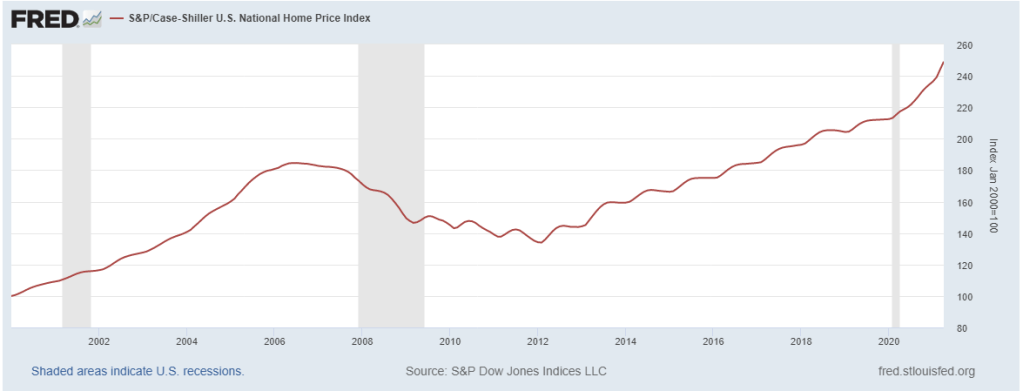

Back in January 2011 I wrote “I think one of the most attractive domestic investment opportunities is also one of the most detested – real estate.” Obvious and easy in hindsight, but in 2011 many people were still licking their wounds from one of the largest real estate crashes ever. People were scared silly and wondering if house prices would ever find a bottom. It took another year for the market to finally bounce and since then prices have surged past the highs of the financial crisis, shown in Figure 1.

Figure 1

I put my own money where my mouth was and closed on seven personal real estate transactions over the past decade. It’s been a good run, but as Stein’s Law states “if something cannot go on forever, it will stop.”

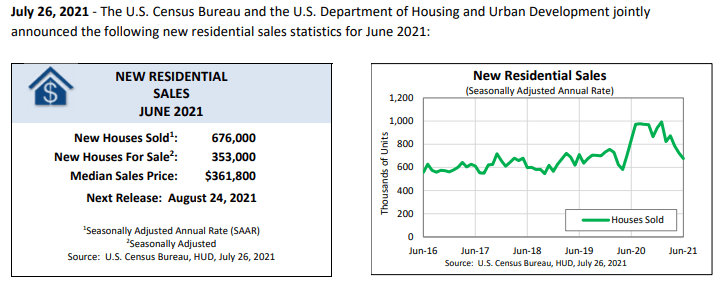

To be clear, I’m not calling a top and I don’t know when this party officially ends. But I do think the easy money has been made in real estate and it’s time to pay attention. One data point I’m watching is new residential home sales. The most recent figures (for June) saw a sharp YoY pullback of more than 19%, shown in Figure 2.

Figure 2

That followed a series of weakening figures that may have peaked early this year. Could it just be a correction of the spike we saw in the second half of 2020? Could it be the subsequent breakdown in supply chains? Or could it simply be buyer fatigue from the breakneck pace of price increases? I think it’s all of the above.

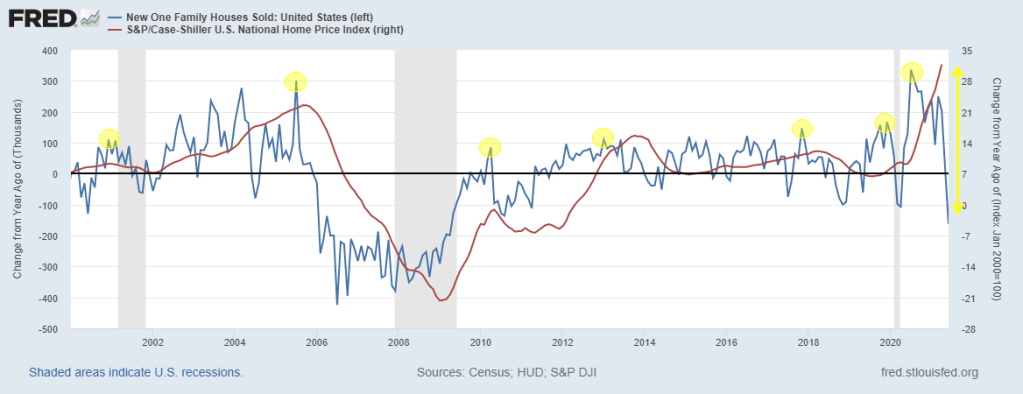

Regardless of the backdrop, new home sales are useful to watch because they tend to be a leading indicator of real estate prices. Figure 3 shows the YoY % change of new home sales (blue line LHS axis) versus YoY % change in average home prices (red line RHS axis).

Figure 3

Notice that peaks in new sales (blue line) tend to precede pull backs in prices (red line). This makes sense because sales reflect demand which obviously affects prices. One way or another I expect to see reversion of the current sharp disconnect.

Beyond real estate prices, new home sales also tend to be a leading indicator of the business cycle. In other words, new home sales tend to peak prior to economic recessions (shown as grey bars in Figure 3). This makes sense because both the construction and purchase of housing requires substantial long-term planning and investment for all parties involved. That far-sightedness makes housing activity sensitive to expected changes in economic conditions.

The silver lining to a downturn in new home sales is a long lead time with respect to the business cycle. It can take many months, even years, for a recession to show up, and sometimes it doesn’t at all. I don’t think the current move in new home sales by itself is a harbinger for a near-term recession. As I’ve been writing all year it will take a huge shock (more than just weakening home sales) to stop the momentum of this runaway economic train.

On the other hand, real estate prices could certainly pull back regardless of where we are in the business cycle, and I think that’s what new home sales data are warning now. Of course, there’s no such thing as a perfect indicator. False positives abound and heaven knows I’ve been wrong plenty.

Indicators aside, let’s just recognize the real estate market has been so good for so long it’s easy for people to let their guards down and ignore warning signs (ditto for most markets, actually). It’s easy to believe prices will only rise, but that’s as unreasonable as thinking prices would never bottom in 2011.

The bottom line is that it’s time to proceed with caution. Although we cannot predict the future, we can pay attention to the data, adjust as it changes, and not lose sight of the fact that all good things eventually come to an end.

—

Victor K. Lai, CFA

You must be logged in to post a comment.