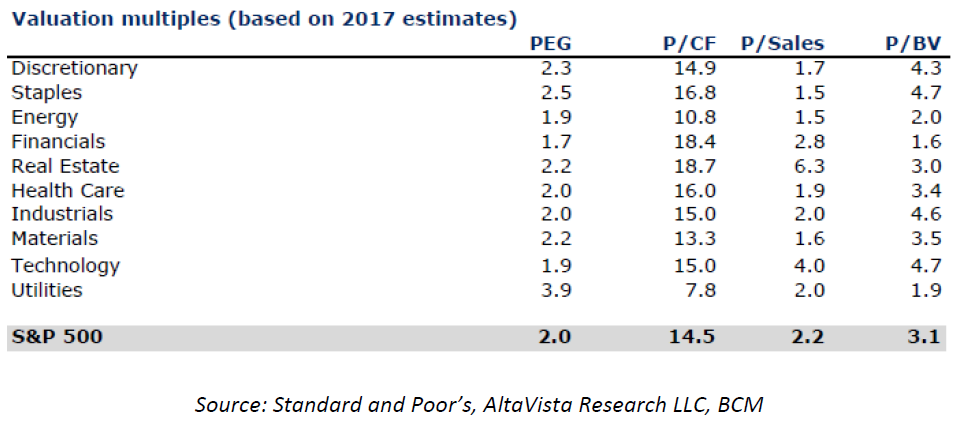

Both the ACWI and the S&P 500 gained more than 20% in 2017. US stocks continue to look expensive. Of course, that doesn’t mean they can’t continue to climb — they’ve looked expensive for several years. But 2018 may be the year to be more selective. The table below shows the trailing P/E ratios for US equity sectors based on forecasted 2017 earnings.

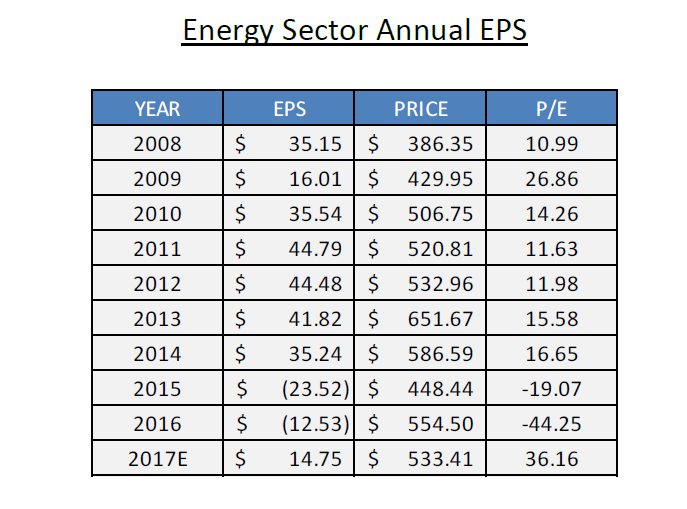

Valuations look high across the board. And at the surface, energy looks most expensive at 36x earnings. But digging deeper yields some unexpected results. Energy took large write-downs in 2015 and 2016 when oil prices collapsed into the $20’s. Reported earnings were negative for both years. Not only was that abnormal, but it also makes valuing on earnings difficult.

The 36x multiple assumes eps of $14.75 for 2017. Relative to history, that’s low, but makes sense since we know earnings are bouncing off a negative level. If we exclude the abnormal reads, normalized eps for the sector are about $36 (by coincidence).

If we assume earnings will normalize, that brings the multiple, at current prices, to about 14x. That’s obviously much better than 36x and actually makes energy look undervalued relative to other sectors. Other measures seem to agree. Energy is tied for least expensive in terms of growth and sales, second in cash flow, and third in book value.

This looks so even as most other sectors are hitting record revenue and earnings, which should make them look less expensive (not more) relative to energy. Point is energy looks relatively undervalued. But honestly, I’m not thrilled about it. This is like wearing the least smelly of the dirty laundry. But in the US, energy may be one thing that passes the valuation sniff test.

Keep in mind since valuations are not absolutely cheap, there’s less cushion. Many energy companies are still recovering from the oil rout. Should oil prices slump again or economic conditions deteriorate, people will be reminded the sector is not as conservative as some think. Let’s not forget the sector saw a drawdown of 53% during the financial crisis.

Victor K. Lai, CFA

This blog is for informational purposes only. Nothing on this blog represents advice of any kind. Investing is inherently risky and involves the risk of potential loss.