MACRO VALUE IS NOW MACRO ALLOCATION

A quick update, moving forward our “Macro Value” strategy is being renamed to “Macro Allocation.” This name change reflects adjustments we made to the strategy over the past year. The core principles are still the same, a macro approach with an emphasis on value.

However, as I have been writing over the past two years, compelling market values have become increasingly hard to find. For MV it created the rising risk of being underinvested due to a lack of attractive traditional value opportunities in a decidedly risk-on environment where valuations increasingly did not seem to matter.

I started addressing the issue in 2019 by incorporating a “target risk allocation” (TRA) into the MV framework, adopted from our aptly named Tactical Allocation strategy. I elaborated on the changes earlier this year.

In short, TRA helps the portfolio stay within minimum and maximum levels of risk exposure regardless of how valuations look. Think of TRA like guard rails that help prevent the strategy from getting too over or underexposed in the wrong market environments.

After the TRA is established, the strategy will still look to fill the allocation with undervalued market opportunities first. However, if there is a dearth of value in a risk-on environment, then we will fill the TRA gap with broad global equity market exposure via the ACWI.

The rationale for that is in a risk-on-environment, broad equity market exposure is the next best thing absent other compelling, value opportunities. The reverse is true in a risk-off environment, we’d reduce risk exposure by trimming allocations in ACWI and value positions as appropriate.

2020 showed just how important the TRA adjustments were as global markets made extreme swings both ways with little to no regard for valuations. As a result, the TRA decisions had a significantly larger impact on the strategy’s results than the value positions did. That won’t always be the case, but the point is TRA is here to stay and will likely have a meaningful impact on results moving forward. Hence, the name changed to Macro Allocation.

MACRO OVERVIEW

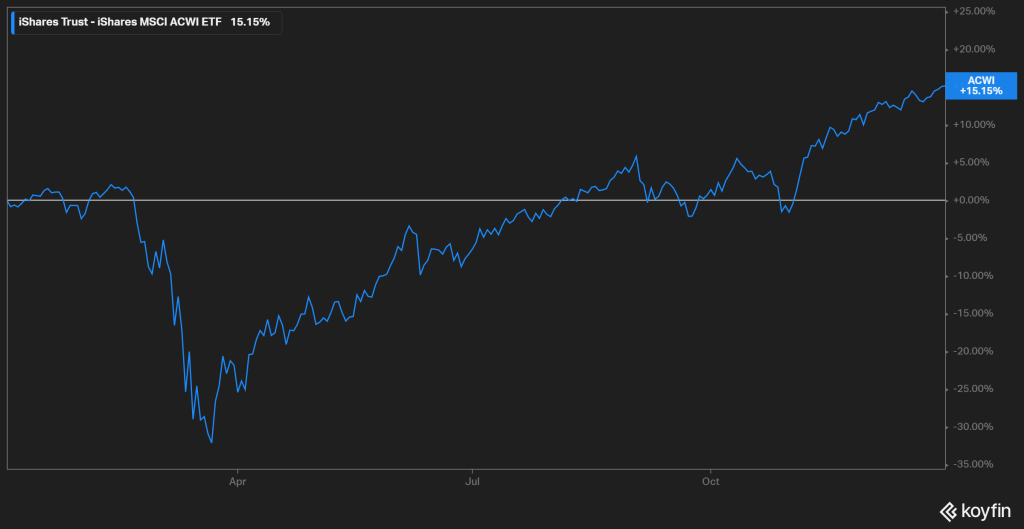

2020 was truly a breathtaking year in more ways than one. Financial markets exhaled a long sigh of relief after March’s unprecedented pandemic plunge. In the end, the global equity market managed a gain of +15.15% for the year (as measured by the ACWI). That was after clawing back a -34% drop from Q1 for a massive rally of +50% in just 9 months! Suffice to say that does not happen often.

Figure 1: Global Equity Market

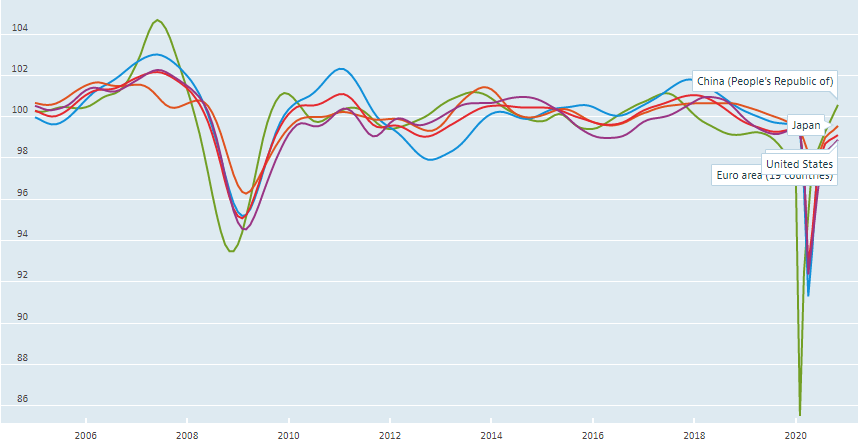

As I’ve written several times even small marginal improvements in economic data (seen as better rather than worse) can be enough to push financial markets higher. It’s clear that much happened in 2020 judging by leading economic indicators.

