In fifth grade, I remember the “cool kids” at my school wore Guess jeans and a lot of hairspray (I wasn’t one of them). While hair spray has lost its popularity, Guess? Inc. has grown into a $2.4 billion dollar company that sells apparel in 90 countries around the world. Last week, Guess reported earnings that missed analyst expectations and its stock price fell by more than 21%. The negative surprise has many people second guessing whether or not GES is still a stock worth owning.

Since it was founded in the 1980s, Guess has primarily targeted teens and young adults with contemporary designer apparel. Staying relevant in such a market can be very challenging due to rapidly changing tastes and intense competition. However, Guess has demonstrated a persistent history of being able to compete successfully in a volatile business. Figure 1 shows how Guess has grown revenue, earnings, and cash flow over the past decade.

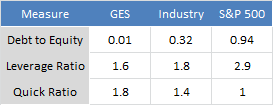

In terms of financial health, Guess is very strong. It has negligible debt and substantial cash on its balance sheet. Relative to peers Guess has lower leverage and higher levels of liquidity. Figure 2 shows some key financial measures for GES, its industry, and the S&P 500.

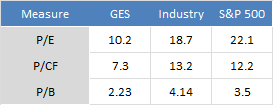

Currently trading around $26, GES’s trailing P/E of 10.2x is well below its historical average of 16.3x. At this level, GES’s PEG ratio has fallen below 1x to 0.62. Relative to peers, GES looks increasingly undervalued. For example, its 13.7% cash flow yield is currently 55% above the industry average. Figure 3 shows some key valuation measures for GES, its industry, and the S&P 500.

So, what are people second-guessing? Well, in addition to missing expectations, Guess may continue to face headwinds moving forward. Almost 60% of Guess’s revenues come from overseas, and more than 40% comes from Europe. Given the lingering European economic concerns, and weakness of the Euro, Guess’s management has provided cautious guidance for the year ahead.

These concerns may be valid, but I think the market is overreacting. Short of outright Armageddon, Europe will recover. Meanwhile Guess may face earnings pressure, but it certainly will not be Guess’s first time around the cyclical track. This company has successfully navigated through 30 years of economic booms and busts. Given its strong financial position and a long history of cash-flow-rich earnings generation, there is little reason to believe Guess will not survive the current cycle.

Of course, the market may not be done punishing GES for its recent misstep. And being a consumer discretionary stock, GES may even hit new lows should new economic concerns surface. However, when the smoke clears, I think GES will emerge trading at valuations that better reflect its fundamentals. As with any investment, positions should be taken with moderation, and of course at your own risk.

Victor K. Lai, CFA

This blog is for informational purposes only. Nothing on this blog constitutes investment, tax, or legal advice. You should conduct proper due diligence and / or consult with professional advisers before taking any investment action. Victor Lai, Bellwether Capital Management LLC, and BCM client accounts do not have any positions in GES at the time of this posting.