Seems like everybody hates solar stocks. They’re down big, but with reason. Earnings have been dismal and financials have been deteriorating. Prominent names like Solar City and Sun Power are simultaneously burning through cash and piling up debt. Adding insult to injury, two years of capitulating oil prices have softened demand for alternative energy. Things look gloomy for solar but step back enough and the outlook gets brighter.

The reality is demand for alternative energy will rise over time. The simple truth is we need more energy than we have dirty fossil fuel. Solar power is clean, abundant, and technically free — solar technology gets cheaper by the day. That paints a positive long-term picture for the solar industry. And even near-term, things could surprise to the upside. In December 2015 Congress approved five years of solar investment and production tax credits, and that could boost activity near-term.

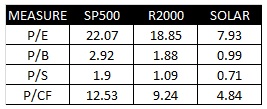

Despite the bright spots, solar stocks are down almost 60% from highs reached in April 2015. At this point, even if they’re not undervalued in absolute terms, they’re certainly undervalued relative to the broader market.

Even if the broad market didn’t look expensive (which it does) solar stocks would still look relatively cheap. Of course, there will be winners and losers, but as I wrote before solar stocks can be complicated and tricky to analyze. I wouldn’t venture into picking out single stocks unless I had some special insight into the industry (which I don’t). Also, there’s no telling if solar stocks have found a bottom. Sales and cash flow have been under pressure and if they don’t improve prices could stay lower for longer.

But all things considered, I’m still long-term optimistic. With current sentiment very negative and valuations already attractive, I think solar stocks are worth a look. If you take a position, average into it slowly on price weakness. Unless you’re keen to what industry segments to prefer, stay as wide as possible (from design and manufacturing to distribution and installation). And of course as with any value play, be tenaciously patient.

Victor K. Lai, CFA

This blog is for informational purposes only. Nothing on this blog represents advice. Investing is inherently risky and involves the potential for loss. Victor Lai is long TAN.