Time for Turkey?

The Holidays are almost here, but no, I’m not writing about your upcoming Thanksgiving dinner. I’m writing about a Turkey with Lira that’s down 90% against USD and an equity market that’s down 70% from its highs.

TUR data by YCharts

TUR data by YChartsWhen others are fearful

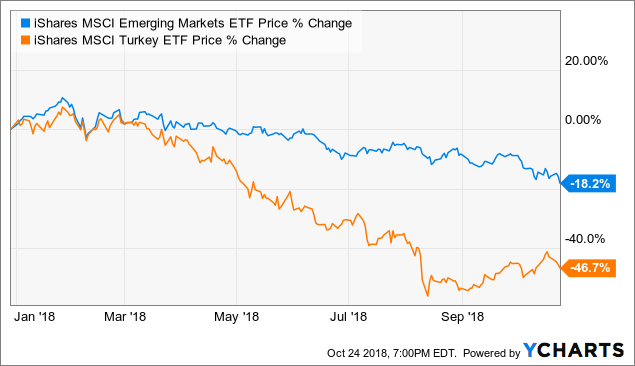

Emerging market equities have sold off broadly year-to-date. The markets seem especially scared of Turkey, but what’s there to be afraid of?

EEM data by YCharts

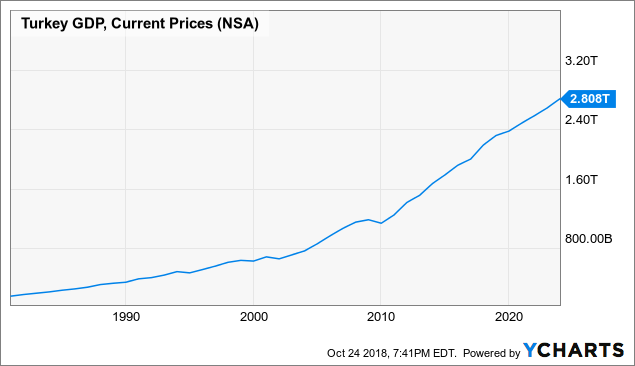

EEM data by YChartsTo start, let’s look at how we got here. Turkey’s long-time leader Recep Tayyip Erdogan is a stimulative bull. He likes borrowing, spending, and keeping rates low. He’s gone as far as claiming that high-interest rates are the “mother and father of all evil.” His approach may be eccentric, but Erdogan successfully grew Turkey’s economy based on GDP.

Turkey GDP, Current Prices data by YCharts

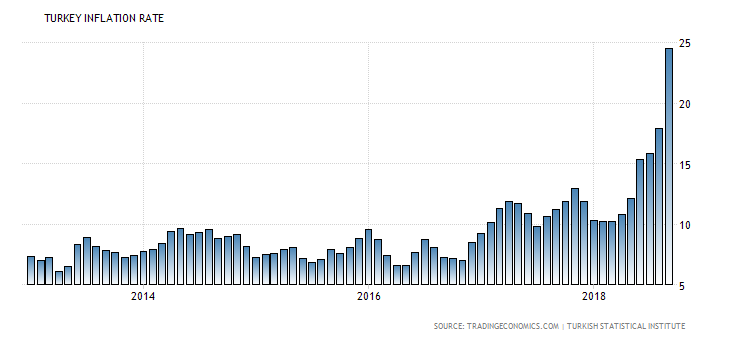

Turkey GDP, Current Prices data by YChartsBut such policies come at a cost. For example, after a long quell, inflation crept up to almost 25% and some fear inflation could return to the runaway levels of the 1990s. At the same time, Erdogan’s reluctance to raise rates, increasingly authoritarian tendencies (he recently consolidated power over the central bank), and a litany of bizarre statements about monetary policy (“higher rates lead to higher inflation”) has markets questioning if Erdogan will fail to keep inflation in check.

