QUARTER IN REVIEW

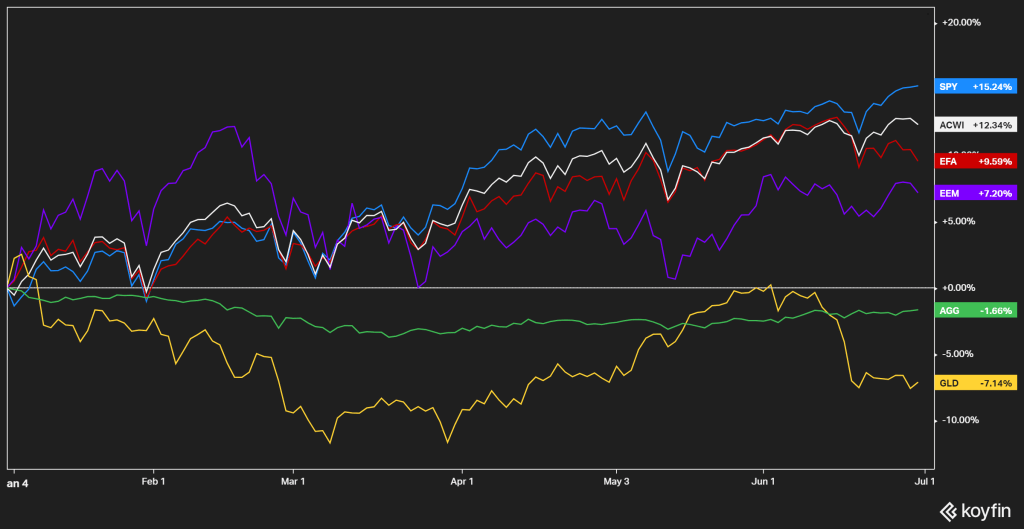

In the second quarter risk appetite remained voracious among investors. Global equities reclaimed and surpassed highs reached in Q1 and the MSCI ACWI was up +12% year to date. Meanwhile, traditional safe havens remained under pressure. Gold was off nearly -12% at one point but clawed back some of that by quarter end.

Figure 1 Global Markets

MACRO PERSPECTIVE

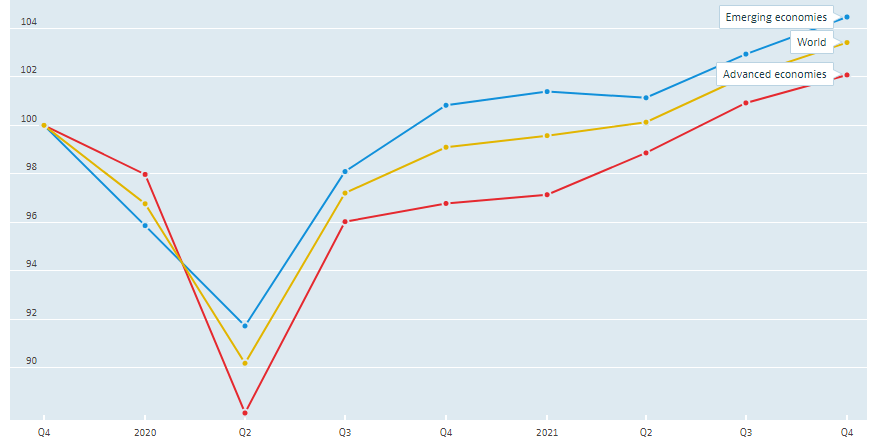

The global economy expanded further in Q2 as we expected given the trifecta of vaccinations, stimuli, and the great reopening. Nobody knows how long this expansion will last, but typically expansions run for years at a time.

Of course, nothing has been “typical” about the past year and it’s possible the fastest recession in history begets the shortest expansion ever. Regardless, it’s fair to assume the breakneck pace of recovery is behind us.

Figure 2: GDP Forecast

Source: OECD Economic Outlook, Base Quarter 100 = Q4 2019

We’re back to climbing the never-ending wall of worry and inflation is the slippery obstacle of the moment. In January 2020’s annual letter I wrote inflation was not just on the rise, but the rate of change was alarming. The pandemic interrupted the trend but it appears to be back in force.

