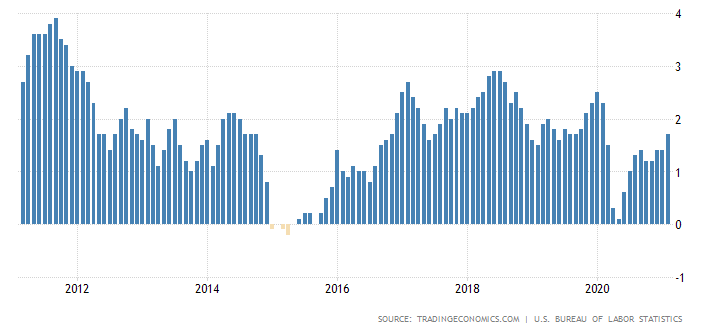

This is a development worth watching closely. The most likely path towards a continued surge in rates is if inflation comes in hotter than expected. In that case, the Fed could be forced to hike rates and inadvertently deflate the stock market.

Figure 6 US Inflation Rate

To be fair, even though inflation and rates have moved up over the past year, they are still relatively low and have been so for a decade. The 10 year yield was actually higher pre-pandemic than where it is now. Meanwhile, based on the US Federal Reserve’s commentary, economic factors like slack in the labor market are likely to keep inflation tame in the near term and the Fed does not expect to raise rates until 2023.

Still, negative surprise are unexpected by definition. So, this is something worth watching and we will be doing that carefully with great interest.

STRATEGY UPDATE

In Q1, BCM model portfolios moved to a modest overweight in risk assets. We worked towards the position during the market corrections in February and March led by tech stocks in the US and emerging markets abroad. While the timing of the selloffs rekindled flashbacks of the Q1-2020 crash, a repeat seemed unlikely based on the positive economic momentum we observed and the lack of a compelling downside catalyst.

In our view the corrections provided needed relief from overbought pressures building across global equity markets. In all likelihood they were temporary pullbacks within the normal ebbs and flows of a longer-term upward trajectory, and as such were opportunities to add to risk exposure.

Within equities we continue to favor cyclical sectors like energy, which still has favorable relative valuation versus the broader market, albeit less so than last year. We also believe small cap and value stocks in general will continue to outpace their large cap growth counterparts.

That being said we remain cautious and tempered. By no means are we overextending on risk or reaching for returns. Valuations remain elevated and markets have already priced in improving expectations, so despite a positive macro outlook we refrain from moving to a maximum overweight risk position.

In other words, the market wagon continues to grind forward and we continue along for the ride. However, we also keep our eyes peeled to the wheels, ready to abort when we see them begin to fall off (i.e., economic and market conditions deteriorate).

Of course, we don’t know when conditions will change, we simply know they will. As always, our job is to watch carefully, wait patiently, and respond accordingly when they do.

—

Victor K. Lai, CFA

You must be logged in to post a comment.