At year-end 2025, consensus expectations were for a continued rally in risk assets. Economic conditions looked strong, earnings were beating estimates, and stock markets were making new highs. There was little to dislike. Equity analyst forecasts for the S&P 500 ranged from 7100 to 8100, predicting another double-digit year.

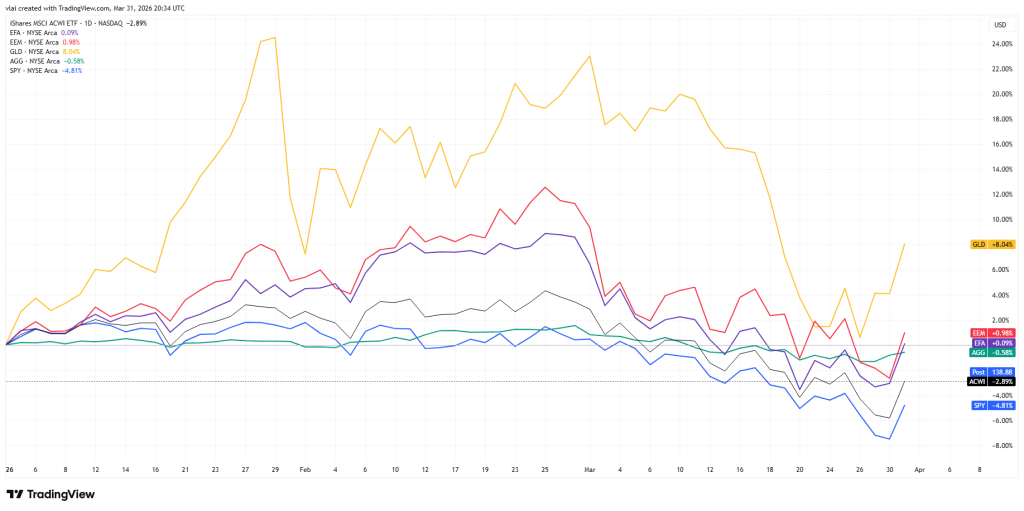

One quarter doesn’t make a year, but markets moved against consensus expectations in Q1. Global stock market prices (ACWI) were down -3% ytd, and US stocks (SPY) were down -5%. US bond market (AGG) prices were also down -1% for the quarter. Gold, once again the outlier, was up +8%.

Global Market Q1 2026

MACRO VIEW

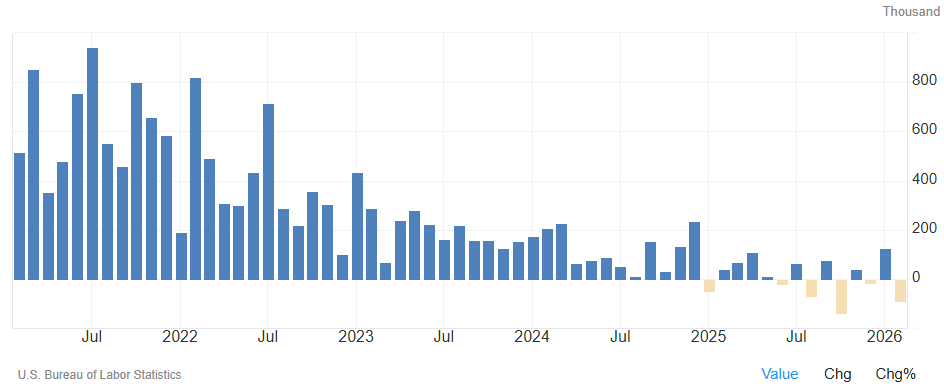

As I wrote in Q4, US employment conditions were weakening. That weakness is persisting in 2026. Not only did February post another month of job losses, but the BLSs’ final count for 2025 job creation was only +181k for the year. Too put that number into perspective, the US was previously adding several hundred thousand jobs per month.

US Non-Farm Payrolls

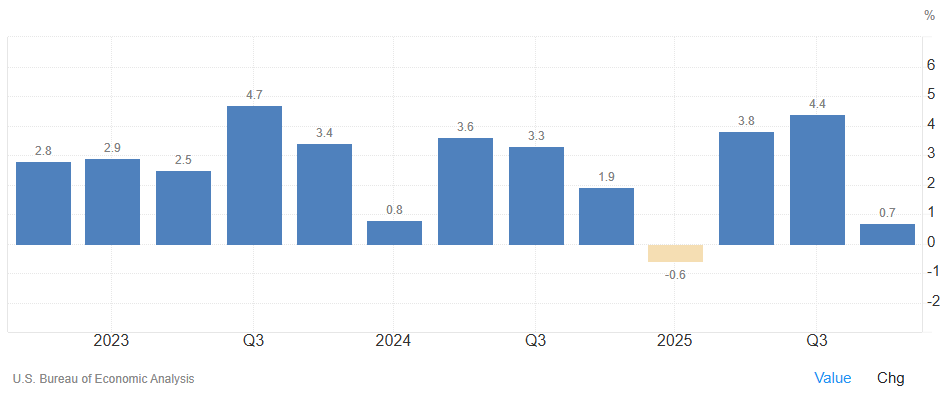

Meanwhile, US economic growth was revised down to a stall speed of just +0.7% for Q4 2025. This was a significant slowdown from the more than +4% growth achieved in Q3.