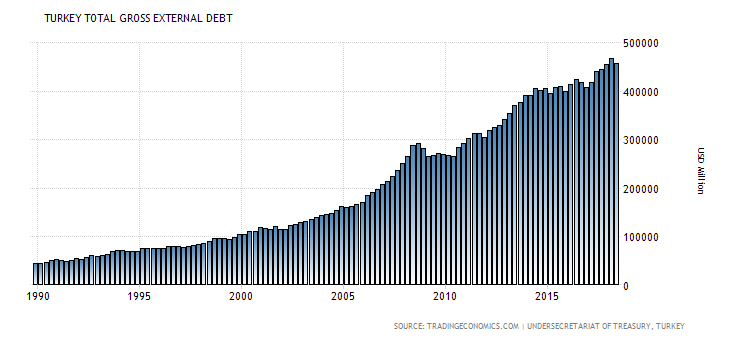

Maybe a bigger fear stems from outside Turkey. During its growth binge, Turkey attracted ever-increasing amounts of foreign investment, and in the process also accumulated large amounts of external debt (or debt denominated in foreign currencies). As of July 2018, Turkey’s external debt to GDP was over 54% based on data from the World Bank.

The toxic mix of inflation, rising debt, and falling Lira spread fear that Turkey wouldn’t make good on its debts. This caused an outflow of foreign capital, which made things even worse. Adding insult to injury, a spat with the United States over a detained US pastor led the Trump administration to announce tariffs and sanctions on Turkey. This was all enough to send investors fleeing for their livelihoods.

A good look

There’s a lot of scary things in Turkey, yes. However, in times like these, it can pay to take a step back and take a good look at the bigger picture.

This isn’t Turkey’s first financial crisis rodeo. In fact, it’s had one every decade over the past thirty years. Like most crises,’ they follow a similar routine. Step 1, inflation rises and currency falls. Step 2, everyone freaks out about financial meltdown and recession. Step 3, markets get oversold and things aren’t as bad as expected. Step 4, there’s a V-shaped recovery and markets rally. “This time” is rarely any different.

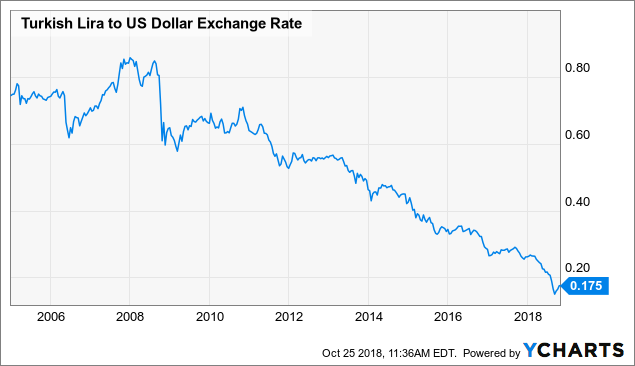

But there are some things that make the current situation less scary. First, the Lira has fallen for the past decade and already looked relatively cheap prior to the accelerated sell-off. In contrast, the Lira looked relatively expensive heading into the previous crisis in 2008.

