We are within an arm’s length of reaching a “debt ceiling” in the United States. In other words, the government has basically maxed out the national credit card (based on limits established by US law). The Treasury Department has indicated that unless Congress authorizes additional borrowing (which only Congress can do through its lawmaking functions), the United States will not be able to pay all of its bills beyond August 2nd. That would create the first default (or failure to pay an obligation that is due) by the US government in history.

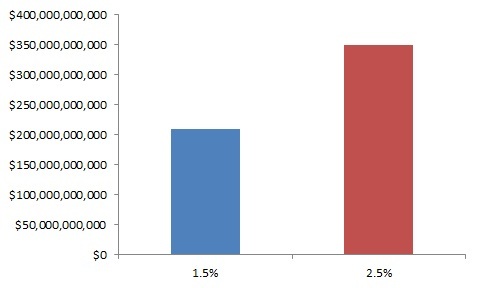

Failure to pay would lower the country’s credit rating, which in turn could raise the interest rates that the government borrows at. Given the government’s enormous debt load, even a small rise in interest rates could result in a significant rise in borrowing costs. Figure 1 shows the hypothetical increase in annual costs for servicing public debt based on a 1% increase in interest rates. The numbers are mind-numbing if you’re not used to looking at values that are trillions in size.

As public dollars are diverted towards debt servicing, there would be fewer resources for things like education, healthcare, government jobs, and public spending in general. Clearly, that would not benefit an already struggling economy.

Other consequences may be more palpable. For example, much of the credit and financing available to individuals and businesses are indexed to interest rates on government debt (i.e. rates on Treasury bills, notes, and bonds). A rise in public sector interest rates could translate into a rise in private sector rates. That would mean higher costs for anyone who borrows to buy a car, buy a house, go to school, start a business, etc. Case in point, a default will be bad for everyone.

In my opinion, an outright default is unlikely. Though Democrats and Republicans are at odds over the terms and conditions for raising the debt limit, choosing not to raise it would spell disaster. Not raising the limit would simply make an already precarious situation even more difficult to deal with – and everyone in Congress must realize that.

That being said, simply raising the debt ceiling may not be enough. Rightfully so, credit rating agencies are concerned about the structural nature of our debt problems. Agencies want to see what steps the government will take to lower its debt burden over time. An increase of the debt ceiling without a compelling plan for debt reduction may not prevent agencies from rating downgrades.

So while an Armageddon scenario of outright default paired with a huge spike in interest rates will probably be avoided, a slight credit downgrade paired with a slight rise in rates is possible. Under such a scenario, I think we could see a peculiar situation where both stock and bond markets could react negatively at the same time – at least initially.

There would likely be inflows into conventional “safe havens” like precious metals (which ironically I do not think are all too safe right now). But as long as default risks are abated, bond markets would probably recover after a limited initial shock. With no default, Treasuries would revert to safe haven status, creating an invisible floor for prices (and even a run up). Stock prices, on the other hand, would probably languish due to a worsened economic outlook.

Given that no one knows for sure what the outcome will be (especially me), and that short-term market movements are impossible to time (correctly and consistently anyway) – I doubt that jumping in or out of the markets in any extreme manner will be a good idea. During times of heightened uncertainty, it’s more important than ever for prudent investors to adhere to a disciplined approach that emphasizes time-tested risk management strategies.

In general, that means maintaining a broadly diversified and properly balanced portfolio that is allocated based on your needs and circumstances, not based on speculation about what the markets may or may not do. For the entrepreneurial among us, reasonable tactical weightings could be used. I would underweight risk assets in general with an offsetting overweight in cash. While cash is earning nothing, it does have the value of optionality, or the ability to buy on weakness. In equities, I would emphasize high quality, reasonably valued, dividend-paying stocks. And in bonds, I would manage both credit quality and duration conservatively.

Victor K. Lai, CFA

This blog is for informational purposes only. Nothing on this blog constitutes investment advice. Bellwether Capital Management LLC does not provide tax or legal advice. You should conduct proper due diligence and/or consult with your professional advisers before taking any investment action.

Pretty insightful!

LikeLike