US stocks are at all-time highs and many valuations measures suggest they are expensive. That doesn’t mean the market can’t keep rising and it’s proven bears wrong for years. However, it’s fair to say US stocks don’t look cheap by traditional standards.

It’s actually getting hard to find any market that looks like a compelling value. Sure, there may be specific concerns teetering on the brink of insolvency (Venezuelan bonds anyone?), but from a big picture perspective, most assets look pricey.

Foreign equities look less overvalued than the US, but are also up by more. Emerging market stocks surged over 24% in the past year. Oil is nowhere near its $20-something lows, and even gold had a nice bounce from the $1,000 level. Meanwhile, bond yields remain depressed across the board.

It seems the low yields on fixed income have caused more investors to reach for yield in riskier assets. That, in turn, has fed into a cycle of higher prices and greed. For example, CNN Money’s Fear & Greed Index registered a 61, or greedy, as of August 29.

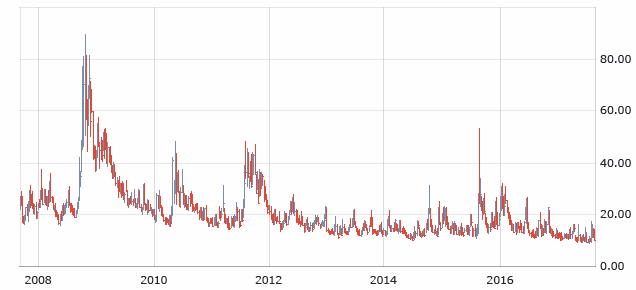

That reading is in line with the market’s “fear gauge,” or VIX, which shows low levels of concern. Historically the VIX averaged around 20 and peaked at over 80 during the financial crisis. But over the last year, the VIX has bounced around 10. There is the recent uptick from North Korean scares, but overall the VIX has been abnormally low.

The VIX doesn’t look much different from other periods of market calm, but given its tendency to spike the VIX may be one of few things in the market that look relatively cheap. The problem is the VIX isn’t actually an investable asset. It’s an index derived from option contracts on another index. The closest investors can get to it is indirect exposure to financial products made to track the VIX (which adds yet another layer of intangible-ness).

To that end, investors should understand the idiosyncrasies of the products they use. For example, options on the VIX are European in style. They can only be exercised or assigned at maturity, which causes deltas to be muted until the options are close to expiration. The options can work well for investors who expect movement (or no movement) in the VIX within a specific time frame. But they may not work well for profiting from short-term swings.

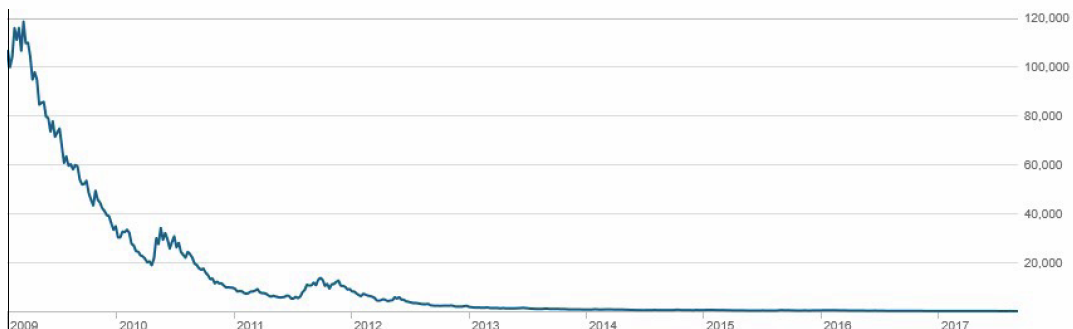

Meanwhile, most VIX exchange-traded funds and notes are susceptible to contango. The products can lose value to time decay as they roll from front month to longer-dated and higher priced contracts. That makes these products better for short-term trading, and terrible for “buy and hold” (even more so for the leveraged variety). The chart below shows price over time for VXX, one of the most popular VIX exchange-traded products.

Investors are both gobbling up risk assets and fairly complacent. The Oracle of Omaha might say this is the time to be fearful, and yet volatility (as measured by the VIX) looks abnormally low and inexpensive. That makes volatility an attractive contrarian position in my opinion. Whether you decide to go long or short volatility, just make sure the product you’re using accurately reflects your position.

Victor K. Lai, CFA

This blog is for informational purposes only. Nothing on this blog represents advice of any kind. Investing is inherently risky and involves the risk of potential loss. Victor Lai is long VXX.