An excerpt from my recent article published at SeekingAlpha.com.

Passive investing has enjoyed a tremendous rise in interest and popularity from investors over the past decade. Following that rise, the number of passive investment products, like index funds and ETFs, has also taken off. So much so that some fear passive investing is the next big bubble to burst. We’ll take a closer look at the argument in this article.

Summarizing the argument

The passive bubble argument can be summarized as follows.

- The rise in popularity of passive investing is leading to large capital flows into passive products.

- That is inflating the market prices of underlying securities because passive investing buys them indiscriminately and often through synthetic exposure.

- This is creating a bubble in passive investments, the eventual unwinding will be disorderly and losses will be large.

Some well-respected investors, like hedge-fund manager Michael Burry, believe the rise in passive investing resembles the frenzy that led to the financial crisis of 2007 to 2009. Here is Burry in his own words from a Bloomberg interview, “This is very much like the bubble in synthetic asset-backed CDOs before the Great Financial Crisis in that price-setting in that market was not done by fundamental security-level analysis, but by massive capital flows based on Nobel-approved models of risk that proved to be untrue.”

Adding context

Burry makes some good points. There’s no doubt there’s been a substantial rise in the number of passive vehicles and their AUM over time. Burry’s not the only one warning about passive vehicles, there are plenty of scary statistics thrown around about how the passive world looks bubbly.

For example, here’s a chart from wsj.com showing eye-catching growth in the percentage of US equity market cap held by index funds.

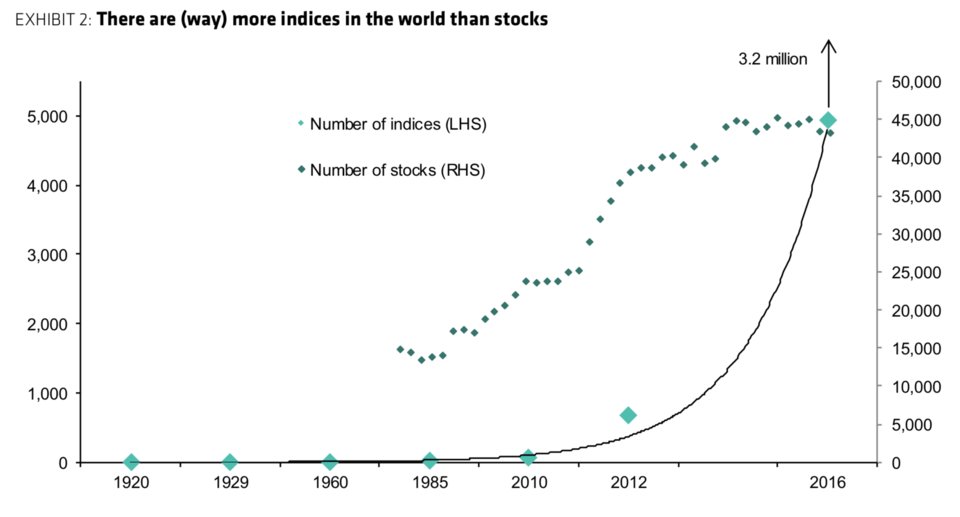

And here’s a chart from businessInsider.com showing a parabolic rise in the number of indices (versus stocks) over time.

These charts look shocking but they can also be misleading without proper context.

Read the full version of this article a SeekingAlpha.com.

Victor K. Lai, CFA

You must be logged in to post a comment.