QUARTER REVIEW: PRECEDENTS

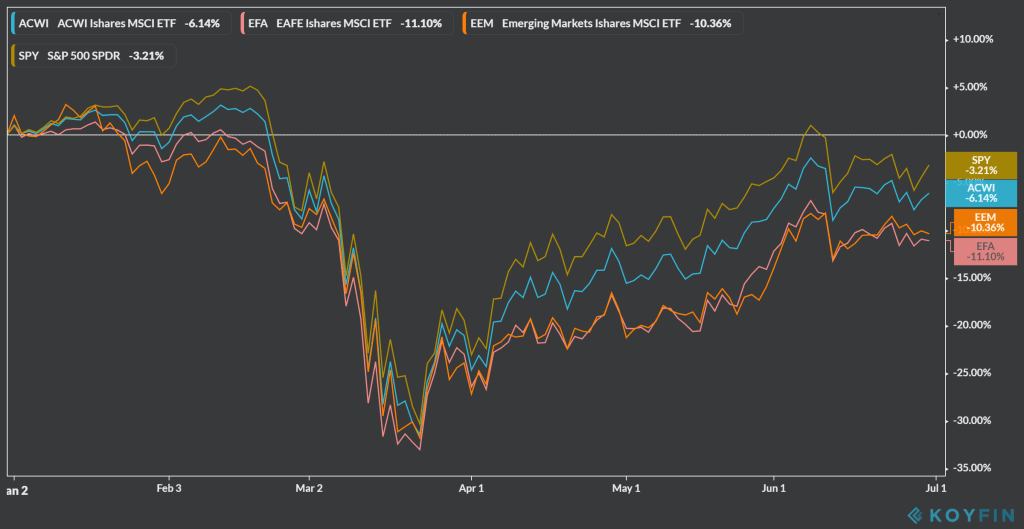

Equity markets set back to back records year to date. In Q1 the MSCI ACWI (global stock market) suffered one of the fastest bear markets in history only to claim one of the fastest rebounds ever in Q2. Full circle the ACWI is down -6% as of June 30.

Figure 1: Global Equity Markets

The unprecedented times “unprecedented” was used to describe the markets indicates how difficult it was/is to predict this year’s swings. To wit, although our underweight of risk exposure in Tactical Allocation helped us dampen the Q1 drawdown, it also muted gains during the Q2 rally.

On balance this worked in our favor as stocks are still down for the year. Although we clearly missed some of the fast money in Q2, we believe the reasons for our conservative positioning remain sound. We’ll review them along with our outlook below.

ECONOMIC AND MARKET CONDITIONS

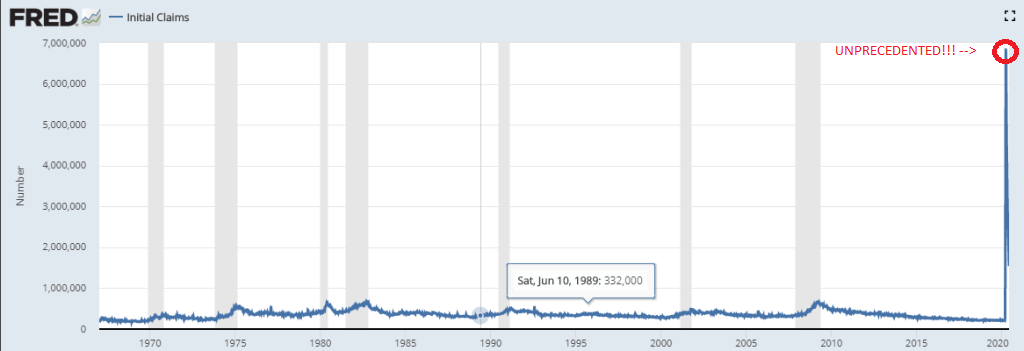

Economic conditions are truly unprecedented. A look at jobs makes that clear. Employment is one of the most important drivers of the US economy. The number of jobs lost during the COVID-19 pandemic is unlike anything we’ve experienced. For reference, the US lost 2.5 million jobs during the Great Financial Crisis. As of May, the pandemic has caused job losses of 36 million.

Figure 2: Initial Jobless Claims

Global economic activity fell off a cliff and the world is in a synchronized recession.

Figure 2: Global Composite PMI

Figure 3: Global Recession

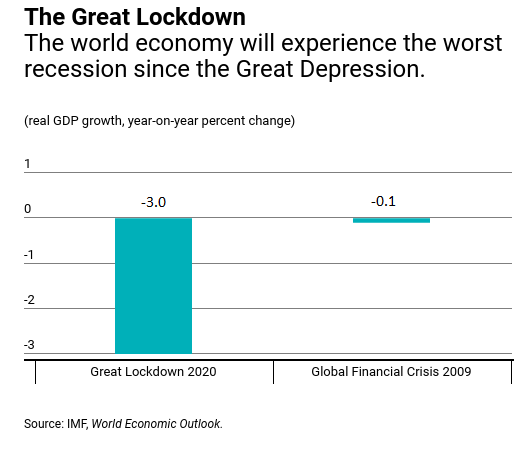

Forward-looking economic indicators have collapsed to levels below the depths of the Great Financial Crisis and the International Monetary Fund expects the worst contraction since the Great Depression.

Figure 4: Composite Leading Indicators

Figure 5: IMF Forecast

Meanwhile, equity markets have whistled past the dismal data. That divergence is clearly visible when contrasting the advance of the S&P 500 with the decline in forward earnings.

Figure 6: S&P 500 vs Forward Earnings

The optimistic viewpoint is the market is looking ahead to a “v-shaped” recovery. Recent data show some indicators are bouncing. For example, a surprise +2.5 million in payrolls from the May employment report.

The question is will the improvements be meaningful and sustained or noise? The answer is nobody knows for certain. The best we can do is watch relevant data and monitor them for trends and confirmations.

TACTICAL ALLOCATION

By March of 2020 we observed uniformly negative economic conditions combined with a breakdown in market conditions. That called for a maximum underweight of risk exposure in the Tactical Allocation strategy (TA). The shift was fortuitous given the steep drawdown in March.

However, global equity markets rallied hard in Q2. While improving market technicals led TA to marginally increase risk exposure, persistently negative economic conditions kept TA anchored at an overall underweight. That resulted in forgoing some returns, but all things considered the shift was a net-positive for TA since stocks are still down year-to-date

Waiting for economic conditions to improve does involve the ROMO (risk of missing out). However, it also protects against the risk of being early. Historically, being late to a bull market has yielded better results than being early in a bear market. Being late resulted in both a higher average return and a higher success rate, summarized below. What really stands out is 100% of “late” instances resulted in positive return while only 69% of “early” were positive.

Figure 7: Early vs Late

Market strength by itself, without the support of economic strength, is more likely to be ephemeral than sustainable. As of now, economic data is mixed at best. While some indicators (like May employment) were stronger than expected, others (like Q1 earnings) are coming in worse than expected.

If history is any precedent, the prudent choice is to patiently wait for confirmation, rather than impatiently act in haste. The bottom line is TA remains underweight risk exposure at present. However, we recognize the data is changing and will adjust our risk exposure as economic and market conditions warrant.

—

Victor K. Lai, CFA

You must be logged in to post a comment.