QUARTER REVIEW

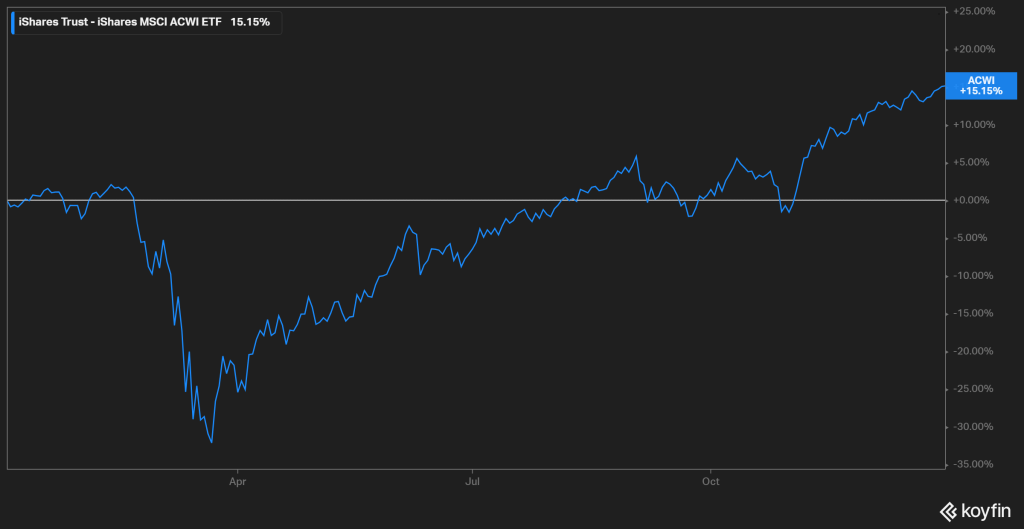

The fourth quarter capped what can only be described as a breath-taking year for the markets (and the world). The global equity market rose +15.15% in 2020, as measured by the MSCI ACWI. While that doesn’t look outstanding by itself, keep it mind that was after clawing back a -34% decline from Q1 for a massive global rally of +50% in 9 months! Let’s just say we don’t see that kind of price action every year.

Figure 1 Global Equity Market

ECONOMIC AND MARKET CONDITIONS

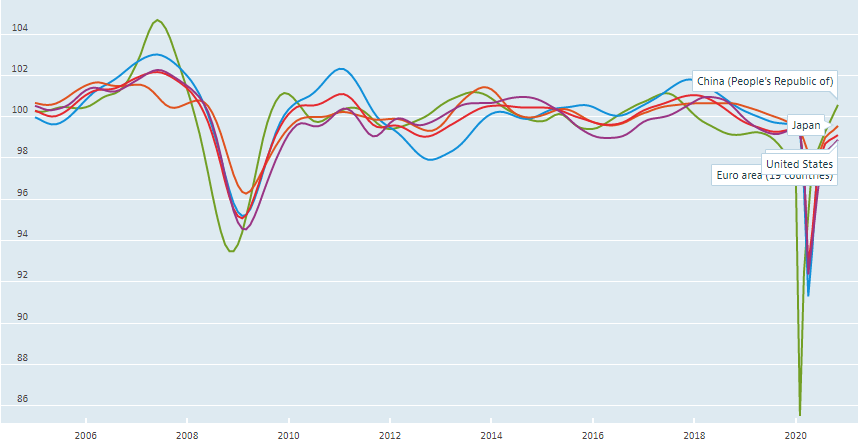

Although many would say economic conditions are not yet in the clear, they have clearly climbed out of a hole since Q1. And while the Q2 surge could be somewhat discredited as a hard bounce off a bottom, conditions continue to improve on the margin. I’ve noted before even small marginal improvements in economic data (seen as better rather than worse) can be enough to push financial markets higher. Judging by leading economic indicators, it appears that’s what happened.