US GDP Growth Rate

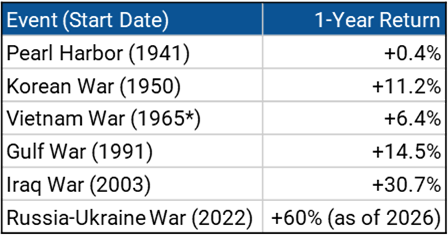

If the outlook were not hazy enough, now the US must also see its way through the fog of war. Some fear the war may mark the start of the next market crash. Yet, markets have been more resilient to war than commonly assumed. For example, while US stocks usually fall at the start of wars, they actually tend to be positive 1 year later.

S&P 500 & Wars

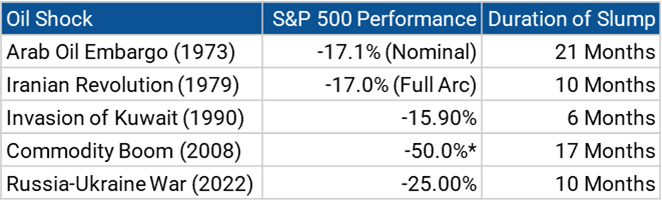

One important exception is an oil price shock. The presence of an oil shock, with or without a war, typically results in prolonged equity market weakness and, no surprise, recessions. The current spike in oil prices, therefore, introduces a relevant current risk to the economy and markets.

Oil Shocks & Markets

Sources: S&P Global, BCM.

MARKETS & INVESTING VIEW

As the wall of worry continues to rise, markets have avoided a free fall. The S&P 500 is down year-to-date but still hasn’t breached the threshold for a common correction of -10%. Of course, every correction starts with less than -10%, and every crash starts with a correction.

So, the billion-dollar question is, “Will the current market volatility escalate into a larger drawdown?” The honest answer is “I don’t know.” Nobody really does, not even ChatGPT (I asked). The best we can do is make educated guesses based on past precedents.

To that end, crude oil prices are a crucial factor. Historically, when oil prices stay above $100 per barrel, it becomes a meaningful drag on the economy. Oil is used in the production of everything from clothing to medicine. Even when products aren’t made of oil, their import and transport mean they’re still affected by oil prices.

For a net importer like the US, higher oil prices become a hidden tax on almost everything. As prices rise, so will inflation, and eventually the Federal Reserve could be forced back into raising interest rates. For markets and an economy that have been anticipating rate cuts, that could be the straw that breaks the camel’s back.

The next question then is, “What will happen to oil prices?” Again, nobody really knows, but that likely depends on what happens with the war in Iran and the Strait of Hormuz. The strait, located in the Persian Gulf, is a vital corridor for global energy supply that moves about 20% of the world’s oil. As long as Iran holds the strait hostage, oil prices are unlikely to subside.

This may be the most significant and miscalculated risk in markets now. President Trump and his administration are promising quick resolution. There was even news today that Iran is willing to negotiate. Many investment strategists recommend looking through the conflict and focusing on better conditions down the road. And judging by market reaction, most investors agree.

Yet, history shows otherwise. Conflicts in the Middle East are rarely short-lived. They usually last longer, cost more, and are more consequential than politicians promise. With the exception of the Gulf War of 1990-1991, every US conflict in the Middle East has languished for years. It’s reasonable to assume that things won’t be different this time.

Of course, we’re not experts on war or geopolitics. Maybe President Trump pulls off a last-minute diplomatic deal, or maybe Iran surrenders. We don’t know. What we do know is that the fog of war adds another layer of complexity onto an already challenging outlook.

That reinforces our cautious position. We continue to hold an underweight position in risk assets and an overweight in high-quality bonds. Fortunately, both moves worked in our favor in Q1. While we don’t know how conditions will change in 2026, we do expect continued volatility ahead. Therefore, we continue to hold our current positions and stay ready to adjust as conditions change.

—

Victor K. Lai, CFA

You must be logged in to post a comment.