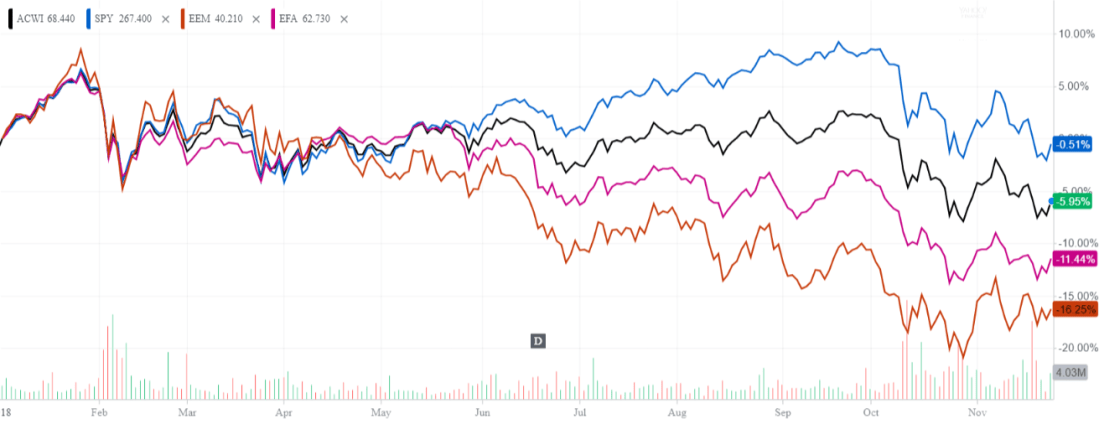

The last two months have been choppy for stocks. The S&P 500 is down about 8% and has given up its gain for the year. Emerging markets have outperformed since October, relatively speaking, but remain the biggest loser YTD, down about 16%.

As usual, the financial media is searching, desperately, for something to fear. Does the decline in emerging market stocks reflect deteriorating economic conditions, does the unwind of FAANG momentum signal slowing growth, and does the fall in oil prices mean weakening demand?

Of course, they could, but they could not just as well. Despite being down 16% this year, emerging market stocks are still up more than 12% since 2017. Tech bellwether FB was up over 500% before falling 25%. And oil demand has actually increased, not decreased, so over supply is likely the issue. The headlines will always find the next thing to fear but more often than not there’s more sensation than substance.

A good recent example of this is rising interest rates. Rates in the US have been rising for 3 years and over the past 12 months there has been increasing rhetoric of the impending doom and gloom it will bring. Sure, high-interest rates can become a headwind for economic growth, corporate earnings, and the stock market.

Yes, rates have risen, but they are still well below long-term average levels and still quite low relatively speaking. If history is any guide, rates start to become a drag on the stock market when the 10 Year Treasury yield is at around 5%. The chart below shows the 10 year Treasury yield since 1962.

Of course, that doesn’t mean there are no risks. Both economic and earnings growth do look to be moderating and that brings us closer to the next recession. But even slowing growth is still moving in the right direction and is not the same thing as a contraction.

Most leading economic indicators don’t signal an imminent recession. That could certainly change in 2019, but for now, you can tell the fear-mongers in the back seat we aren’t there yet. There will be plenty of headlines to worry about along the way. It’s always something, but more likely than not, it ends up being much ado about nothing.

Victor K. Lai, CFA

You must be logged in to post a comment.