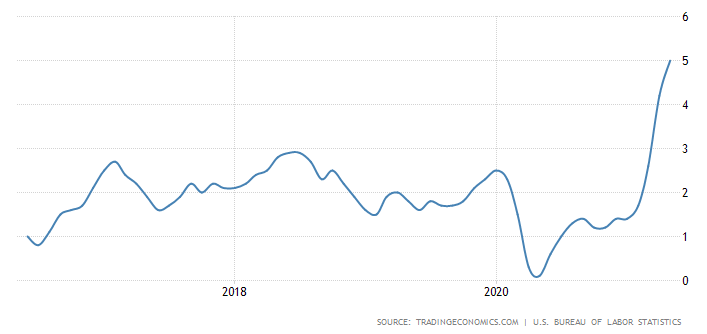

The most recent CPI numbers (5% annualized as of May) were not only higher than expected, but also some of the highest we’ve seen in decades. I wrote in March hotter than expected inflation could force the Fed’s hand to tighten monetary policy sooner than anticipated. The Fed’s June FOMC statement and commentary since reflected just that, signaling rate hikes and tapering may begin sooner than previously expected.

Figure 3: US CPI Annualized Inflation Rate

Markets and sentiment slipped following the Fed’s pivot, but was any of the news really surprising? US money supply growth has long been inflating and reached outrageous levels during the pandemic. Was it reasonable to believe that much money supply would not be inflationary?

Figure 4: US M2 Money Supply

Semantics and technicalities can be debated – components of M2, credit creation, velocity of money, etc. But in the end inflation is simply the monetary phenomenon that is too much money chasing too few goods, and obviously the money is there.

As for goods, we have the peculiar affects of the pandemic to thank. The economy cannot be just turned on and off like a light switch, not without consequences anyway. The abrupt lockdowns of the past year caused major disruptions to global supply chains. The sudden recovery made matters worse as suppliers struggled to keep up with the rebound in demand. The consequence was price hikes for everything from lumber to food.

However, prices may have peaked in Q2 and, as with life, may be heading back to normal. That’s why the Federal Reserve insists recent inflation is “transitory” and that it too shall pass. The Fed looks right based on the recent pullback in commodity prices.

Figure 4: Commodities Prices

Then again, the parabolic moves in commodities were never sustainable and a reversal was always logical. The question is where do prices settle after the transitory spike? My guess is somewhere higher than before. My guess is the past decade of below average inflation will be followed by a period of above average inflation.

In fact, Chairman Powell stated multiple times that the Fed will allow inflation to run above its long-term target. The Fed is telling us what to expect, higher inflation. This could have substantial affects on financial markets, yet they remain relatively calm.

INVESTING COMMENTARY

Markets seem complacent and myopically focused on the Fed’s transitory narrative. For example, the 10 Year Treasury yield has bounced off all time lows but remains subdued below its pre-pandemic range and long-term average.

Figure 5: 10 Year Treasury Yield

Remember, yields reached double digits during the 70’s and 80s. That’s not saying we’re headed for double digit inflation, but it does mean bond yields have some catch up to do if inflation continues to come in higher than expected.

At BCM we’ve been reducing our bond exposure and the duration of our bond allocation since last year. Within fixed income we’ve favored short-term Treasuries and investment-grade corporates. This positioning provides a dual purpose of defending against inflation and potential equity market drawdowns.

Meanwhile, we marginally increased our allocation to risk assets. At present, we continue to hold a modest overweight risk allocation relative to strategic targets. Most of that is through global equity market exposure.

I’ve written several times about elevated stock market valuation, but I’ve also pointed out valuation can take a back seat to economic and market conditions in the short run. Conditions have been such that the stock market became a runaway train and the opportunity cost of waiting at the valuation station was just too high.