Turkish Lira to US Dollar Exchange Rate data by YCharts

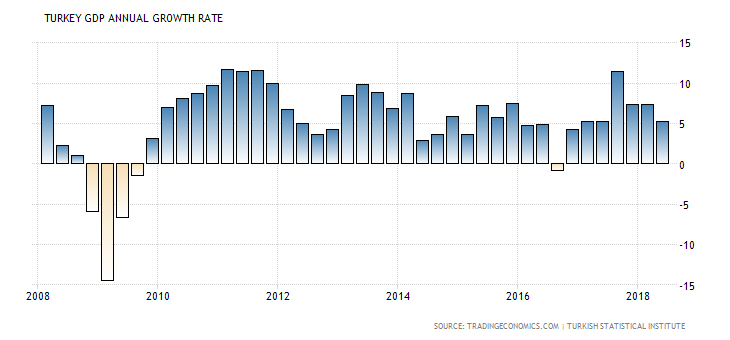

Turkish Lira to US Dollar Exchange Rate data by YChartsSecond, Turkey was previously one of the fastest growing emerging markets, clocking an average GDP growth rate of 7% per year. It’s most recent read was a “weak” 5.5%, which relatively speaking doesn’t look that bad compared to developed economies clawing to stay above 3%. Despite the short-term turmoil, Turkey’s long-term trajectory remains intact. Goldman Sachs includes Turkey in its “N11” or list of next eleven countries poised to drive global economic growth, much like the “BRIC” countries did in recent decades. Likewise, Fidelity names Turkey in its list of four “MINT” countries.

Third, despite Erdogan’s stubborn persona, he may be more flexible than he appears. In September, Turkey’s central bank hiked short-term rates to 24% which was not only contrary to Erdogan’s public position but also significantly above expectations. Then in October, after refusing to release a detained US pastor, Erdogan unexpectedly did just that, improving US relations in the process. The point is Erdogan may be more rational than he’s given credit for, and conditions are already turning out better than expected.

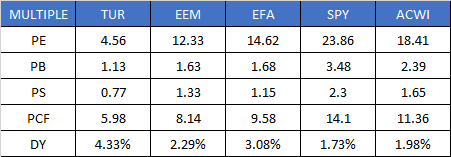

Fourth, in a world of ever-increasing valuations, Turkey’s equity market is a rare find. The table below shows a comparison of price multiples and dividend yields for the iShares MSCI Turkey ETF (TUR) versus other market-ETFs. Its hard to argue Turkey doesn’t look cheap on a relative basis, and hard to imagine one of the “N11/MINT” markets will trade under 5x earnings and 0.77x sales for good.

Valuations

Source: ETF.com, Thomson Reuters, BCM

I know, I can hear it now, “but Turkey has all kinds of problems and no upside catalyst which justifies lower multiples.” The argument makes sense, but I think it misses the point. Turkey doesn’t need a complete turnaround or standing ovation, it just needs to do less badly than expected. Right now, the hurdle is low.

For the record, I heard similar arguments against my call long call for Russia in September 2015 (+58% in 2016), my long call for Greece in October 2016(+35% in 2017), and my long call for Nigeria in April 2017 (+34% in 2017).

No pain no gain

There are risks, as always, and Turkey certainly has its share. Emerging markets are obviously selling off and Turkey will likely follow the tide, up and down.

Should the market continue to lose confidence in Erdogan’s ability to fend off inflation things will get worse before better for both the Lira and Turkish stocks.

Also, if capital outflows accelerate, Turkey may seriously have trouble defending its currency and servicing its foreign debt due to its limited foreign currency reserves.

If the situation gets bad enough, Turkey would likely need to fall back on the lender of last resort, the IMF, for bailout loans as they have in the past.

One last concern, Turkey’s prior crises corresponded with recessions. This time around, that hasn’t happened, but we’re not in the clear yet. It’s still early and we don’t fully know what the impact will be on Turkey’s business cycle.

All of these issues are uncertain, and none of them are market-friendly, to say the least.

The bottom line

In the near-term, there are plenty of uncertainties surrounding Turkey. And those who cannot look beyond the rampant short-term volatility in Turkish markets should probably just look away.

I don’t know if the Turkish stock market has found a bottom, and there could certainly be more downside from here. But pessimism is pervasive, expectations are in the gutter, and prices look low enough to warrant some serious consideration.

Unless Turkey implodes, it gets past the current crisis and resumes on its positive long-term trajectory. I think a patient position in TUR at current prices or better will prove to be an excellent value.

If you take a position, do your homework, build it on price weakness over time, and don’t bite off more than you can stomach.

Victor K. Lai, CFA

Disclosure: Victor Lai is long TUR