Emerging markets are down close to 7% YTD as of the end of July. The reasons are various — rising interest rates, softening economic data, and US tariffs to boot.

Unrecognized headliner

China is on the front page because of the trade war and its equity market was down over 20% from its YTD highs. But the unrecognized story is the Brazillian equity market, which was down more than 30% from its high.

Source: Yahoo Finance

In addition to EM macro issues, Brazil is also dealing with an uncertain presidential election and a massive trucker strike that shook its burgeoning economic recovery.

The market reaction was swift and fierce, but also likely an overreaction. Brazil only recently emerged from one the deepest recessions in its history. And from 2010 to 2016 the Brazillian equity market fell by over 75%, wounds still fresh for many.

Turning point

But the reality is the cycle has already turned and conditions are improving. Though the trucker strike will dampen economic activity, it is unlikely to completely derail Brazil’s trajectory, which continues to move in the right direction.

Unemployment, while high by US standards, has been on the decline since its highs in 2017.

The Brazillian Real, which collapsed into the recession, has fully recovered and is bouncing back around all-time highs vs the USD.

And capital flows, which fell off a cliff during the recession have started showing signs of life, albeit in a choppy fashion.

Sniffing for value

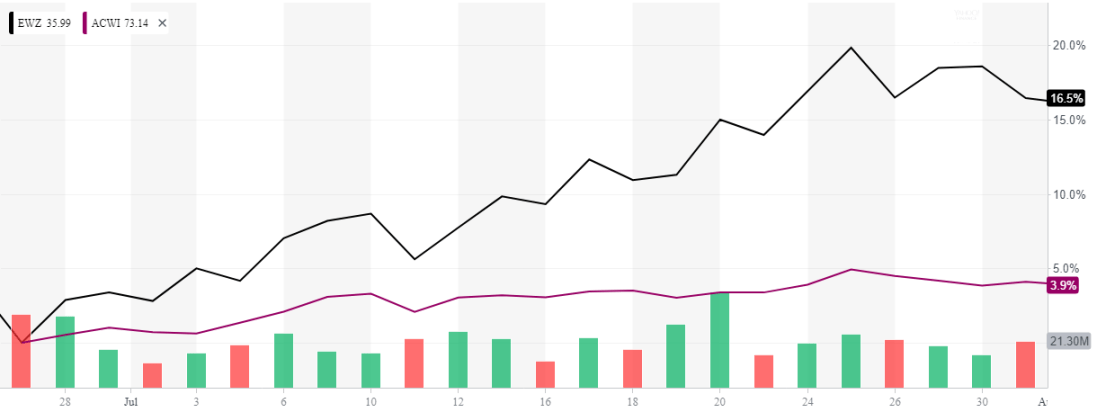

Meanwhile, animal spirits are sniffing up Brazillian equities. Since it’s YTD lows in June, the market has bounced over 16% versus about 4% for the global market.

Source: Yahoo Finance

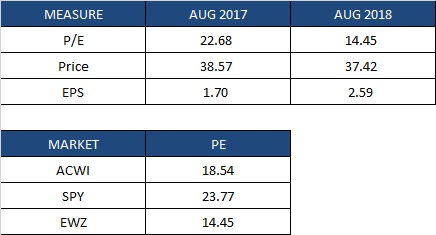

Though market prices are just back to where they were a year ago, valuations actually look better. The trailing P/E for the Brazillian stock market was at 22.68 in August 2017 and sits at 14.45 today, implying aggregate earnings growth of over 50% in the past year. This is particularly attractive in a global market where good values are increasingly hard to find.

Source: ETF.com, BCM

Keeping it real

Of course, emerging markets always come with real risks. Tightening global liquidity has historically been bad for emerging markets in general. Not only is capital more expensive, but emerging markets are also not fully “decoupled.” Rising-rates in developed markets inevitably lead to contractions, and a recession in US or EAFE regions may still affect EM.

Within Brazil, political uncertainty looms over the October general election. There isn’t a clearly favored, market-friendly presidential candidate. And sensitive issues like pension reform and state subsidies which are important to Brazil’s long-term success are up for debate.

Last but not least, though the Brazillian market does not look overbought yet, after the recent rally we’ll likely see some short-term pullback in price. At best it will be profit taking and at worst the search for a new bottom.

The bottom line is we can expect a lot more volatility for Brazil. Despite that, it remains one of my more favored markets at the moment based on outlook and valuation.

Victor K. Lai, CFA

Disclosure: Victor Lai is long EWZ.

You must be logged in to post a comment.