Figure 2: OECD Composite Leading Indicators

That doesn’t mean markets must continue to rally from here. To be fair, markets have already priced in positive expectations while improvements in economic conditions have moderated. What happens next will most likely be influenced by the relative changes in economic and market conditions moving forward.

Figure 3: TCB Leading Economic Indicators

MACRO ALLOCATION

In Q4, Tactical Value (MA) maintained a neutral Target Risk Allocation (TRA) of approximately 60%. In hindsight, moving to 100% risk allocation (or even more with leverage) would have been the most profitable move. But at the same time we avoided the equally extreme move of sitting in cash and watching from the sidelines (in horror and disbelief) as equity markets notched one record high after another.

We reached our moderate position by understanding that marginal economic improvements (better than worse) could increase risk appetite while simultaneously recognizing that a number of unresolved issues could upend the burgeoning recovery at any moment.

At this point, it appears a number of those issues have been or will be resolved. At year-end 2020, COVID vaccines are already being administered, the second round of stimulus is inked, and the POTUS election confirmations are around the corner. Barring another blind-siding shock, and all else equal, this provides a favorable backdrop for risk assets heading into 2021. From that perspective, TV maintains its neutral TRA.

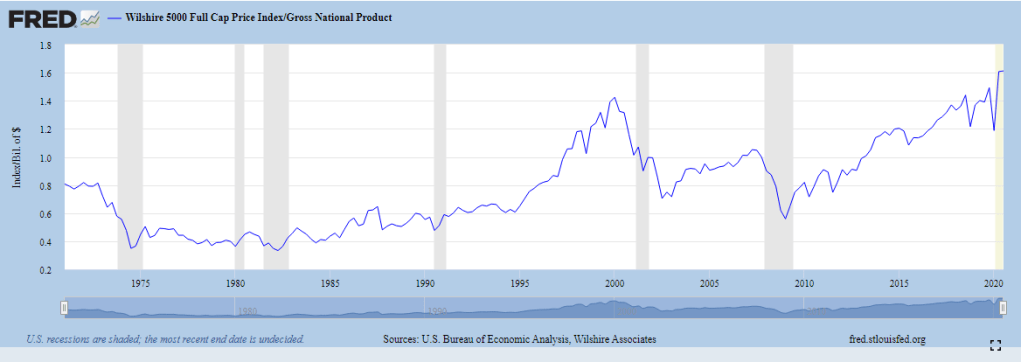

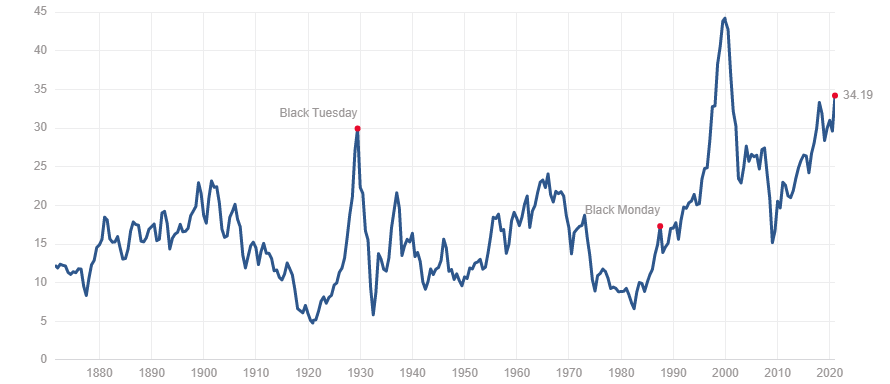

One lingering issue that remains unresolved and prevents MA from going overweight is valuation. Ultimately, value is still a key consideration for MA and at present equity market valuations are just high. Two of the most reliable equity market valuation measures, market cap to GDP and CAPE, are at their highest and second-highest levels in history (respectively).

Figure 4: Market Cap to GDP

Figure 5: Shiller CAPE

I wrote in Q3 that the high prices may be less extreme than they appear due to abnormally low-interest rates. That’s still true and reinforces the argument that high prices alone are not a sufficient reason to sit on the sidelines and avoid the market (i.e. high prices could always go even higher).

At the same time, thinking that overvalued assets can become even more overvalued is a poor argument for increasing exposure. Our neutral TRA position reflects our respect for both sides of the argument.

Within the risk allocation, MA has positions in cyclical markets and sectors such as foreign small-cap and US energy stocks. Not only are these areas have relatively attractive valuations versus the broader market, but they should also benefit from continued global economic expansion, which is our base case assumption.

“Relatively attractive valuation” is worth repeating because absolute, compelling market values are still elusive. As a result, the largest position within the TRA at present is ACWI. This is our temporary remedy to “fill the gap” as explained above.

THE BOTTOM LINE

2020 was truly a historic year that will likely change the world, how people behave, and how business is done forever. It certainly affected how Macro Value, now Macro Allocation, works. However, some things never really change. Although MA has added an emphasis on tactical risk allocation, that does not mean valuation no longer matters.

To be clear, in the short-run value can matter less and may even seem irrelevant during temporary bouts of speculation and investing fads. But in the long-run valuation still does matter. Value is, always has been, and always will be the foundation of rational, intelligent, long-term investing.

To that end, valuation will continue to play a key role in the MA strategy, just to differing degrees depending on changes in the market environment. I can’t predict when those changes will happen, but I can assure you that we will watch closely, wait patiently, and respond accordingly when they occur.

—

Victor K. Lai, CFA

You must be logged in to post a comment.