Gold is popular, to say the least. People have conjured up more cliches and trite sayings about the metal than any other. But this year “all that glisters is not gold” (h/t Shakespeare). From April to September gold saw an intra-year drawdown of about -19% while the S&P 500 was down by nearly -15%.

Figure 1: Gold vs S&P 500

That caught some investors by surprise because gold is commonly seen as a safe haven and a hedge against risky assets like stocks. Gold’s drawdown this year might be explained by unique circumstances like the spike in interest rates and US dollar strength (gold prices are sensitive to both). Regardless of what happened this year, the bigger question is should we view gold as a safe haven and a hedge, to begin with?

Gold as a hedge

We can evaluate gold as a hedge by looking at the historical correlation of returns between gold and risky assets like stocks. Chart 2 shows a linear regression of annual gold returns against S&P 500 returns from 1928 to 2021.

Figure 2: Gold & Stock Returns

The slight negative correlation of -0.0737 and coefficient of determination (R-squared) of 0.0043 implies stock returns explained an insignificant level of gold returns. In other words, historically when stock prices fell, gold prices generally did not rise to offset losses in annual terms (not meaningfully, anyway).

If it did, we would expect to see a tighter fit around a more negatively sloped trend line. This data suggest gold and stocks are more non-correlated than negatively correlated. Which in turn implies gold does not exhibit the hedging characteristics it is commonly credited with.

Gold as a safe haven

The lack of a negative correlation with stocks does not mean gold cannot be a safe haven. For example, cash is one of the best-known safe havens even though it is not negatively correlated with stocks.

But gold falls short of safe haven status in another way. If we define risk as volatility of price and uncertainty of return, then gold is not low-risk. For example, gold prices peaked near $2600 in 1980 and then fell by more than -80% until bottoming around $445!

Figure 3: Gold Prices

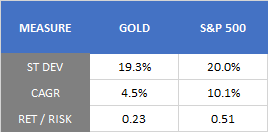

A low-risk, safe haven asset should not exhibit such extreme price movements. The magnitude of gold’s swings was more similar to high-risk assets like stocks. For reference, from 1928 to 2021 the annual volatility of return (standard deviation) for the S&P 500 was 20.0% and it was 19.3% for gold.

Figure 3: Risk & Returns Statistics

Not only were gold returns nearly as volatile as stock returns, but the annualized return for gold was less than half of the S&P 500’s. In other words, for every unit of risk taken, an investment in the S&P 500 provided over 2x more return than gold. From that perspective, gold does not look like a low-risk safe haven, and not even like an attractive investment.

Gold still glitters

Despite gold’s shortcomings, people, investors, and governments continue to hoard it all around the world. One possible reason is that gold can still be a good portfolio diversifier, which is different from being a good hedge. While effective hedging requires negative correlation, diversification only needs non-correlation to work.

Proper diversification combines non-correlated assets to reduce portfolio volatility and improve risk-adjusted returns over time (less risk and more return). As Figure 2 showed, gold and stock returns showed little to no correlation historically. So gold can be a good diversifier for a stock portfolio.

Consider a simple example using three portfolios.

a) 100% Gold

b) 100% U.S. stocks

c) 80% U.S. stocks + 20% Gold.

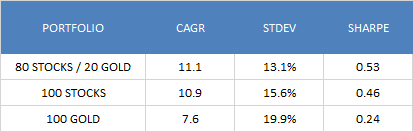

Backtesting from 1972 to 2021, stocks delivered annualized growth of 10.9% per year and gold delivered 7.6%. During that period stocks had a lower standard deviation than gold, 15.6% vs 19.9%, respectively. Based on those statistics, 100% Stocks seem like the best investment (higher return and lower risk).

But surprisingly, the 80/20 portfolio delivers higher return (CAGR), lower risk (st dev), and better risk-adjusted performance (Sharpe) than either 100% Stocks or 100% Gold. This was possible because the non-correlation between stocks and gold reduced overall portfolio volatility and produced smoother compound annual growth over time. Summarized in Figure 4 below.

Figure 4: Portfolio Statistics

A reasonable bottom line

Based on historical data, gold does not appear to offer a meaningful hedge against risky assets like stocks and does not behave like a low-risk safe haven asset. However, gold can still be an effective portfolio diversifier that helps reduce portfolio volatility and improve risk-adjusted returns over time.

The most avid precious metal bulls may also point out gold provides physical utility and tangible value that cannot be fully explained by statistics. If nothing else, gold can still conduct electricity and glitter as jewelry. Bulls might also add another cliche, “buy gold because they stopped making it a long time ago.” Admittedly, that is all more than we can say about fiat or digital currencies.

This is not a bullish or bearish opinion on gold, and I do not have a price target for the metal. This is a reminder we should be clear about our reasons for investing in gold, or anything else. We should also be willing to objectively evaluate relevant data and recognize how information does or does not support our reasoning. Said another way, do your homework and do not just invest based on trite sayings.

A year-end note

2022 has been a challenging year, it is not easy or enjoyable to navigate bear markets. At BCM, we managed to do relatively better than the broad markets because we reduced our risk exposure across portfolios early in the year. However, “relatively better” is still negative for the year, and that is never easy or enjoyable to endure.

At BCM our objectives were to avoid the worst of the drawdowns, survive the volatility, and be positioned to re-risk when economic and market conditions improve. Although we do not believe we are “in the clear” yet, we have been able to achieve the first two objectives so far. As 2022 comes to a close we are one step closer to the third.

I want to thank our clients, families, and friends for their continued trust and confidence in BCM. I am thankful and grateful for you all and wish you the very best this holiday season.

—

Victor K. Lai, CFA

See the original version of this article at SeekingAlpha.com.

You must be logged in to post a comment.