Most people probably think of Hewlett-Packard when they hear “HP.” This is almost certainly the case for investors who have followed Hewlett-Packard’s struggles. However, I’m not writing about that HP, I’m writing about another HP that many people have never heard of. Helmerich & Payne (HP) is a $4.9 billion oil and gas company based in the US. It provides contract drilling services for oil and gas wells worldwide. As of September 26th, HP is trading around $46 a share. At this price, I think HP looks attractive, here’s why.

Industry Outlook

My outlook for the oil and gas drilling industry is generally positive. Even in the face of sluggish economic growth, drilling activity remains robust due to persistently rising oil prices, increased focus on domestic energy security, and the growing need for unconventional extraction techniques.

Company Overview

A long history of investing in R&D has positioned HP as an industry leader. Its proprietary “FlexRigs” are more advanced and flexible than conventional rigs. They can drill where others cannot. Even at a higher price point, FlexRigs can lower total operating costs due to increased efficiency. Increasing demand from operators has resulted in a shortage of high-end rigs, and has allowed HP to charge a premium with contracts that are longer than average.

Financial Condition

HP’s balance sheet looks rock solid. It has little debt and ample cash. Compared to industry averages, HP has superior levels of liquidity, solvency, and financial strength. Figure 1 shows a quick comparison of some key financial condition measures.

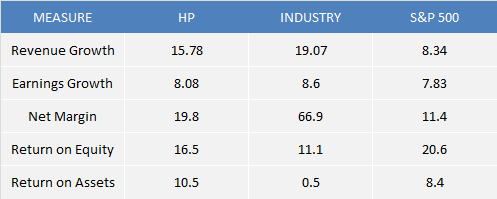

Growth & Profitability

For the past decade, HP has steadily grown sales, earnings, and cash flow without a hitch. Though HP’s revenue growth lags its peers, it still outpaces the broad market thanks to robust industry conditions. In addition, HP outperforms its peers in terms of both RoE and RoA. Figure 2 shows a quick comparison of some key growth and profitability measures.

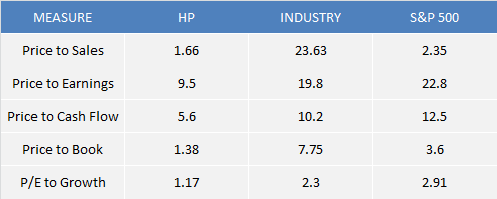

Valuation

HP looks undervalued relative to both industry peers and the broad market. At 9.5x, HP’s current PE multiple is less than half of its long-term average of 20.3x. The industry average is currently at 19.8x. HP’s PEG ratio is also about half of the industry average. This suggests that HP is still attractively priced relative to peers, despite its lower earnings growth.

Target Price

Using a blend of relative valuation and discounted cash flow analysis, I arrive at a 12-month price target of $59. This target is based on multiples of 15x earnings, 10x cash flow, 1.5x book value (all five-year average values), and an 11% discount rate against average analyst earnings estimates for FY 2013. From $46 that’s a 28% return.

Risks

As with any equity investment, risks to my price target include sales and earnings expectations that miss analyst expectations. In addition, the oil and gas industry is very cyclical so HP will be more sensitive to economic conditions than the average stock. Unexpected economic weakness could be very adverse to HP’s business. As with any single stock, positions should be taken in moderation as part of a properly diversified portfolio, and only at your own risk.

The Bottom Line

HP’s strong financial condition, high levels of profitability, and superior technology make it appealing relative to its peers. Though the economy may be a concern for the industry in general, HP has navigated through ninety years of volatile economic conditions. With a long history of consistent earnings and cash flow generation, I see no reason to believe that HP will not successfully manage the current business cycle. At $46 or better, HP looks like an attractive buy, in my opinion.

Victor K. Lai, CFA

Victor Lai does not hold any positions in HP. Bellwether Capital Management LLC client accounts may hold long positions in HP. This blog is for informational purposes only. Nothing on this blog constitutes investment, tax, or legal advice. You should conduct proper due diligence and / or consult with professional advisers before taking any investment action.