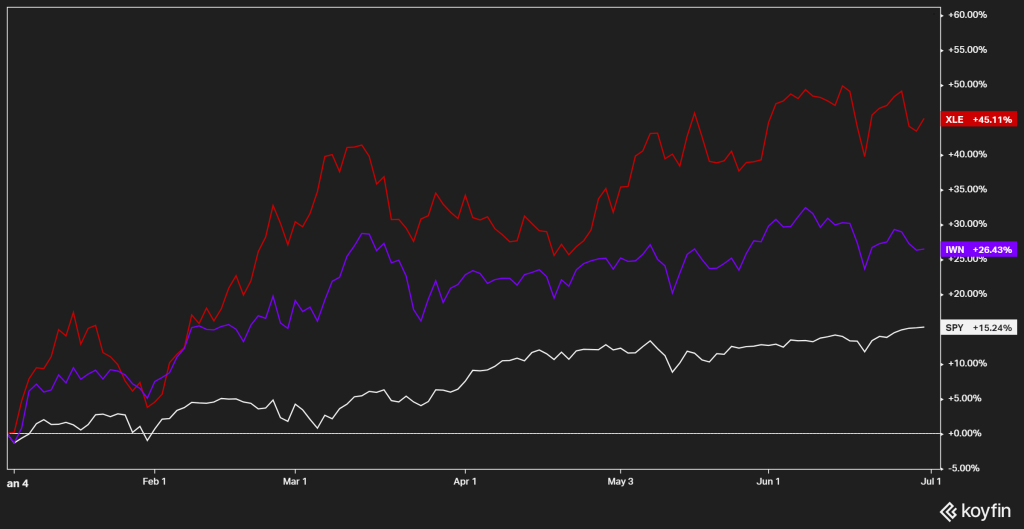

Within US equities we still favor energy and value. We believe these market segments will continue to benefit from an ongoing expansion of the business cycle. We also still see traces of favorable relative valuation in the segments versus the broader market. Both energy and value have outpaced the S&P 500 year to date.

Figure 6: Energy, Value, and S&P 500

Globally, we prefer foreign equity markets versus the US for contrarian reasons. The US has emerged as a clear leader both in terms of vaccination and reopening. For example, as recently as May India was still struggling with outbreak and Germany was still in lockdown.

As a consequence, both foreign economic conditions and equity markets have trailed those of the US. However, as Chairman Powell would say, those conditions are “transitory.” The effects of COVID19 will pass and the rest of world will catch up. In other words, foreign markets are next in line to ride the rolling wave of global recovery and expansion.

Figure 8: US vs Foreign Equity Markets

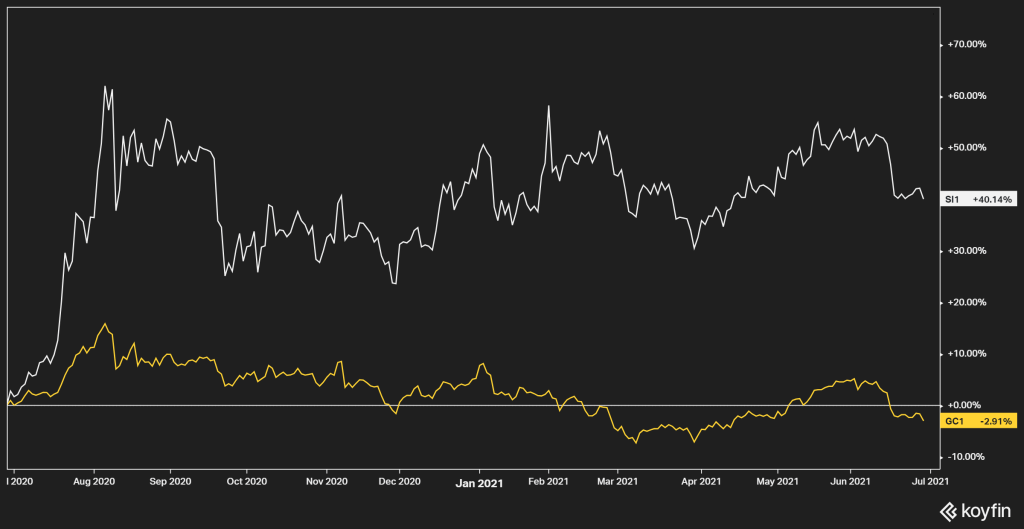

Lastly, we’re still holding precious metals. We sold off our gold position after a strong 2020, but held on to silver and even added to it during the sell off in March and April. We preferred silver due to it’s relative valuation versus gold and also due to it’s sensitivity to inflation, something I’ve written about previously. Silver prices are up over +40% in the past year while gold is negative.

Figure 9: Silver vs Gold

THE BOTTOM LINE

Heading into the third quarter life in the US is getting back to normal. The traffic is back on the streets and the kids are back in school. It’s all familiar but also somewhat strange following a year of abnormality. Likewise, the economy and the markets are still adjusting and trying to get back on track.

For now the macro trajectory and momentum are positive. So long as the global expansion rolls on markets should continue their risk-on trend. It will take a substantial shock to throw conditions off course. However, shocks are also surprises that most people don’t see coming.

Higher than expected inflation could be such a shock. If inflation rages out of control financial markets across the board from stocks to bonds would suffer steep drawdowns given historically high equity valuations and historically low bond yields.

However, that extreme scenario is also not our baseline expectation. Rather, we think inflation could be both higher than expected but also not catastrophically high. That scenario favors equity over fixed income. As such we are currently positioned for both continued expansion and higher than expected inflation. But, as always, we will actively adjust our positions as economic and market conditions change.

—

Victor K. Lai, CFA

You must be logged in to post a comment.