MARKET OVERVIEW

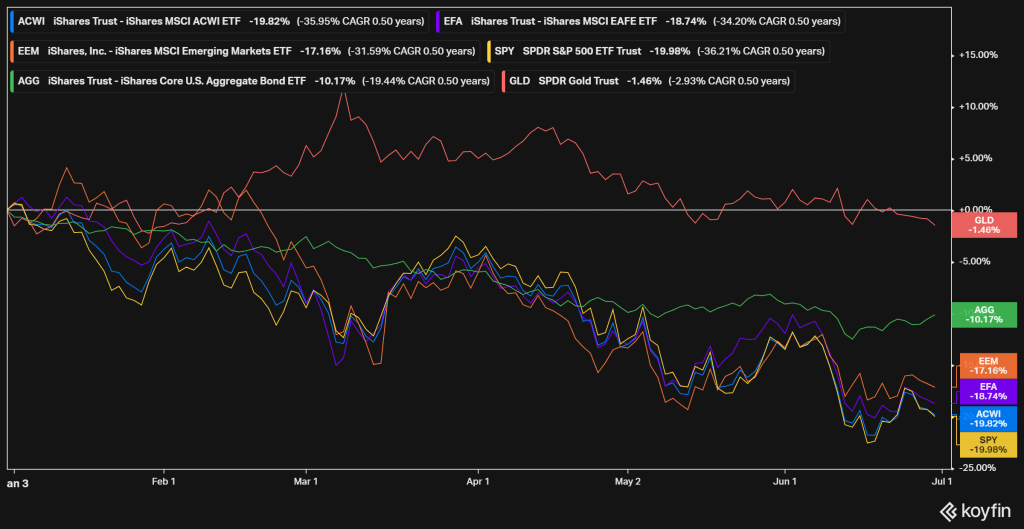

The global sell-off in financial markets accelerated during Q2. Global equities officially entered a bear market, breaching the technical definition of a -20% decline. US stocks were down most, but all major equity regions were down double digits year-to-date. Even the US bond market was off by -10% for the year.

Figure 1: Global Markets

MACRO PERSPECTIVE

The likelihood of a US recession continues to rise. Over the past seven months, I’ve written about how various leading indicators turned negative. Among the most severe is new home sales, which deteriorated further in May with a big miss.

Figure 2: New Home Sales

The 2-10 Treasury yield curve, which recovered after a brief inversion in March-April, briefly inverted again in June and remains only several basis points flat.

Figure 3: Treasury Yield Curve

Except for Japan, leading economic indicators around the world have been deteriorating since late last year, shown below as Composite Leading Indicators from OECD.

Figure 4: Composite Leading Indicators

One of the last vestiges supporting the case for soft-landing is strong employment and consumption. Labor markets are tight, wages are up, and it is difficult to contract without a pullback in spending (especially in the US).

However, despite rising nominal wages, the real, inflation-adjusted value of those wages has decreased. Rising prices for non-discretionary items like food, energy, and housing will have a crowding-out effect on other areas of spending.

Figure 5: Real Median Wages

Meanwhile, there are cracks forming in the labor market. One of the best leading indicators for employment, jobless claims, is trending upwards.

Figure 6: Initial Jobless Claims

Finally, the US Central Bank’s surprise 75 basis point hike in June may have marked the end of the Fed Put era when ever-easing monetary policy could be counted on to bail out markets. With headline CPI roaring near 9%, Chairman Powell & Co have double-downed on their position to fight inflation.

Ironically, a Fed tightening-induced recession may be the undesirable solution to the equally undesirable problem of inflation.

INVESTING COMMENTARY

At BCM, we continued to decrease risk exposure during the quarter, as we have been doing since the start of 2022. At this point, our portfolios are at their maximum tactical underweight of risk assets, which is approximately half of strategic targets.

Within risk assets, we are overweight consumer staples for defense and overweight materials, select emerging markets, and gold due to inflation. For non-risk assets, we continue to be heavily weighted towards short-term Treasuries and investment-grade bonds.

However, as yields rise and broader bond market exposure becomes more palatable, we expect to increase our allocation opportunistically. Meanwhile, cash equivalents are an acceptable alternative for the first time in many years with yields finally off the zero level.

Despite our pessimistic outlook for risk assets, we do not make extreme “all or nothing” changes to portfolios. That can increase risk by causing a portfolio to deviate outside its range of expected and acceptable outcomes.

For example, making an extreme move to 100% cash due to perceived stock market risk could actually be riskier than maintaining some stock exposure. Market reversals can happen abruptly and aggressively, and missing rallies can hurt as much as taking losses.

The pandemic crash and recovery experience of 2020 was a recent example. Many equity investors, expecting the worst, moved to cash during Q1 2020 only to watch in horror and disbelief as stocks violently soared to new highs in the weeks that followed.

Those investors not only realized losses but also missed out on the short-lived opportunity to recover them. In hindsight, many would have been better off by simply staying invested. I’m not suggesting this is a repeat of the pandemic crash. I’m recognizing I don’t know what happens next and I could be wrong.

Our current underweight of risk assets enables us to limit drawdowns and endure expected volatility, but also maintains some market exposure supportive of a quick position reversal if needed.

We don’t know what happens next, but we are watching carefully, waiting patiently, and making adjustments as conditions change. We’ll keep you apprised of what we are seeing and doing along the way.

—

Victor K. Lai, CFA

You must be logged in to post a comment.