Given that it does, in fact, look like the “kitchen sink” is being tossed out the window, I thought I’d provide an example of something I consider to be a reasonable opportunity.

Cisco Systems (CSCO) designs, manufactures and sells products and services related to networking and information technology in general. Over the past year, CSCO stock has been put through the wringer, it’s down by more than 43% while the NASDAQ has been up by close to 5%. In fact, CSCO’s price has basically gone nowhere for the past 10 years. Primary reasons, according to various analysts, seem to be lackluster EPS performance and poor strategic business decisions. The disappointments were compounded by an overzealous CEO who basically promised investors that he would deliver double-digit growth. While CSCO the stock has clearly been beaten and battered, Cisco the company, in my opinion, is far from broken – here’s why.

The Big Picture

You’re reading this on your computer, or maybe even your smartphone. Whatever the case, increases in network traffic, bandwidth, capacity, and so forth are obviously on the rise all around the world. Like it or not, CSCO is still the 800-pound gorilla in the room. When it comes to networking, CSCO is the industry leader with 50% market share in routers and 70% in switches. While the competition is up and coming, CSCO enjoys a strong advantage in that the costs of changing vendors (with respect to CSCO’s customers) are high. Customers that already use Cisco products and services will need very compelling reasons to change vendors. Consider, for example, that “Cisco certification” is not expected to be replaced with “HP certification” anytime soon. Case in point, Cisco has a strong position in an industry that is expected to grow.

The Numbers

Analysts have criticized CSCO for lackluster growth, and they’re right – neither revenue nor earnings growth has been spectacular – but relative to what? Maybe relative to the broad tech sector in general, but relative to industry peers CSCO has actually been outperforming. Figure 1 shows the average sales and earnings growth for CSCO over the past five years relative to peers.

In terms of financial health, CSCO is as solid as a rock. Based on its most recent balance sheet, CSCO is showing over $6.6 billion in cash, and $36.7 billion in short-term investments. While its debt to equity ratio is a bit higher than its peers, its overall capital structure is healthy and is nothing to be worried about. It’s also worth noting that most of Cisco’s debt is long-term, meaning not much is due in the near future. This leaves Cisco with high levels of solvency and liquidity, shown by its strong current ratio. In addition, the long-term nature of its debt may be beneficial given the current low-interest rate environment. Figure 2 shows the debt to equity and current ratios for CSCO and its peers.

Figure 2 Financial Health

Despite its healthy financial condition and a positive industry outlook, CSCO is trading at a discount relative to its peers. Figure 3 shows CSCO’s current price ratios based on trailing 12-month cash flow and net earnings. In addition, it’s worth noting that despite generally negative analyst sentiment about performance, CSCO has actually delivered a strong return on equity over the past 5 years (shown in Figure 3 as a 5-year average). At the end of the day, isn’t ROE exactly what equity investors are looking for?

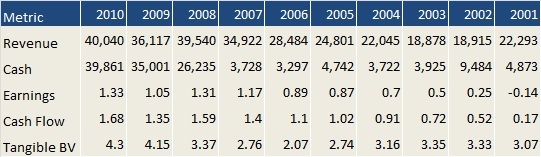

To sum up the numbers, Figure 4 shows a snapshot of what CSCO has done over the past 10 years. In a world of uncertainty, CSCO has consistently grown sales, earnings, cash flow, and book value for the past decade.

The Risks

When investing in stocks, there is never any shortage of risks. The heightened possibility of a coming recession would certainly be negative for stocks in general. Cisco is sensitive to business spending, and businesses may postpone capital spending plans should economic uncertainties increase.

Something timely to note is that Cisco is slotted to report earnings later today after the market closes. From last quarter’s guidance, we know that Cisco is going to take a big charge against earnings related to the recent restructuring of its business lines. In addition, it also warned that revenue would be flat and margins would narrow. Should Cisco deliver results that disappoint estimates, its stock will almost certainly be punished further.

A potential long-term risk is that management continues to make poor strategic business decisions. In the past, it has entered into some questionable markets that it had no competencies in or synergies with. For example, the well known “Flip” video debacle. As Cisco continues to stockpile cash, some investors see it as a chance for management to make another bad acquisition.

As a final note, CSCO’s higher than average beta will mean more volatility than average should the markets continue in fear mode. Case in point, it’s not for the risk-averse or faint of heart.

The Bottom Line

Yes, Cisco has made some bad decisions. The “flip” side to that is management has shown a willingness to own up to mistakes and make changes. CEO John Chambers has conceded that sustained double-digit growth is just not realistic. Cisco has spent the past year restructuring and reorganizing. It is exiting underperforming businesses, refocusing on its core competencies, streamlining operational inefficiencies, and slashing costs in general. Based on a combination of relative valuation and discounted cash flow analysis, my estimate of fair value for CSCO is $19.

Given the current market volatility, and the potential for slowing economic growth I can’t put a finger on when that target will be hit. But given that CSCO’s situation does not change for the worse I am confident that it will eventually trade back in line with a valuation that better reflects its fundamentals. Keep in mind that Cisco is a huge company, with a $76 billion market cap, CSCO isn’t the kind of stock that we can expect to quadruple in value (the math just doesn’t work that way). With that said, barring any unforeseen circumstances, a further drop in price represents an even better buying opportunity, in my opinion.

The bottom line, currently trading under $14 a share, I think CSCO is a good long-term buy as an addition to a properly diversified portfolio.

Victor K. Lai, CFA

Victor Lai, Bellwether Capital Management LLC, and/or its clients, either own or intend to own shares of CSCO stock. This blog is for informational purposes only. Nothing on this blog constitutes investment advice. Bellwether Capital Management LLC does not provide tax or legal advice. You should conduct proper due diligence and/or consult with your professional advisers before taking any investment action.