Figure 2 OECD Composite Leading Indicators

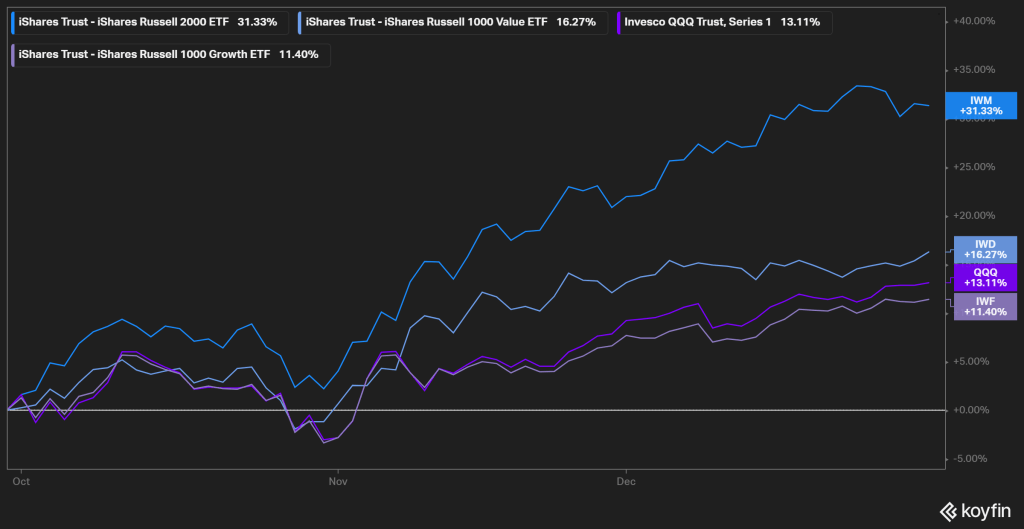

Another development that supports the positive trend is the recent rotation in market performance. We’ve seen a pronounced shift in US equity market returns during Q4 favoring small cap and value stocks over large cap growth stocks. This is shown in the chart below as the R2000 and R1000V (IWM and IWD in blues) versus the NASDAQ100 and R1000G (QQQ and IWF in purples).

Figure 3 Equity Market Rotation

This is noteworthy because large cap growth stocks, like the infamous “FANGMAT” gang, have dominated in terms of performance and attention for the past decade. So much that a small handful of tech bellwethers now account for close to 20% of all US equity market cap. That’s the highest level in the past two decades (albeit not the highest ever).

That concentration can be indicative of economic weakness and market fragility. Weakness because crowding into a small handful of stocks implies investors are doubtful of widespread economic strength that supports broad market advances. And fragility because so much market cap and return concentrated into so few stocks leaves the market more vulnerable to large drawdowns.

On the other hand, outperformance of small cap and value stocks tends to occur during periods of broadening (not narrowing) economic and market strength. So, this is an encouraging development. Additional encouragement exists in the end of a polarizing POTUS election, highly anticipated federal stimulus, and of course long awaited vaccinations.

Does that mean markets continue to rally from here? I don’t know. To be fair, improvements in economic conditions have moderated and markets have already priced in positive expectations. Moving forward, it will be the relative changes in economic and market conditions (for better or worse) that determine where we head next.

Figure 4

TACTICAL ALLOCATION

In Q4, TA model portfolios maintained neutral risk weights in line with their strategic targets. This is a continuation of the changes we made in Q3. We refrained from moving to overweight risk exposure during the year which, in hindsight, worked against us.

However, there was and still is a substantial amount of lingering uncertainty. COVID19 continues to hold the world hostage with threats of shutdowns. In the US, the full economic impact of the pandemic is still unclear as government assistance withers for millions of individuals and businesses. All this at a time when both equity and fixed income markets are priced at all-time-highs.

Indeed, uncertainties abound. In times like these, like 2020, when anything could happen, it makes sense to maintain balance and to avoid sudden or extreme movements. We don’t know when conditions will change, but we recognize they will. As always, we will be watching closely, waiting patiently, and responding accordingly to the changes when they occur.

—

Victor K. Lai, CFA

You must be logged in to post a comment.